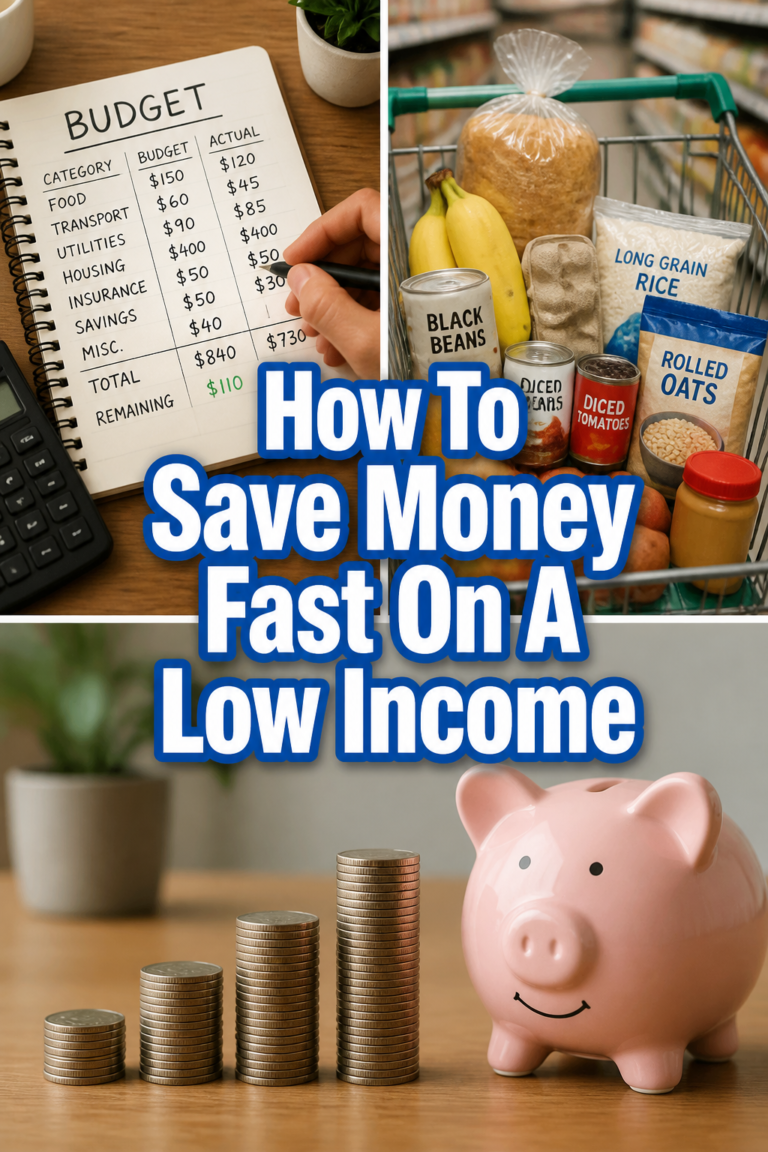

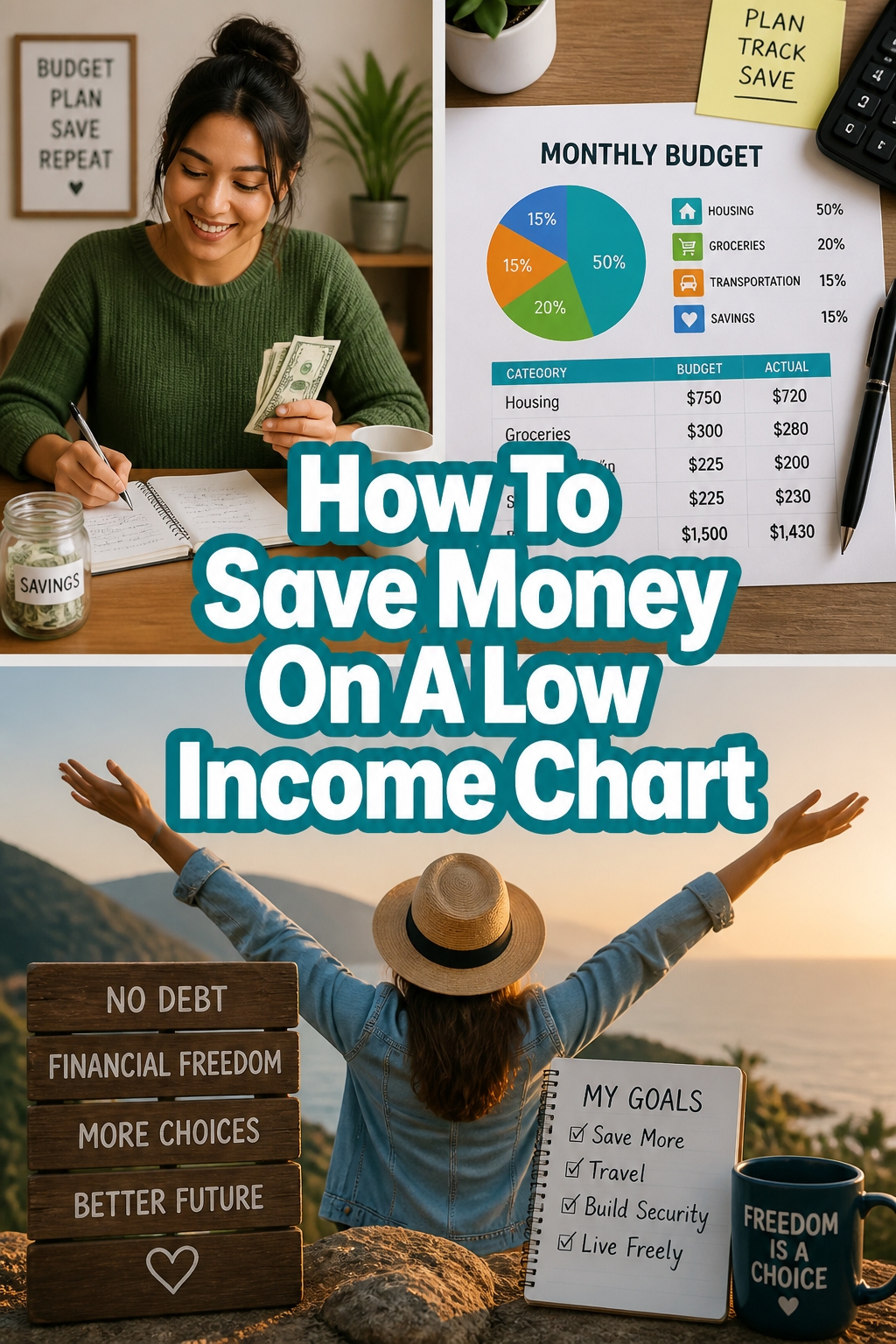

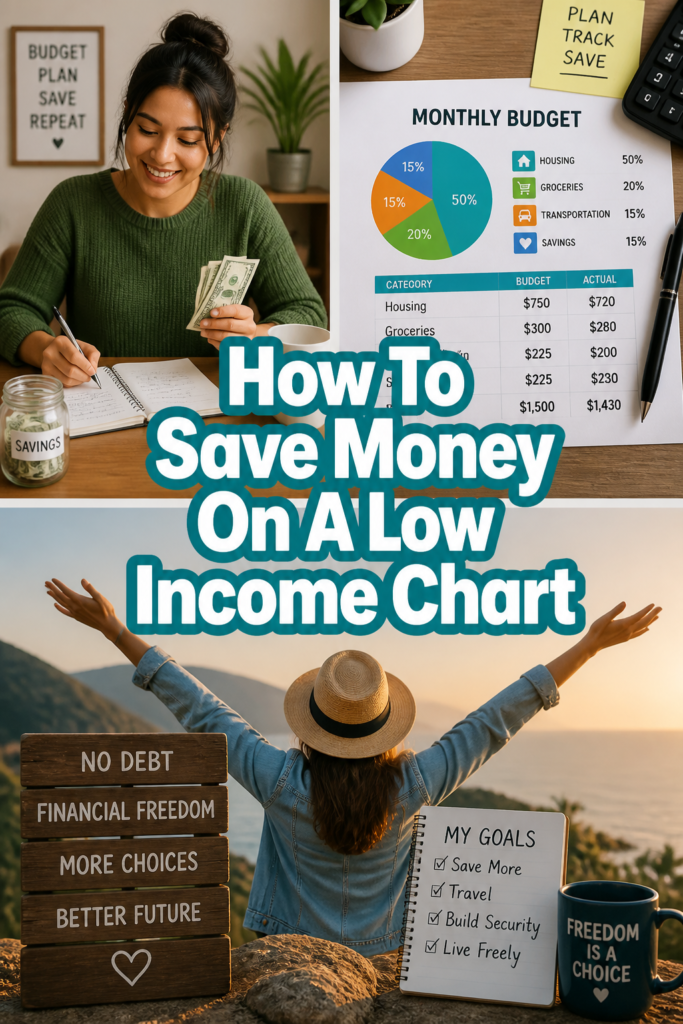

💰 How To Save Money On A Low Income Chart

📚 The Financial Literacy Library

The best investment you can ever make is in your own financial education. These 5 cornerstone books are what millionaires, financial advisors, and wealth-builders universally recommend for completely rewiring how you think about earning, saving, and investing money.

🧠 The Psychology of Money

Doing well with money isn't necessarily about what you know—it's about how you behave. Morgan Housel masterfully breaks down the emotional and psychological biases that secretly dictate our financial decisions, offering a true paradigm shift in how to view wealth.

🏠 Rich Dad Poor Dad

The #1 personal finance book of all time for a reason. This foundational read shatters the myth that you need to earn a high income to be rich, teaching you the critical difference between working for money and making your money work for you via assets.

📈 Atomic Habits

While not strictly a finance book, building wealth is absolutely dependent on the daily habits you cultivate. James Clear provides the definitive framework for breaking bad spending habits and effortlessly automating the good ones that lead to long-term success.

📊 The Simple Path to Wealth

