📊 70 20 10 Budget

📚 The Financial Literacy Library

The best investment you can ever make is in your own financial education. These 5 cornerstone books are what millionaires, financial advisors, and wealth-builders universally recommend for completely rewiring how you think about earning, saving, and investing money.

🧠 The Psychology of Money

Doing well with money isn't necessarily about what you know—it's about how you behave. Morgan Housel masterfully breaks down the emotional and psychological biases that secretly dictate our financial decisions, offering a true paradigm shift in how to view wealth.

🏠 Rich Dad Poor Dad

The #1 personal finance book of all time for a reason. This foundational read shatters the myth that you need to earn a high income to be rich, teaching you the critical difference between working for money and making your money work for you via assets.

📈 Atomic Habits

While not strictly a finance book, building wealth is absolutely dependent on the daily habits you cultivate. James Clear provides the definitive framework for breaking bad spending habits and effortlessly automating the good ones that lead to long-term success.

📊 The Simple Path to Wealth

The ultimate antidote to complex, intimidating financial advice. JL Collins provides an incredibly accessible, low-stress roadmap to financial independence through index fund investing, perfectly explaining why simplicity beats Wall Street complexity every time.

💳 I Will Teach You to Be Rich

A tactical, no-BS, 6-week program that actually works. Ramit Sethi teaches you how to crush debt, automate your savings, and negotiate your salary—all while guilt-free spending on the things you truly love. A must-read for modern money management.

Are you tired of feeling overwhelmed by your finances? Do you dream of a simpler, more effective way to manage your money, save for the future, and even build lasting wealth? If so, you’re in the right place! Welcome to the world of the 70 20 10 Budget – a powerful yet wonderfully straightforward financial framework that’s helping countless individuals transform their relationship with money. Forget complex spreadsheets and restrictive rules; this isn’t about deprivation, it’s about smart allocation, intentional living, and unlocking your financial potential.

In a world where financial advice often feels complicated and out of reach, the 70 20 10 Budget stands out for its clarity and adaptability. It’s more than just a budgeting method; it’s a mindset shift that empowers you to take control, reduce financial stress, and actively work towards your goals. Whether you’re just starting your financial journey, looking to regain control, or aiming to accelerate your wealth-building efforts, this guide will walk you through everything you need to know. We’ll break down the concept, share practical tips, reveal common pitfalls to avoid, and equip you with the knowledge to make this budget work seamlessly for your life. Get ready to embrace a money-smart approach that’s friendly, motivational, and genuinely designed to help you thrive!

What is 70 20 10 Budget?

