💰 How To Save 3000 In 3 Months Biweekly

📚 The Financial Literacy Library

The best investment you can ever make is in your own financial education. These 5 cornerstone books are what millionaires, financial advisors, and wealth-builders universally recommend for completely rewiring how you think about earning, saving, and investing money.

🧠 The Psychology of Money

Doing well with money isn't necessarily about what you know—it's about how you behave. Morgan Housel masterfully breaks down the emotional and psychological biases that secretly dictate our financial decisions, offering a true paradigm shift in how to view wealth.

🏠 Rich Dad Poor Dad

The #1 personal finance book of all time for a reason. This foundational read shatters the myth that you need to earn a high income to be rich, teaching you the critical difference between working for money and making your money work for you via assets.

📈 Atomic Habits

While not strictly a finance book, building wealth is absolutely dependent on the daily habits you cultivate. James Clear provides the definitive framework for breaking bad spending habits and effortlessly automating the good ones that lead to long-term success.

📊 The Simple Path to Wealth

The ultimate antidote to complex, intimidating financial advice. JL Collins provides an incredibly accessible, low-stress roadmap to financial independence through index fund investing, perfectly explaining why simplicity beats Wall Street complexity every time.

💳 I Will Teach You to Be Rich

A tactical, no-BS, 6-week program that actually works. Ramit Sethi teaches you how to crush debt, automate your savings, and negotiate your salary—all while guilt-free spending on the things you truly love. A must-read for modern money management.

I remember a time when saving even a few hundred dollars felt like climbing Mount Everest.

The idea of hitting a significant financial goal in a short timeframe seemed impossible, yet I discovered practical ways to make it happen.

This guide shares those exact strategies, refined through experience, to help you save $3000 in just three months, paid biweekly.

Quick Overview

This challenge is about transforming your financial habits and seeing tangible results fast.

You’ll learn to identify spending leaks, create a powerful budget, and boost your savings with intentional actions.

- Time needed: 3 months (6 biweekly pay periods)

- Difficulty: Intermediate

- What you’ll need: A clear budget, a separate savings account, discipline, and a positive, proactive mindset.

