🏠 How To Save Money To Buy A House

📚 The Financial Literacy Library

The best investment you can ever make is in your own financial education. These 5 cornerstone books are what millionaires, financial advisors, and wealth-builders universally recommend for completely rewiring how you think about earning, saving, and investing money.

🧠 The Psychology of Money

Doing well with money isn't necessarily about what you know—it's about how you behave. Morgan Housel masterfully breaks down the emotional and psychological biases that secretly dictate our financial decisions, offering a true paradigm shift in how to view wealth.

🏠 Rich Dad Poor Dad

The #1 personal finance book of all time for a reason. This foundational read shatters the myth that you need to earn a high income to be rich, teaching you the critical difference between working for money and making your money work for you via assets.

📈 Atomic Habits

While not strictly a finance book, building wealth is absolutely dependent on the daily habits you cultivate. James Clear provides the definitive framework for breaking bad spending habits and effortlessly automating the good ones that lead to long-term success.

📊 The Simple Path to Wealth

The ultimate antidote to complex, intimidating financial advice. JL Collins provides an incredibly accessible, low-stress roadmap to financial independence through index fund investing, perfectly explaining why simplicity beats Wall Street complexity every time.

💳 I Will Teach You to Be Rich

A tactical, no-BS, 6-week program that actually works. Ramit Sethi teaches you how to crush debt, automate your savings, and negotiate your salary—all while guilt-free spending on the things you truly love. A must-read for modern money management.

Remember that feeling of seeing your dream home, but then the panic sets in when you think about the down payment? I’ve been there, staring at bank statements, wondering if homeownership was just a distant fantasy.

But I learned that with a clear plan and smart strategies, that dream can become a reality much sooner than you think.

This guide distills my personal journey and years of financial wisdom into actionable steps, helping you build your house fund with confidence.

Quick Overview

This guide will walk you through the essential steps to build your home savings. You’ll learn how to set clear financial goals, optimize your budget, boost your income, and make your money grow, all geared towards buying your first house.

Time needed: 3-4 hours to set up your initial plan, ongoing daily/weekly effort

Difficulty: Intermediate (requires consistent discipline and focus)

What you’ll need: Pen and paper or spreadsheet software, recent bank statements, a clear vision of your homeownership goal

Step-by-Step Instructions

Step 1: Define Your Dream Home & Budget

Before you can save, you need a target. Understanding the financial goal helps you stay motivated and focused. Researching actual costs grounds your dream in reality.

Research local housing market prices in your desired areas. Look at recent sales of homes similar to what you envision.

Understand the typical down payment requirements. While 20% is ideal to avoid Private Mortgage Insurance (PMI), many programs allow for much less.

Calculate potential closing costs. These are fees associated with buying a home, usually 2-5% of the loan amount, and are often overlooked.

Factor in a separate emergency fund. You’ll want cash reserves after buying your home for unexpected repairs or job changes.

Pro Tip: Use online mortgage calculators to estimate monthly payments based on different down payment amounts. This gives you a clear picture of what’s affordable.

Step 2: Master Your Money Map (Budgeting)

A budget isn’t about restriction; it’s about control. Knowing where your money goes is the first step to directing it towards your home. This map illuminates your spending habits.

Track every dollar you spend for at least one month. Use an app, a spreadsheet, or simply a notebook.

Categorize your expenses into “needs” (rent, groceries, utilities) and “wants” (dining out, entertainment, new gadgets). Be honest with yourself.

Create a strict budget with a dedicated line item for “House Savings.” Make this a priority, not an afterthought.

Identify areas where you can cut back on wants. Even small, consistent reductions add up over time.