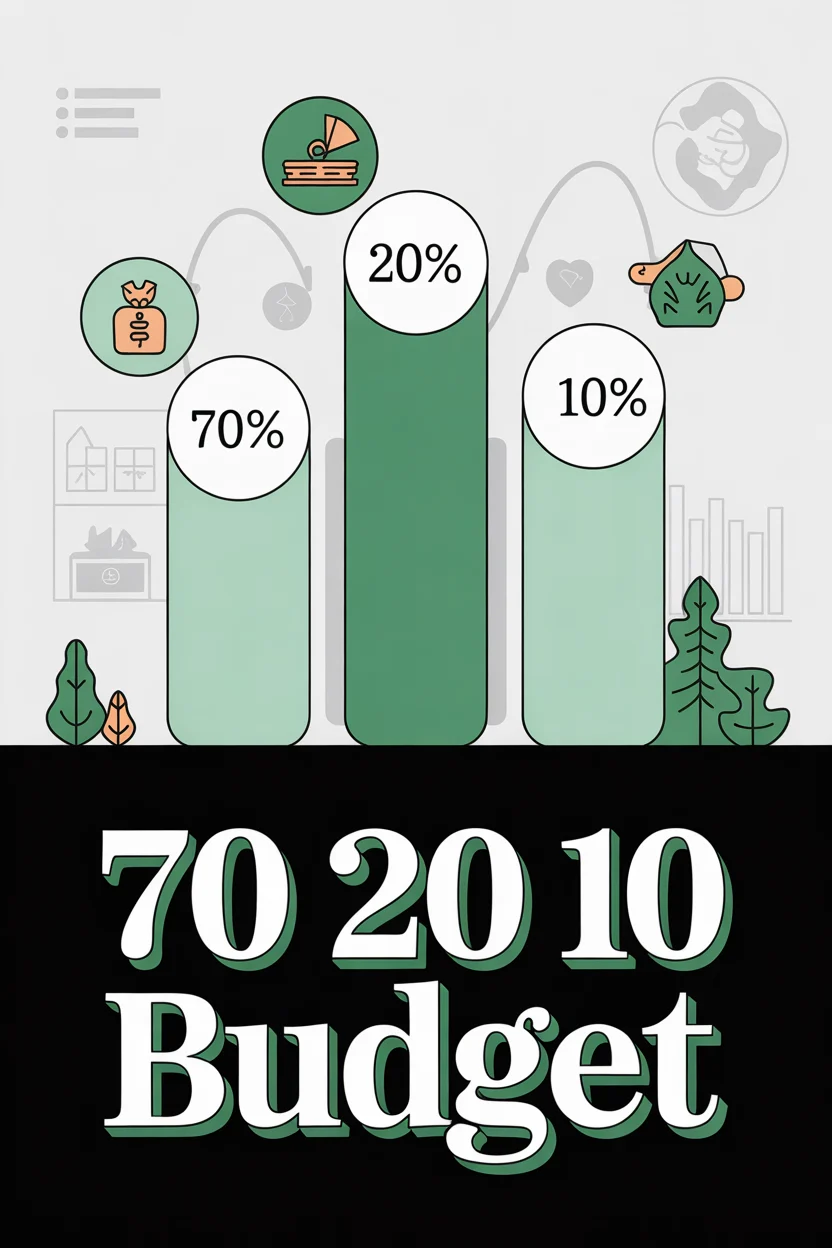

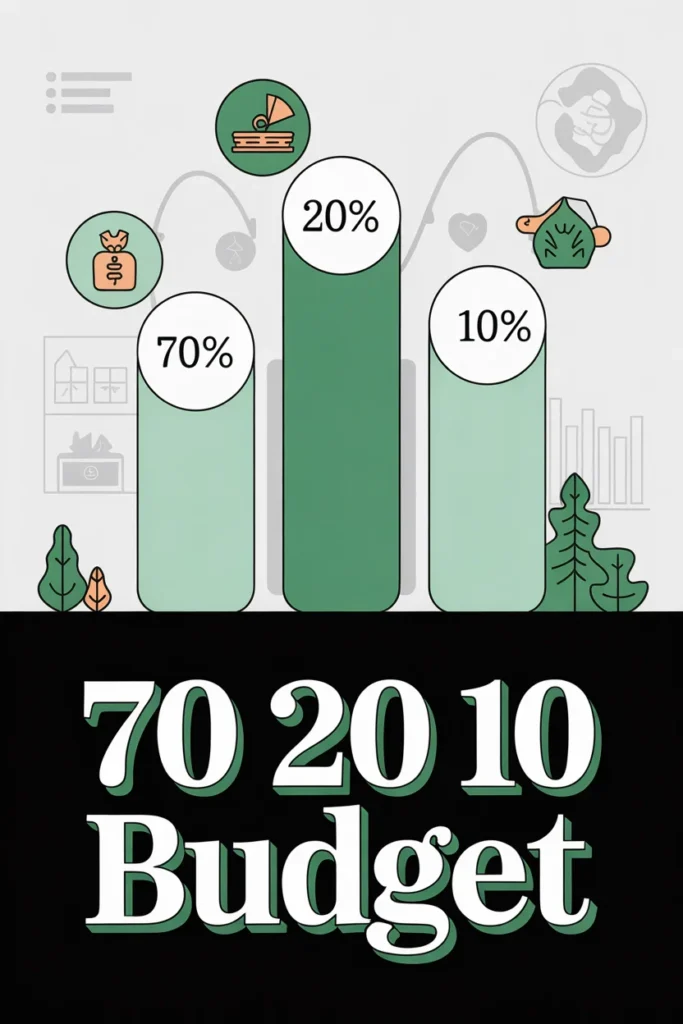

At its core, the 70 20 10 Budget is a simple yet incredibly effective rule of thumb for managing your income. It suggests that you divide your after-tax (net) income into three distinct categories with specific percentages: 70% for your Needs & Wants, 20% for Savings & Debt Repayment, and 10% for Giving & Investing (often referred to as wealth building or impact investing). This method provides a clear, actionable framework for allocating your money, ensuring you cover your present expenses, secure your future, and even contribute to causes or investments that fuel long-term growth.

The Three Pillars Explained:

- 70% Needs & Wants (Living Expenses): This is the largest portion of your income and covers all your everyday living expenses, both essential and discretionary. Think of it as your “lifestyle fund.”

- Needs: These are your non-negotiable expenses that keep a roof over your head, food on your table, and the lights on. Examples include rent/mortgage payments, utilities (electricity, water, internet), groceries, transportation costs (car payment, gas, public transit), essential insurance, and basic personal care items.

- Wants: These are the discretionary items and experiences that enhance your quality of life but aren’t strictly necessary for survival. This could include dining out, entertainment (streaming services, movies, concerts), hobbies, vacations, new clothes (beyond essentials), and non-essential subscriptions. The beauty of the 70% is that it allows for both, giving you flexibility to enjoy life while still budgeting responsibly.

Example: If your after-tax income is $4,000 per month, $2,800 (70%) would be allocated to cover all your needs and wants.

- 20% Savings & Debt Repayment: This crucial segment is dedicated to building your financial security and eliminating burdensome debt. It’s your engine for future stability.

- Savings: This primarily focuses on building an emergency fund (aim for 3-6 months of living expenses), but also includes saving for larger short-term goals like a down payment on a house, a new car, or a significant trip.

- Debt Repayment: This portion is specifically for tackling high-interest debt beyond minimum payments. Think credit card debt, personal loans, or even accelerating student loan payments. Prioritizing this can save you thousands in interest over time.

