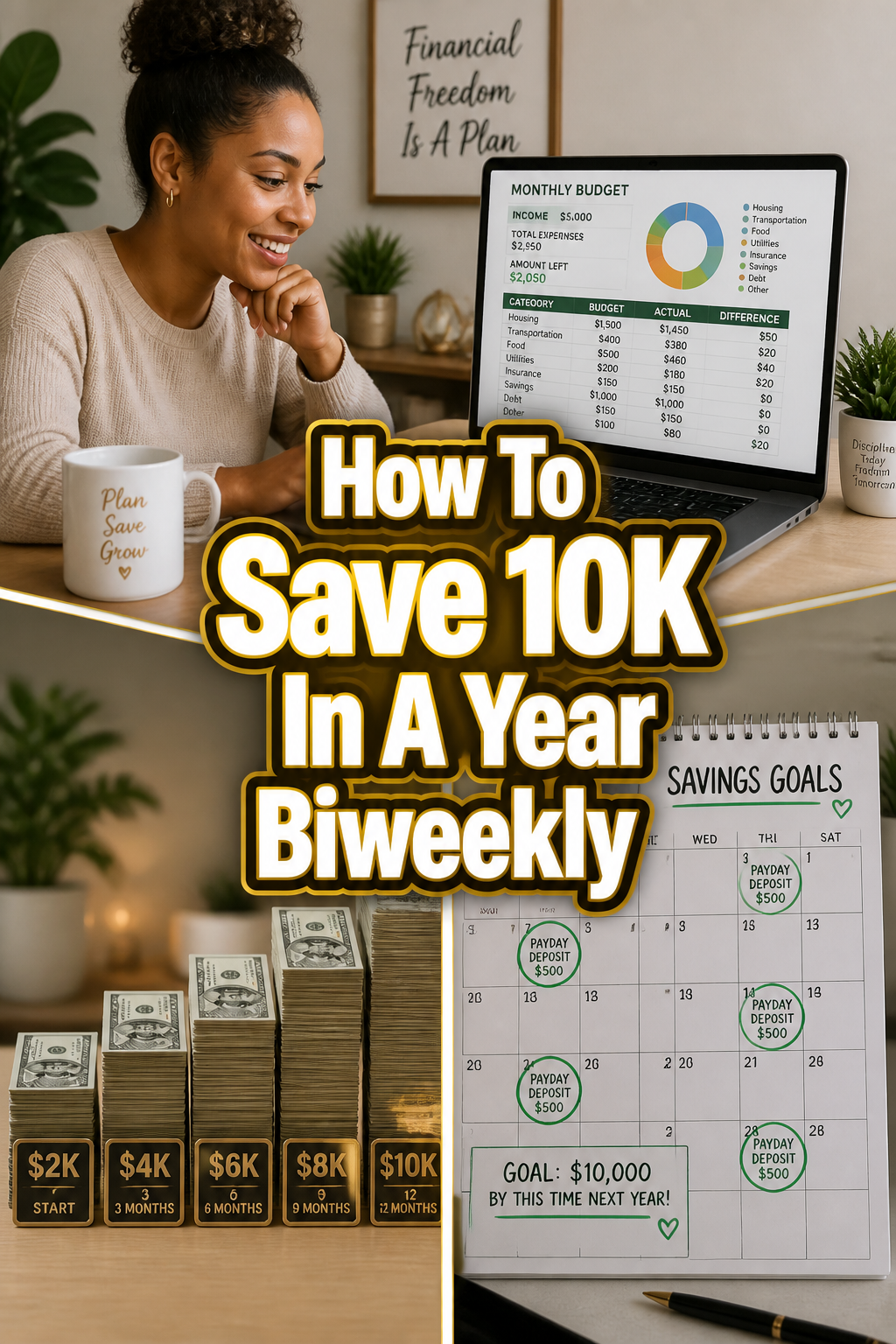

💰 How To Save 10K In A Year Biweekly

📚 The Financial Literacy Library

The best investment you can ever make is in your own financial education. These 5 cornerstone books are what millionaires, financial advisors, and wealth-builders universally recommend for completely rewiring how you think about earning, saving, and investing money.

🧠 The Psychology of Money

Doing well with money isn't necessarily about what you know—it's about how you behave. Morgan Housel masterfully breaks down the emotional and psychological biases that secretly dictate our financial decisions, offering a true paradigm shift in how to view wealth.

🏠 Rich Dad Poor Dad

The #1 personal finance book of all time for a reason. This foundational read shatters the myth that you need to earn a high income to be rich, teaching you the critical difference between working for money and making your money work for you via assets.

📈 Atomic Habits

While not strictly a finance book, building wealth is absolutely dependent on the daily habits you cultivate. James Clear provides the definitive framework for breaking bad spending habits and effortlessly automating the good ones that lead to long-term success.

📊 The Simple Path to Wealth

The ultimate antidote to complex, intimidating financial advice. JL Collins provides an incredibly accessible, low-stress roadmap to financial independence through index fund investing, perfectly explaining why simplicity beats Wall Street complexity every time.