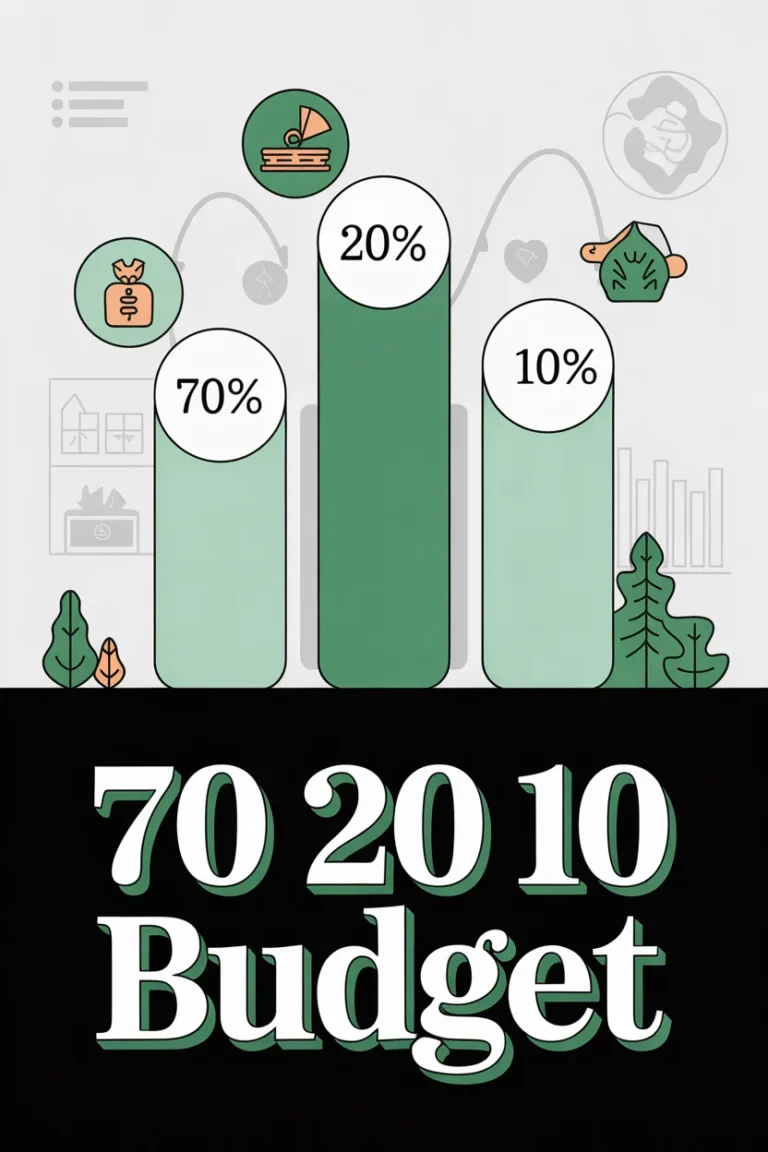

Pro Tip: Try the 50/30/20 rule: 50% of your income for needs, 30% for wants, and 20% for savings and debt repayment. Adjust the savings portion upwards if you’re aggressive about homeownership.

Step 3: Supercharge Your Savings Rate

Once you know where your money is going, it’s time to redirect more of it. This step focuses on finding extra cash within your existing expenses. Every dollar saved is a dollar closer to your home.

Review all your subscriptions (streaming services, gym memberships, apps). Cancel anything you don’t use regularly or truly value.

Cook at home more often and pack your lunches. Eating out is a major budget drain for many people.

Negotiate your bills. Call your internet, cable, or insurance providers and ask for a better rate or explore competitor pricing.

Find cheaper alternatives for everyday items. Switch to generic brands, shop sales, or explore discount stores.

Pro Tip: Automate your savings transfers. Set up an automatic transfer from your checking account to your dedicated house savings account every payday. “Pay yourself first” before you have a chance to spend it.

Step 4: Boost Your Income Streams

Saving isn’t just about cutting expenses; it’s also about earning more. Increasing your income can significantly accelerate your home-saving timeline. Think creatively about your skills and time.

Explore side gigs or freelancing opportunities. Consider pet sitting, tutoring, graphic design, delivery services, or virtual assistant work.

Sell unused items around your home. Decluttering your space can bring in hundreds or even thousands of dollars. Use platforms like Facebook Marketplace or eBay.

Ask for a raise or promotion at your current job. Prepare by documenting your achievements and contributions to the company.

Develop a new skill that can command a higher hourly rate or open up new income avenues. Online courses can be a great investment.

Pro Tip: Treat any extra income from side hustles or bonuses as “house money.” Immediately transfer it to your savings account before it can be absorbed into your regular spending.