Example: With a $4,000 after-tax income, $800 (20%) would go towards savings and/or debt repayment. You might put $400 into your emergency fund and $400 towards an aggressive credit card payoff.

- 10% Giving & Investing (Wealth Building): This is where you truly supercharge your financial future and make an impact. It’s about growing your money and contributing to the world around you.

- Giving: This includes charitable donations to causes you care about, tithing, or helping out friends and family in need. It fosters a sense of abundance and generosity.

- Investing: This is for long-term wealth creation. Think contributions to a retirement account (like a Roth IRA or 401k beyond any employer match that might already be deducted from gross pay), investing in a brokerage account for long-term growth, or even funding a child’s college education plan. This is where your money starts working for you, compounding over time to build substantial wealth.

Example: From your $4,000 after-tax income, $400 (10%) could be split, perhaps $100 for charitable giving and $300 invested into a low-cost index fund or your retirement account.

The beauty of the 70 20 10 Budget lies in its clear direction. It simplifies complex financial decisions into manageable percentages, allowing you to easily see where your money should go and helping you make conscious choices about your spending and saving habits.

Key Features

The 70 20 10 Budget isn’t just another financial fad; it’s a robust framework with several standout features that make it incredibly effective and popular:

- Simplicity and Clarity: Perhaps its most appealing feature is its straightforwardness. You don’t need to be a finance expert to understand or implement it. The percentages are clear, easy to remember, and provide an immediate roadmap for your money, cutting through the confusion often associated with budgeting.

- Built-in Balance: This method inherently balances your present needs with your future financial security and wealth-building aspirations. It acknowledges that you need to live and enjoy life now (70%), but also ensures you’re proactively saving and reducing debt (20%) while simultaneously growing your wealth and making an impact (10%). This holistic approach prevents you from feeling deprived or neglecting important financial goals.