Step-by-Step Instructions

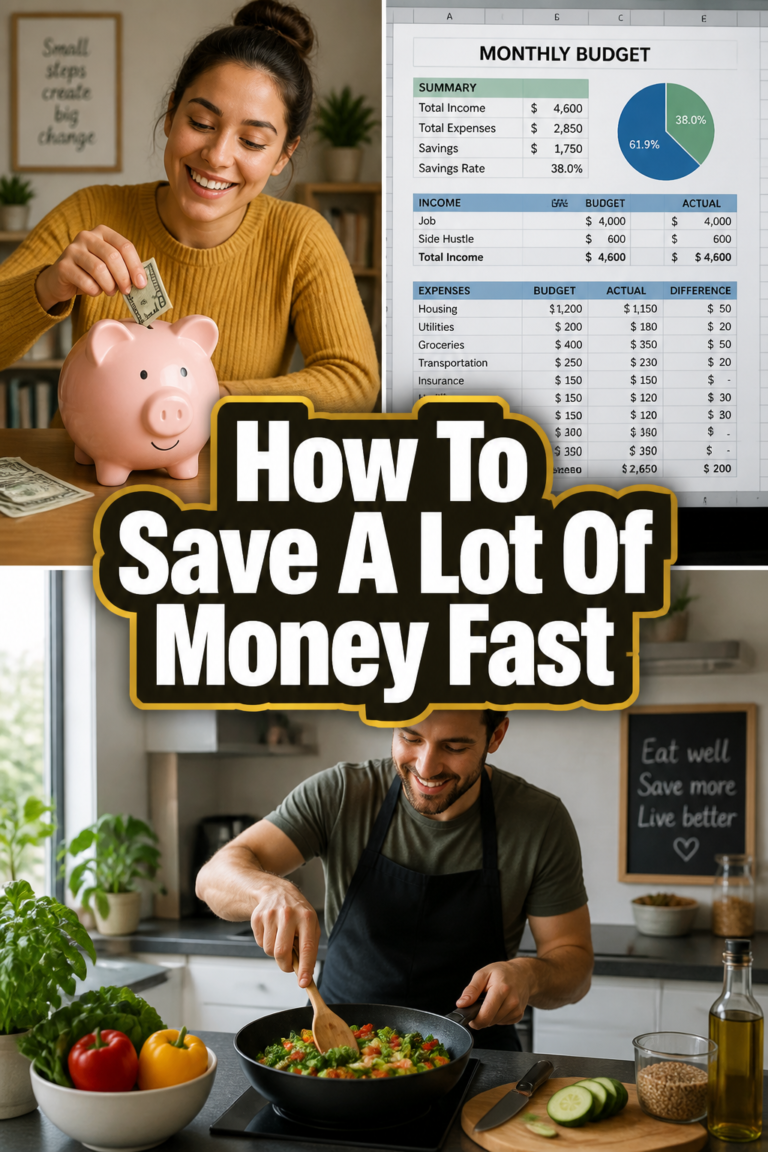

Step 1: Calculate Your Target Biweekly Savings

The first step is to clearly understand the numbers. You need to save $3000 over three months, which translates to six biweekly paychecks.

This means you’ll need to set aside $500 from each biweekly paycheck to reach your goal.

Knowing this exact figure makes the goal concrete and manageable.

Pro Tip: Write this $500 figure down somewhere visible, like on your fridge or computer monitor. Visual reminders reinforce your commitment.

Step 2: Audit Your Current Spending Habits

Before you can cut expenses, you need to know where your money is currently going. For the next two weeks, track every single dollar you spend.

Use a budgeting app, a simple spreadsheet, or even a small notebook to record all transactions.

This audit reveals your true spending patterns, often highlighting areas you didn’t realize were costing you so much.

Step 3: Create a Lean, Goal-Focused Budget

Now that you know your spending, it’s time to build a budget that prioritizes your $500 biweekly savings goal. Allocate your $500 savings first, right after your essential bills.

Then, strategically cut back on non-essential categories like dining out, entertainment, and subscriptions.

Every dollar saved here directly contributes to your $3000 goal.

Step 4: Automate Your Biweekly Savings Transfer

The easiest way to ensure you hit your target is to make saving automatic. Set up an automatic transfer of $500 from your checking account to a separate savings account every time you get paid.

This “pay yourself first” strategy removes the temptation to spend the money and builds consistency.

Treat this transfer like a non-negotiable bill.

Step 5: Boost Your Income Creatively

Sometimes cutting expenses isn’t enough, or you want to accelerate your progress. Look for ways to earn extra money.

Consider selling unused items around your home, taking on freelance gigs, or picking up a few extra shifts if possible.

Even small amounts of extra income can make a significant difference towards your $3000.

Pro Tip: Dedicate any extra income you earn entirely to your savings goal. This money becomes “bonus” savings that can help you exceed your target or provide a buffer.

Step 6: Implement Strategic Spending Cuts

With your budget in place, it’s time to make intentional cuts. Identify specific areas where you can reduce spending without feeling completely deprived.

Perhaps you can pack your lunch instead of buying it, brew coffee at home, or swap expensive outings for free activities.

Small, consistent cuts add up quickly over three months.

Step 7: Track Your Progress and Stay Motivated

Seeing your savings grow is incredibly motivating. Regularly check your savings account balance and track how close you are to your $3000 goal.

Consider using a visual tracker, like a thermometer chart, to mark your progress after each biweekly transfer.

Celebrate small milestones, like hitting $1000 or $2000, to keep your spirits high.

Step 8: Re-evaluate and Adjust as Needed

Life happens, and your budget might need tweaks. Review your spending and savings plan after the first month.

If you’re finding it too difficult, identify areas for further adjustment or consider additional income streams.

Flexibility is key to long-term success, even in a short-term challenge.

Common Mistakes to Avoid

Not Being Realistic

A common pitfall is creating a budget that is too restrictive, leading to quick burnout. Trying to cut every single non-essential expense can feel overwhelming and unsustainable.