Step 5: Smart Debt Management

Debt can be a major roadblock to homeownership. High debt levels impact your ability to qualify for a mortgage and divert funds that could be going towards your down payment. Managing it strategically is crucial.

List all your current debts, including credit cards, personal loans, and auto loans. Note their interest rates and minimum payments.

Prioritize paying off high-interest debt first. The money saved on interest can then be redirected to your house fund.

Avoid taking on new debt while saving for a house. Resist the urge to make large purchases on credit.

Understand how your debt-to-income (DTI) ratio affects mortgage eligibility. Lenders prefer a lower DTI, typically below 43%.

Pro Tip: Even if you have low-interest debt, consider making extra payments if it frees up monthly cash flow. This improves your DTI and makes your budget more flexible.

Step 6: Grow Your Home Fund (Invest Wisely)

Your money shouldn’t just sit there; it should work for you. While long-term investing involves higher risk, there are smart, lower-risk ways to grow your down payment fund.

Open a high-yield savings account (HYSA). These accounts offer significantly higher interest rates than traditional savings accounts, accelerating your growth.

Consider a Roth IRA for first-time homebuyer withdrawals. You can withdraw contributions tax-free and penalty-free for a first-time home purchase (up to $10,000 in earnings).

Learn about low-risk investment options for shorter timelines (1-5 years). This might include Certificates of Deposit (CDs) or short-term government bonds.

Avoid chasing high-risk investments like individual stocks or cryptocurrency for money you need in the near future. The potential for loss is too great.

Pro Tip: Keep a close eye on interest rates and account fees. Transfer your funds if you find a better HYSA rate elsewhere. Every fraction of a percent counts.

Step 7: Stay Motivated & On Track

Saving for a house is a marathon, not a sprint. Maintaining motivation is key to staying consistent and reaching your goal. Celebrate your progress along the way.

Set mini-goals for your savings. For example, “Save $5,000 by June” or “Pay off credit card X by October.”

Visualize living in your new home. Keep a picture of your dream house or a mood board where you can see it daily.

Celebrate small wins. When you hit a savings milestone, treat yourself to a small, budget-friendly reward that doesn’t derail your progress.

Review your progress regularly. Schedule monthly check-ins with your budget and savings accounts to see how far you’ve come and make adjustments.

Pro Tip: Find an accountability partner. This could be a friend, family member, or your partner. Share your goals and progress to keep each other motivated.

Common Mistakes to Avoid

Ignoring Closing Costs

Many aspiring homeowners focus solely on the down payment, forgetting the additional expenses that come with buying a house. Closing costs, which include appraisal fees, legal costs, title insurance, and various taxes, can add 2-5% of the home’s value to your total outlay. This oversight can lead to a significant shortage of funds right before you close. Always factor in these extra expenses from the very beginning of your saving journey.

Not Having an Emergency Fund

Diving headfirst into saving for a house without a separate, fully funded emergency account leaves you incredibly vulnerable. Unexpected expenses, like a car repair or medical bill, can force you to dip into your house savings, completely derailing your progress. Aim to have 3-6 months of living expenses saved in a separate, easily accessible account before aggressively saving for a down payment. This protects your home fund.

Falling for “Lifestyle Creep”

As your income grows, it’s natural to want to enjoy the fruits of your labor. However, letting your spending increase along with your earnings, known as “lifestyle creep,” directly sabotages your saving efforts. Instead of funneling extra income into discretionary spending, consciously resist upgrading your lifestyle and direct any additional funds straight into your house savings. This discipline is vital for accelerated saving.

Being Undisciplined with Your Budget

Creating a detailed budget is an excellent start, but it’s only half the battle. Consistently sticking to your budget requires ongoing discipline and commitment. If you frequently overspend on “wants” or regularly dip into your savings, your homeownership timeline will stretch indefinitely. Regularly review and adjust your budget, holding yourself accountable for every dollar, to ensure you stay on track.

Troubleshooting

“I can’t seem to save enough each month.”