- Flexibility and Adaptability: While the percentages are a guideline, the 70 20 10 Budget is highly adaptable. It works for various income levels and life stages. As your income grows, your capacity for savings and investments increases within the same framework. If you face a temporary financial setback, you can temporarily adjust within the 70% “Needs & Wants” category to prioritize essentials, knowing you have a solid structure to return to.

- Empowerment Through Intentionality: This budget encourages intentional spending rather than restrictive deprivation. By assigning a purpose to every dollar, you gain a sense of control and empowerment over your money. You’re not just spending; you’re allocating funds in alignment with your values and long-term goals.

- Focus on Wealth Building: Unlike some budgets that primarily focus on just covering expenses, the 70 20 10 method explicitly carves out a significant portion (20% + 10%) for building a robust financial future. It ensures that savings, debt repayment, and long-term investments are non-negotiable parts of your financial plan, setting you on a clear path to financial independence.

How to Get Started

Ready to dive in and take control of your finances with the 70 20 10 Budget? Here’s a step-by-step guide to get you started:

- Calculate Your After-Tax Income:

- Crucial First Step: Do NOT use your gross income (the amount before taxes and deductions). You need to know your net income – the actual amount that hits your bank account after all taxes, benefits, and retirement contributions (like a 401k match, which is often considered part of your savings already) have been deducted.

- Gather Your Pay Stubs: Look at your most recent pay stubs or bank statements to find your take-home pay. If you have irregular income, average your income over the last 3-6 months to get a realistic monthly figure.

Example: If your gross pay is $5,000, but after taxes and deductions, your take-home pay is $4,000, then $4,000 is your after-tax income for this budget.

- Allocate Your Funds According to the Percentages:

- 70% for Needs & Wants: This is your biggest category.

- Track Your Current Spending: For a month or two, meticulously track where every dollar goes. Use a budgeting app, a spreadsheet, or even a notebook. This will give you a realistic picture of your current expenses.

- Identify Areas for Adjustment: Compare your actual spending to your 70% allocation. Are you over or under? If you’re consistently spending more than 70%, identify “wants” that can be trimmed (e.g., fewer restaurant meals, cheaper entertainment, canceling unused subscriptions) to bring you back within target.

- Prioritize Needs: Ensure all your essential needs are covered first within this 70%.

- 20% for Savings & Debt Repayment: This is where you build your safety net and tackle high-interest debt.

- Emergency Fund First: If you don’t have one, prioritize building a starter emergency fund (e.g., $1,000-$2,000) here.

- Tackle High-Interest Debt: Once you have a small emergency fund, aggressively pay down credit card debt, personal loans, or other high-interest consumer debt.

- Mid-Term Savings Goals: Allocate funds for things like a down payment, a new car, or a significant vacation once the emergency fund is robust and high-interest debt is managed.

- 10% for Giving & Investing: This fuels your long-term wealth and impact.

- Long-Term Investments: Direct funds into retirement accounts (IRA, 401k), brokerage accounts, or educational savings plans.

- Charitable Contributions: Set aside money for causes you believe in.

- 70% for Needs & Wants: This is your biggest category.

- Automate Everything Possible:

- Make it Effortless: This is a game-changer. Set up automatic transfers from your checking account to your savings, investment accounts, and even a separate “giving” account on payday.

- Pay Yourself First: By automating, you ensure that your 20% and 10% are taken care of before you even have a chance to spend it. This is the most powerful budgeting hack!

- Track, Review, and Adjust Regularly:

- Monitor Your Spending: Keep an eye on your 70% category throughout the month. Are you staying within your limits?

- Monthly Check-ins: At least once a month, sit down and review your budget. See what worked, what didn’t, and where you might need to make adjustments.

- Be Flexible: Life happens! Your budget isn’t set in stone. If your income changes, or you have a major life event, be prepared to adjust your allocations. The goal is progress, not perfection.