💳 I Will Teach You to Be Rich

A tactical, no-BS, 6-week program that actually works. Ramit Sethi teaches you how to crush debt, automate your savings, and negotiate your salary—all while guilt-free spending on the things you truly love. A must-read for modern money management.

Imagine having an extra $10,000 in your bank account just one year from now. It sounds like a dream, but I’ve seen firsthand how a clear plan makes it a reality for everyday people.

This guide will break down exactly how you can achieve that goal, saving a little bit at a time, biweekly, without feeling deprived.

You’re about to learn practical strategies that have helped many, including myself, build significant savings.

Quick Overview

Saving $10,000 in a year, especially on a biweekly schedule, is a powerful financial goal. This guide will equip you with the knowledge and tools to make it happen.

You’ll learn how to set up your finances, track your progress, and stay motivated every step of the way.

- Time needed: 1 year of consistent effort (initial setup takes 1-2 hours)

- Difficulty: Intermediate (requires discipline and minor lifestyle adjustments)

- What you’ll need: A bank account, budgeting app/spreadsheet, a clear financial goal, and commitment

Step-by-Step Instructions

Step 1: Define Your “Why” and Set Clear Goals

Before you even think about numbers, take a moment to understand why you want to save this money. Is it for a down payment, an emergency fund, a dream vacation, or starting a business?

Having a strong “why” will be your biggest motivator when things get tough. Write it down and keep it visible.

Your goal is specific: $10,000 in one year, saving biweekly. This means you’ll need to save approximately $384.62 every two weeks.

Pro Tip: Visualize what reaching your goal looks like. Create a vision board or write a detailed description of how you’ll feel and what you’ll do with that $10,000. This emotional connection makes the goal feel real.

Step 2: Understand Your Current Cash Flow

You can’t manage what you don’t measure. Start by gathering all your financial statements: bank accounts, credit cards, pay stubs, and recurring bills.

Track every dollar coming in and going out for at least one month. This helps you see exactly where your money goes.

Use a spreadsheet, a notebook, or a budgeting app to categorize your spending. Don’t judge your habits yet; just observe.

Step 3: Create a Realistic Biweekly Budget

Now that you know your cash flow, it’s time to build a budget that prioritizes your $384.62 biweekly savings goal. This isn’t about deprivation; it’s about intentional spending.

List all your biweekly income and then all your fixed expenses (rent, loan payments, subscriptions). Subtract these from your income.

What’s left is your discretionary income. This is where you’ll find the $384.62, and adjust your variable spending (groceries, entertainment, dining out) to accommodate it.

Pro Tip: Use the “50/30/20 rule” as a guideline: 50% for needs, 30% for wants, and 20% for savings and debt repayment. Adjust this to fit your specific goal, aiming for a higher savings percentage if needed.

Step 4: Automate Your Savings

This is arguably the most powerful step. Set up an automatic transfer of $384.62 from your checking account to a dedicated savings account every two weeks, ideally on your payday.

Treat this transfer like a non-negotiable bill. If you don’t see the money, you won’t miss it.

Many banks allow you to schedule recurring transfers. Make sure this savings account is separate from your everyday checking account to avoid accidental spending.

Step 5: Trim the Fat: Identify and Reduce Expenses

Review your budget for areas where you can cut back. Look at your “wants” first. Can you reduce dining out, cancel unused subscriptions, or find cheaper alternatives for services?

Even small changes add up. For example, packing your lunch twice a week could save you $20-$30 biweekly, putting you closer to your goal.

Challenge yourself to find $50-$100 in cuts each biweekly period. You might be surprised how much you can free up.

Pro Tip: Try a “no-spend” challenge for a weekend or even a week. This helps you identify non-essential spending habits and breaks the cycle of impulse purchases. It also shows you how resourceful you can be.

Step 6: Boost Your Income (Even a Little Bit)

If finding $384.62 biweekly feels tight, consider ways to increase your income. This doesn’t mean getting a second full-time job.

Think about side hustles: freelance writing, dog walking, babysitting, selling crafts online, or even selling items you no longer need around your house.

Even an extra $50-$100 a week can significantly ease the pressure on your budget and accelerate your savings.

Step 7: Track Your Progress and Stay Accountable

Regularly check your savings account balance. Seeing your money grow is incredibly motivating. Create a simple tracker, either digital or physical, to mark off each biweekly transfer.

Share your goal with a trusted friend or family member who can offer encouragement and hold you accountable. Their support can make a big difference.

Celebrate small milestones along the way. Reaching your first $1,000 or $5,000 is a huge accomplishment and deserves recognition.

Step 8: Be Flexible and Adjust as Needed

Life happens. There will be unexpected expenses or periods where saving $384.62 feels difficult. Don’t get discouraged if you miss a transfer or have to save less for a period.

The key is to get back on track as soon as possible. Review your budget regularly, perhaps once a month, to see if adjustments are needed.

Perhaps you found a new way to save, or an unexpected bonus came in. Use these opportunities to catch up or even get ahead.

Step 9: Understand the Power of Compound Interest (for the long term)

While your primary goal is to accumulate $10,000, it’s wise to understand what your savings can do over time. Once you hit your goal, consider moving your money to a high-yield savings account or even investing it.