Revisit your budget with a fine-tooth comb. Are there any “wants” that can be cut or significantly reduced, even temporarily, to boost your savings? Consider trying a temporary “no-spend” challenge for a month to reset your habits and identify hidden spending. This challenge can reveal surprising areas for savings.

This issue might also signal a need to focus more on boosting your income. Can you pick up an extra shift at work, freelance for a few hours each week, or sell some items you no longer need? Sometimes, earning more is more effective than cutting more.

“I keep dipping into my house savings.”

This often happens when your savings are too easily accessible or you lack a robust emergency fund. Ensure your house fund is in a dedicated, perhaps slightly less convenient, account that isn’t linked to your everyday spending. This creates a mental barrier.

Also, evaluate why you’re dipping into it. Is it for genuine emergencies (indicating a need for a separate emergency fund) or for discretionary spending? Addressing the root cause directly, whether it’s a budgeting issue or a lack of emergency cash, is crucial.

“My partner and I aren’t on the same page about saving.”

Open, honest communication is absolutely key when saving with a partner. Sit down together and clearly define your shared homeownership goal, making sure you both envision the same future. Discuss your individual financial habits, fears, and aspirations.

Create a joint budget and savings plan that you both agree on and feel committed to. Schedule regular financial check-ins to review your progress, celebrate milestones, and address any concerns or disagreements proactively. Alignment is power.

Key Takeaways

Clearly define your homeownership goal, including estimated costs for down payment and closing fees.

Create and consistently stick to a detailed budget, prioritizing your home savings.

Aggressively increase your savings rate by cutting expenses and boosting your income.

Manage existing debt wisely to improve your financial standing and mortgage eligibility.

Utilize appropriate savings vehicles like high-yield accounts to grow your money faster.

Maintain motivation by setting small milestones, visualizing your goal, and celebrating progress.

Frequently Asked Questions

How much should I save for a down payment?

While a 20% down payment is often recommended to avoid private mortgage insurance (PMI) and secure better interest rates, many lenders offer options with as little as 3-5% down. Research FHA loans or conventional loans with lower down payment requirements. Remember, a larger down payment generally means lower monthly payments and less interest paid over the life of the loan.

Should I pay off all my debt before saving for a house?

Not necessarily all debt, but you should definitely prioritize paying off high-interest debt, such as credit card balances. Student loans or car loans with low interest rates can often be managed alongside saving, as long as your overall debt-to-income ratio remains healthy. Lenders look at your total debt burden when considering mortgage applications.

What’s the fastest way to save for a house?

The fastest way involves a powerful combination of aggressive expense reduction and significant income boosting. This means making tough, temporary choices, like cutting all non-essential spending and actively taking on extra work or side hustles. Simultaneously, ensure all your savings are earning the highest possible interest in a high-yield account.

How long does it typically take to save for a house?

This timeline varies greatly based on your income, current expenses, the cost of homes in your desired area, and your savings rate. For many, it could take anywhere from 2 to 7 years to save a substantial down payment. The key is consistent saving, adapting your plan as needed, and maintaining motivation through regular progress checks.

Our Top Recommended Finds

Budgeting App (e.g., YNAB, Mint, Personal Capital): These digital tools are essential for effortlessly tracking your spending, categorizing expenses, and visualizing your financial picture, making budgeting much easier to maintain.

High-Yield Savings Account (HYSA): Moving your down payment fund to an FDIC-insured HYSA means your money earns significantly more interest than in a traditional savings account, helping your principal grow faster with minimal risk.

Personal Finance Books (e.g., The Total Money Makeover, I Will Teach You To Be Rich): These resources offer deeper insights into wealth building, budgeting strategies, and investing principles, empowering you with knowledge to make smarter financial decisions.

Your Homeownership Journey Starts Today

Saving for a home is a significant undertaking, but it’s one of the most rewarding financial goals you can achieve. The path may have its challenges, yet with a clear plan and unwavering commitment, your dream home is well within reach.

Now that you’ve got a solid foundation, consider exploring related topics like “Understanding Different Mortgage Options” or “Finding First-Time Homebuyer Programs” in your area. The biggest step is simply starting. Pick one actionable item from this guide and implement it today. Your future self, enjoying coffee in your own home, will thank you.