Tips for Success

Implementing a new budget can feel like a big step, but with these money-smart tips, you’ll be well on your way to mastering the 70 20 10 Budget and achieving your financial goals:

- Automate Your Savings and Investments (Seriously!): This cannot be stressed enough. Set up automatic transfers from your checking account to your savings, debt repayment, and investment accounts to occur on or immediately after your payday. This “pay yourself first” strategy ensures your financial future is prioritized before you have a chance to spend the money. It removes willpower from the equation and makes consistent progress effortless.

- Clearly Distinguish Between Needs and Wants: This is crucial for managing your 70%. A “need” is something essential for survival and basic living (shelter, food, utilities, transportation to work). A “want” enhances your life but isn’t strictly necessary (daily lattes, streaming services, dining out, new gadgets). Be honest with yourself. If your 70% feels too tight, scrutinize your “wants” first. Can you cut back on dining out, find cheaper entertainment, or reduce subscriptions?

- Start Small and Be Patient: If you’re currently spending more than 70% on needs and wants, don’t try to go from 90% to 70% overnight. Start by aiming for 80/15/5, then gradually adjust to 75/18/7, and eventually hit 70/20/10. Small, consistent improvements are more sustainable than drastic, unsustainable cuts. Financial success is a marathon, not a sprint.

- Find Your Budgeting Tools: Whether it’s a spreadsheet, a dedicated budgeting app (like Mint, YNAB, or Personal Capital), or even a simple pen and paper, find a tool that helps you track your spending and income effectively. The best tool is the one you’ll actually use consistently. Seeing where your money goes in black and white is incredibly powerful.

- Celebrate Small Wins and Stay Motivated: Acknowledging your progress, no matter how small, can keep you motivated. Paid off a credit card? Celebrated! Hit your emergency fund goal? Treat yourself (modestly, within your 70%!). Financial journeys can be long, so positive reinforcement is key to staying engaged and committed.

Common Mistakes to Avoid

While the 70 20 10 Budget is simple, there are a few common pitfalls that can derail your progress. Being aware of them can help you steer clear and stay on track:

- Using Gross Income Instead of Net Income: This is perhaps the most frequent mistake. If you budget based on your income before taxes and deductions, your percentages will be skewed, and you’ll always feel like you’re falling short. Always use your after-tax (net) income – the money that actually lands in your bank account.

- Being Too Rigid or Giving Up Too Soon: Life is unpredictable. There will be months with unexpected expenses or income fluctuations. If you have an “off” month, don’t throw in the towel. Adjust, learn from it, and get back on track next month. A budget is a living document, not a rigid set of rules that lead to failure if not followed perfectly.

- Ignoring the 20% or 10% Categories: It’s easy to let the 70% needs and wants consume everything, especially when starting out. However, the 20% for savings/debt and 10% for investing/giving are the wealth-building engines of this budget. Neglecting them means you’re missing out on compounding interest, debt freedom, and long-term financial security. Make these non-negotiable.

- Not Tracking Spending Within the 70%: Just because 70% is for “needs and wants” doesn’t mean it’s a free-for-all. You still need to track where that money is going. Without tracking, you won’t know if you’re overspending in certain areas or if you have room to reallocate funds for more enjoyment or to boost your savings.

- Failing to Automate: Relying purely on willpower to transfer funds to savings or investments is a recipe for inconsistency. If you don’t automate, you’re much more likely to spend the money instead of saving it. Make automation your best friend.

- Comparing Yourself to Others: Everyone’s financial situation, income, and life circumstances are unique. Comparing your budget or progress to someone else’s can lead to frustration or unrealistic expectations. Focus on your own journey and celebrate your own progress.

FAQ

Q1: What if my 70% isn’t enough to cover my basic needs?

A: This is a common challenge, especially in high cost-of-living areas. If your 70% doesn’t cover essentials, you have two primary options: increase your income or drastically reduce your expenses. Look for ways to earn more (side hustle, raise, second job) or make significant cuts (downsize housing, sell a car, reduce utility usage, cook every meal at home). In the short term, you might need to temporarily adjust your percentages (e.g., 80/15/5) but make a concrete plan to get back to the 70/20/10 split as soon as possible by addressing the root cause.