The ultimate antidote to complex, intimidating financial advice. JL Collins provides an incredibly accessible, low-stress roadmap to financial independence through index fund investing, perfectly explaining why simplicity beats Wall Street complexity every time.

💳 I Will Teach You to Be Rich

A tactical, no-BS, 6-week program that actually works. Ramit Sethi teaches you how to crush debt, automate your savings, and negotiate your salary—all while guilt-free spending on the things you truly love. A must-read for modern money management.

It can feel incredibly daunting to think about saving money when your income is already stretched thin.

I remember those days vividly, wondering how I’d even cover basic bills, let alone put something aside for the future.

But I learned that building financial stability isn’t about how much you earn; it’s about smart choices and consistent habits, and I’m here to share what worked for me and countless others.

Quick Overview

This guide will equip you with practical, actionable steps to start saving money, no matter your current income level. You’ll learn how to identify saving opportunities, manage your budget effectively, and cultivate a mindset for financial growth.

- Time needed: 2-3 hours to read and set up initial steps

- Difficulty: Beginner

- What you’ll need: A pen and paper or a digital spreadsheet, bank statements, an open mind

Step-by-Step Instructions

Step 1: Understand Your Current Money Story

Before you can change your financial future, you need to know exactly where you stand today.

This isn’t about judgment; it’s about gathering facts without emotion.

- List all your income sources. Write down every single dollar that comes in each month, from your main job to any side gigs or benefits.

- Track every expense for at least 30 days. This means logging every coffee, every bill, every grocery run. Use an app, a notebook, or a simple spreadsheet.

Pro Tip: Don’t skip the tracking step. It’s often surprising to see where money actually goes versus where you think it goes. This is your personal financial X-ray.

Step 2: Create a Realistic Budget (Your Spending Plan)

A budget isn’t a restriction; it’s a plan that gives you control over your money.

With a low income, every dollar has a job.

- Categorize your expenses from Step 1. Group them into categories like housing, food, transportation, utilities, and personal care.

- Identify fixed expenses (rent, loan payments) and variable expenses (groceries, entertainment). Fixed costs are usually stable, while variable costs can often be adjusted.

- Allocate your income. Assign a specific amount of money to each category for the upcoming month. Make sure your total expenses don’t exceed your total income.

Step 3: Trim the Fat: Finding Savings Opportunities

Once you have your budget, it’s time to look for areas where you can reduce spending without sacrificing your well-being.

Even small cuts add up significantly over time.