Compound interest means your money earns interest, and then that interest also earns interest. This concept is a wealth-building superpower over many years.

For now, focus on saving, but keep this long-term vision in mind to inspire future financial growth.

Common Mistakes to Avoid

Ignoring Your “Why”

Starting to save without a clear purpose often leads to losing motivation. When you don’t know why you’re saving, it’s easy to justify spending the money elsewhere.

Always keep your ultimate goal in mind. Revisit your “why” whenever you feel your resolve weakening to reignite your commitment.

Failing to Track Spending

Many people create a budget but then don’t stick to it because they don’t actually know where their money is going. Without tracking, you’re just guessing.

Regularly review your bank statements and categorize your expenses. This honest look at your habits is crucial for making informed financial decisions.

Being Too Restrictive

A budget that’s too tight and doesn’t allow for any fun or flexibility is unsustainable. You’ll quickly feel deprived and give up entirely.

Build in some money for “wants” or a small “fun fund.” It’s better to save a little less consistently than to burn out trying to save too much too fast.

Not Automating Savings

Relying on willpower alone to transfer money to savings is a recipe for failure for most people. Life gets busy, and that transfer often gets forgotten or pushed aside.

Set up automatic transfers from your checking to your savings account immediately after you get paid. Make it a non-negotiable part of your financial routine.

Troubleshooting

I Can’t Afford $384.62 Biweekly

This is a common concern. Start by re-evaluating your expenses with a fine-tooth comb. Can you cut even more, perhaps temporarily, like pausing subscriptions or reducing entertainment?

If cuts aren’t enough, focus on increasing your income. Even an extra $50-$100 from a side gig can make a huge difference. You might need to adjust your timeline slightly, but don’t give up on the goal.

I Keep Dipping Into My Savings Account

If your savings account is too accessible, it’s easy to use it for non-emergencies. Consider opening an account at a different bank than your primary checking, making transfers a little less convenient.

Also, ensure you have a separate emergency fund. If you’re using your $10K savings for unexpected costs, it means you lack a buffer for true emergencies.

I Lost Motivation Halfway Through

It’s normal to feel your motivation wane. Reconnect with your “why.” Look at your progress tracker and see how far you’ve come. Remind yourself of the positive impact this money will have.

Talk to your accountability partner. Perhaps reward yourself with a small, non-financial treat for hitting a milestone. Sometimes, a short break from intense saving can help you reset.

Key Takeaways

- Clarity is King: Define your “why” and know exactly how much you need to save biweekly ($384.62).

- Budget Smart: Understand your income and expenses to create a realistic spending plan that prioritizes your savings.

- Automate Everything: Set up automatic transfers to a dedicated savings account to ensure consistent progress.

- Trim & Earn: Actively look for ways to reduce expenses and explore options to boost your income, even slightly.

- Track & Celebrate: Monitor your progress regularly and acknowledge milestones to stay motivated and accountable.

- Stay Flexible: Be prepared to adjust your plan when life throws curveballs, and always get back on track quickly.

Frequently Asked Questions

Is $10,000 in a year a realistic goal for most people?

Yes, it is absolutely realistic for many people, especially with a clear plan and consistent effort. It requires discipline and sometimes making temporary sacrifices, but it’s an achievable goal that can significantly improve your financial standing.

Should I use a separate bank for my savings account?

Using a separate bank can be very helpful. It creates a slight barrier to accessing the funds, reducing the temptation to dip into your savings for impulse purchases. It also helps you mentally separate your savings from your everyday spending money.

What if I have debt? Should I save or pay off debt first?

This often depends on the type of debt. High-interest debt (like credit card debt) usually makes more sense to pay off first due to the high interest rates. However, having a small emergency fund (e.g., $1,000) is often recommended before tackling debt aggressively. Once that’s established, you can focus on the debt or balance saving and debt repayment, depending on your specific situation.

How can I stay motivated when I feel like giving up?

Revisit your initial “why” and visualize the end result. Review your progress to see how far you’ve come. Talk to a trusted friend or family member about your struggles. Sometimes, a small, non-financial reward for hitting a milestone can also provide a much-needed boost.

Our Top Recommended Finds

- Budgeting App (e.g., YNAB, Mint, Personal Capital): These tools help you track spending, categorize transactions, and visualize your financial progress effortlessly.

- High-Yield Savings Account: Once you start accumulating savings, move your money to an account that offers a higher interest rate than traditional banks, making your money work harder for you.

- A Simple Notebook and Pen: Sometimes, the best tools are the simplest. A physical notebook for tracking expenses and writing down your goals can be incredibly effective and low-tech.

Your Path to Financial Freedom Starts Today

Saving $10,000 in a year, biweekly, isn’t just about the money; it’s about building financial discipline and proving to yourself what you’re capable of.

This journey will teach you valuable lessons about your spending habits, your priorities, and your resilience.

Don’t wait for the “perfect” time to start. The best time is always now. Take that first step, set up your automation, and watch your savings grow.

Once you hit this goal, consider exploring topics like investing for beginners, building a substantial emergency fund, or planning for retirement. Your financial future is in your hands – go make it happen!