Q2: Can I adjust the percentages, like 60/30/10 or 70/15/15?

A: Absolutely! The 70 20 10 is a powerful guideline, but it’s not a rigid law. It’s a starting point designed for broad applicability. If you have aggressive debt to pay off, you might temporarily shift to a 60/30/10 split. If you’re a high earner with low expenses, you might do 50/30/20. The key is to maintain the spirit of the budget: prioritize saving and investing, cover your needs, and manage your wants. Just ensure you’re always allocating a significant portion to your future self (the 20% and 10% combined).

Q3: Should I focus on paying off debt or saving first?

A: A good rule of thumb is to first build a small starter emergency fund (e.g., $1,000-$2,000) so you don’t go further into debt for minor emergencies. After that, prioritize high-interest consumer debt (like credit cards) within your 20% category. The interest rates on these debts often far outweigh any returns you’d get from saving, making them a drag on your financial progress. Once high-interest debt is gone, you can then focus more heavily on building a full emergency fund and investing.

Q4: How often should I review my budget?

A: Ideally, you should review your budget at least once a month. This monthly check-in allows you to see if you’re sticking to your allocations, identify any overspending, and make necessary adjustments for the upcoming month. Quarterly reviews are also beneficial for a broader perspective, especially if you have seasonal expenses or income changes. Consistent review ensures your budget remains relevant and effective for your evolving financial life.

💼 The Money Management Toolkit

Knowledge is power, but proper execution requires the right tools. Getting your financial life organized doesn't have to be overwhelming. These 5 physical management tools are exactly what successful households use to budget, track cash, and secure their most important assets.

📝 Clever Fox Budget Planner & Bill Organizer

The ultimate analog command center for your finances. Sometimes keeping your budget in an app just doesn't stick. Physically writing down your goals, tracking expenses, and planning for debt payoff creates a level of accountability that digital spreadsheets simply can't match.

💵 A6 Leather Cash Stuffing Binder

The viral tool that made the cash-envelope budgeting system popular again. By allocating actual physical cash to designated envelopes (groceries, dining out, fun money), you physically cap your spending, making it virtually impossible to overdraft or overspend.

🔥 Fireproof & Waterproof Document Safe

A critical piece of financial security that many families overlook. Protecting your passports, birth certificates, property deeds, and estate planning documents from disaster is just as important as protecting the money in your bank account.

🏷️ Brother P-Touch Digital Label Maker

The unsung hero of a functional home office. When tax season rolls around or you need to find an important receipt, having perfectly labeled and categorized filing cabinets or accordion folders saves hours of frustrating searches and potential late fees.

🔒 SentrySafe Compact Fireproof Lock Box

For the physical assets that need extra heavy-duty protection—think emergency cash reserves, hard drives with Bitcoin cold wallets, or physical precious metals. This compact, locking safe provides peace of mind that your physical wealth is secure at home.

Conclusion

Congratulations! You’ve just taken a significant step towards mastering your money and building a future filled with financial peace and freedom. The 70 20 10 Budget isn’t just a set of numbers; it’s a philosophy that simplifies personal finance, empowers you with clarity, and provides a clear path to achieving your most ambitious financial goals. By consistently allocating 70% to your needs and wants, dedicating 20% to savings and debt repayment, and committing 10% to giving and long-term investing, you’re creating a robust, balanced financial ecosystem.

Remember, financial success isn’t about perfection; it’s about progress, consistency, and intentional choices. There will be bumps in the road, but with the flexibility and inherent balance of the 70 20 10 Budget, you have a powerful tool to navigate them. Start today by calculating your net income, setting up those crucial automated transfers, and making a conscious effort to align your spending with your values. Embrace the journey, celebrate your wins, and watch as your financial picture transforms from overwhelming to empowering. Your future self will thank you for taking control now!