- Review your variable expenses first. Can you cook more at home instead of eating out? Are there cheaper alternatives for your entertainment?

- Challenge your fixed expenses. Can you negotiate a lower internet bill? Shop around for cheaper car insurance? These changes can have a big impact.

- Cancel unused subscriptions. Many people pay for services they no longer use or have forgotten about. Check your bank statements carefully.

Pro Tip: Think about the “why” behind your spending. Are you buying things out of habit, boredom, or actual need? Understanding this can help you make more mindful choices.

Step 4: Automate Your Savings, Even Small Amounts

Make saving effortless by setting it up to happen automatically.

This removes the temptation to spend the money before you save it.

- Set up an automatic transfer. Even if it’s just $5 or $10 each payday, transfer it directly from your checking account to a separate savings account.

- Treat savings like a bill. Just like rent or utilities, your savings payment is non-negotiable.

This “pay yourself first” strategy ensures that a portion of your income is always dedicated to your future.

Step 5: Boost Your Income Strategically

When cutting expenses isn’t enough, increasing your income becomes a powerful saving strategy.

Even a small increase can make a big difference.

- Explore side hustles. Think about skills you have that you can monetize, like babysitting, dog walking, freelance writing, or selling crafts online.

- Ask for a raise or seek a higher-paying job. If you’ve been at your current role for a while and perform well, prepare a case for why you deserve more.

- Sell unused items. Declutter your home and turn unwanted items into cash through online marketplaces or local consignment shops.

Step 6: Build an Emergency Fund (Your Safety Net)

An emergency fund is crucial, especially on a low income, to prevent small setbacks from becoming major financial crises.

It keeps you from going into debt when unexpected costs arise.

- Start small. Aim for $500 to $1,000 in a separate, easily accessible savings account. This can cover minor car repairs or unexpected medical bills.

- Prioritize this fund. Before saving for anything else, focus on building this initial safety net.

This fund provides peace of mind and prevents you from dipping into other savings or using high-interest credit cards.

Step 7: Tackle Debt Strategically

High-interest debt can be a major roadblock to saving, as interest payments eat into your available income.

Addressing it is a form of saving.

- List all your debts, including the interest rate and minimum payment for each.

- Focus on high-interest debts first (credit cards, payday loans). Pay as much as you can above the minimum payment on these.

Pro Tip: Consider the “debt snowball” or “debt avalanche” method. Snowball pays smallest balances first for psychological wins. Avalanche pays highest interest rates first to save more money. Choose what motivates you most.

Step 8: Master Meal Planning and Grocery Shopping

Food is one of the biggest variable expenses, offering huge potential for savings.

Smart planning can significantly reduce your grocery bill.

- Plan your meals for the week. Look at what you already have in your pantry and base meals around those ingredients.

- Make a grocery list and stick to it. Avoid impulse purchases by only buying what’s on your list.

- Shop sales and use coupons. Check weekly flyers and digital coupons for deals on staples.

- Cook in bulk. Prepare larger portions of meals and freeze leftovers for quick, cheap meals later.

Step 9: Review and Adjust Regularly

Saving money isn’t a one-time event; it’s an ongoing process.

Life changes, and your budget needs to adapt.

- Schedule monthly check-ins. Review your income, expenses, and savings progress.

- Adjust your budget as needed. Did you overspend in one category? Find ways to cut back next month. Did you have extra income? Allocate it to savings or debt.

This regular review ensures your money plan stays relevant and effective.

Common Mistakes to Avoid

Ignoring Small Expenses

It’s easy to dismiss small, everyday purchases like a daily coffee or a vending machine snack as insignificant. However, these “latte factors” accumulate rapidly.

Over time, these seemingly minor expenses can derail your saving efforts. Be mindful of where every dollar goes, because even small consistent leaks can sink a ship.

Having an Unrealistic Budget

Creating a budget that’s too restrictive or doesn’t account for occasional treats is a recipe for failure. If your budget feels like punishment, you’re less likely to stick to it.

Aim for a budget that is challenging yet sustainable, allowing for some flexibility. A little wiggle room for discretionary spending can prevent burnout and help you stay on track long-term.

Not Tracking Progress

Saving money can feel like a slow grind, especially on a low income, and it’s easy to get discouraged if you don’t see results. Not tracking your progress means you miss out on celebrating small victories.