Instead, identify a few key areas where you can make significant, yet manageable, reductions. Allow yourself small, planned indulgences to prevent feeling deprived.

Ignoring Small Expenses

Many people focus on large bills but overlook the cumulative impact of small, daily purchases. A daily coffee, a snack from the convenience store, or frequent online impulse buys can quickly derail your progress.

These “small leaks” in your budget add up significantly over three months. Pay attention to every dollar, as even small changes here can free up substantial funds.

Lack of Accountability

Trying to save a large sum alone can be tough. Without someone to share your goals with or a system to keep you on track, it’s easy to slip.

Tell a trusted friend or family member about your goal, or find an online community. Even just regularly reviewing your own progress acts as a form of self-accountability.

Troubleshooting

Falling Off Track with Spending

It’s easy to overspend occasionally, especially when feeling stressed or celebratory. If you find yourself deviating from your budget, don’t give up entirely.

Acknowledge the slip, then immediately get back on track with your next paycheck. Adjust your spending in the following period to compensate if possible, but most importantly, recommit to your goal.

Unexpected Expenses Arise

Life is unpredictable, and emergencies can happen. If an unexpected cost eats into your planned savings, take a deep breath.

Assess if you can temporarily reduce your savings transfer for just one biweekly period, or if you need to find an additional income source to cover the gap. Prioritize essential needs, then get back to your savings plan as soon as you can.

Feeling Deprived or Unmotivated

Saving aggressively can sometimes feel like a sacrifice, leading to a lack of motivation. Remind yourself of the “why” behind your $3000 goal, whether it’s for an emergency fund, a down payment, or a special purchase.

Revisit your budget to see if there’s a small, guilt-free treat you can allow yourself, or plan a free activity you truly enjoy. Sometimes, a mental break from strict saving can re-energize your efforts.

Key Takeaways

- Automate Your Savings: Set up biweekly transfers to ensure consistent progress toward your $3000 goal.

- Know Your Numbers: Understand that you need to save $500 from each biweekly paycheck.

- Track Everything: Monitor your income and expenses rigorously to identify and eliminate spending leaks.

- Boost Income: Actively seek opportunities to earn extra money and dedicate it to your savings.

- Stay Flexible: Be prepared to adjust your budget and strategy as unexpected situations arise.

- Celebrate Progress: Acknowledge milestones to maintain motivation throughout the three months.

Frequently Asked Questions

Is saving $3000 in 3 months truly realistic?

Yes, it is absolutely realistic for many people, especially with a biweekly pay schedule. It requires dedication and intentional effort, but by following these steps, you create a clear path to achieve it. Many individuals successfully meet similar aggressive savings goals.

What if I don’t get paid biweekly?

The principles remain the same regardless of your pay schedule. Simply adjust the target amount to match your pay frequency. For example, if you’re paid monthly, you’d aim to save $1000 per month for three months. The key is consistent, automated saving.

Should I use a separate savings account for this goal?

Absolutely. A separate savings account makes it much harder to accidentally spend your dedicated savings. It also provides a clear visual of your progress and helps mentally separate your goal money from your everyday spending funds.

Can I still have fun and save aggressively?

Yes, you can. The key is intentionality. Instead of spontaneous, expensive outings, plan free or low-cost activities. Focus on experiences over material purchases, and look for deals. A lean budget doesn’t mean no fun, it means smarter fun.

Your Journey to Financial Confidence Starts Now

Saving $3000 in three months biweekly is more than just hitting a number; it’s about building financial muscle.

You’ll gain invaluable skills in budgeting, self-discipline, and resourcefulness that will serve you well for years to come.

This challenge is a powerful stepping stone towards achieving even bigger financial dreams.

Start today by reviewing your last paycheck and identifying one small expense you can cut. Your future self will thank you for taking action.

Our Top Recommended Finds

- Budgeting Planner & Journal: A physical planner helps you visualize your budget, track expenses, and stay organized without screen time.

- Reusable Coffee Mug & Water Bottle: Significantly cut down on daily coffee shop expenses and single-use plastic, saving money and helping the environment.

- Library Card: Access books, movies, and events for free, replacing costly entertainment subscriptions and purchases.