Regularly reviewing your savings balance and comparing it to your goals provides motivation and helps you identify what’s working and what needs adjustment. Seeing your money grow, even slowly, is incredibly powerful.

Falling for “Get Rich Quick” Schemes

When money is tight, the allure of quick solutions can be strong. However, most “get rich quick” schemes are scams or highly risky ventures that can leave you worse off.

Focus on proven, consistent strategies like budgeting, saving, and increasing your income through legitimate means. Building wealth is a marathon, not a sprint, and it requires patience and discipline.

Troubleshooting

“I Can’t Find Any More Money to Cut!”

If you’ve meticulously reviewed your budget and feel like there’s nothing left to trim, it’s time to shift your focus. Instead of cutting, concentrate on increasing your income.

Look for micro-side hustles that can bring in an extra $50-$100 a month. Even small amounts can kickstart your savings. Consider selling unused items or offering services to neighbors.

“I Keep Dipping into My Savings Account”

This often happens when your emergency fund is too small or non-existent, or if your budget is too restrictive. Ensure your emergency fund is robust enough to cover unexpected expenses.

Also, reassess your budget for areas where you might be depriving yourself too much. Sometimes, allowing a small amount for “fun money” prevents larger, unplanned splurges that deplete savings.

“My Budget Feels Too Complicated and Overwhelming”

If your budgeting method feels like a chore, simplify it. You don’t need fancy software; a simple pen and paper or a basic spreadsheet can work wonders.

Try the 50/30/20 rule as a guideline: 50% needs, 30% wants, 20% savings/debt. Adjust these percentages to fit your low income situation. The goal is to make budgeting easy enough to stick with consistently.

Key Takeaways

- Know Your Numbers: Understand your income and expenses intimately to make informed decisions.

- Budget with Purpose: Create a realistic spending plan that aligns with your financial goals, not just restrictions.

- Automate Savings: Make saving effortless by setting up automatic transfers, even if the amount is small.

- Boost Income: Actively seek ways to increase your earnings, from side hustles to negotiating better pay.

- Build an Emergency Fund: Prioritize a small safety net to prevent debt from unexpected expenses.

- Review and Adjust: Regularly check your progress and adapt your budget as your circumstances change.

Frequently Asked Questions

Is it really possible to save money on a very low income?

Absolutely, yes. While it requires more discipline and creativity, saving on a low income is entirely possible. The key is to start small, be consistent, and focus on both reducing expenses and finding ways to increase your income, even marginally.

What’s the best way to track my spending?

The best way is the one you’ll actually use consistently. This could be a simple notebook and pen, a spreadsheet on your computer, or a budgeting app on your phone. Experiment to find what feels most natural and least burdensome for you.

How much should I aim to save each month?

Start with what you can realistically afford, even if it’s just $5 or $10. The consistency of the habit is more important than the amount at first. As you cut expenses or increase income, gradually challenge yourself to save a bit more. Aim for at least 10% of your income if possible, but any amount is better than none.

Should I save or pay off debt first?

This depends on the type of debt. If you have high-interest debt (like credit cards), it often makes financial sense to focus on paying that down first, as the interest can outweigh savings returns. However, it’s always wise to build a small emergency fund ($500-$1000) before tackling debt aggressively, to prevent new debt from forming due to unexpected expenses.

Our Top Recommended Finds

- Budgeting App (e.g., Mint, YNAB, or a free spreadsheet template): These tools help you track spending, categorize expenses, and visualize your financial situation effortlessly.

- Reusable Water Bottle & Coffee Mug: Small purchases like daily bottled water or takeout coffee add up. Bringing your own saves money and helps the environment.

- Cookbook for Budget Meals: A good cookbook focused on affordable, healthy recipes can inspire you to cook more at home and significantly reduce food costs.

Charting Your Path to Financial Freedom

Saving money on a low income isn’t just about accumulating cash; it’s about building resilience, gaining control, and creating a foundation for a more secure future.

Every small decision you make today contributes to a powerful ripple effect over time. Don’t underestimate the impact of consistent, mindful choices.

You have the power to change your financial narrative. Take the first step today, commit to your plan, and watch your savings grow.