💰 How To Be Frugal

📚 The Financial Literacy Library

The best investment you can ever make is in your own financial education. These 5 cornerstone books are what millionaires, financial advisors, and wealth-builders universally recommend for completely rewiring how you think about earning, saving, and investing money.

🧠 The Psychology of Money

Doing well with money isn't necessarily about what you know—it's about how you behave. Morgan Housel masterfully breaks down the emotional and psychological biases that secretly dictate our financial decisions, offering a true paradigm shift in how to view wealth.

🏠 Rich Dad Poor Dad

The #1 personal finance book of all time for a reason. This foundational read shatters the myth that you need to earn a high income to be rich, teaching you the critical difference between working for money and making your money work for you via assets.

📈 Atomic Habits

While not strictly a finance book, building wealth is absolutely dependent on the daily habits you cultivate. James Clear provides the definitive framework for breaking bad spending habits and effortlessly automating the good ones that lead to long-term success.

📊 The Simple Path to Wealth

The ultimate antidote to complex, intimidating financial advice. JL Collins provides an incredibly accessible, low-stress roadmap to financial independence through index fund investing, perfectly explaining why simplicity beats Wall Street complexity every time.

💳 I Will Teach You to Be Rich

A tactical, no-BS, 6-week program that actually works. Ramit Sethi teaches you how to crush debt, automate your savings, and negotiate your salary—all while guilt-free spending on the things you truly love. A must-read for modern money management.

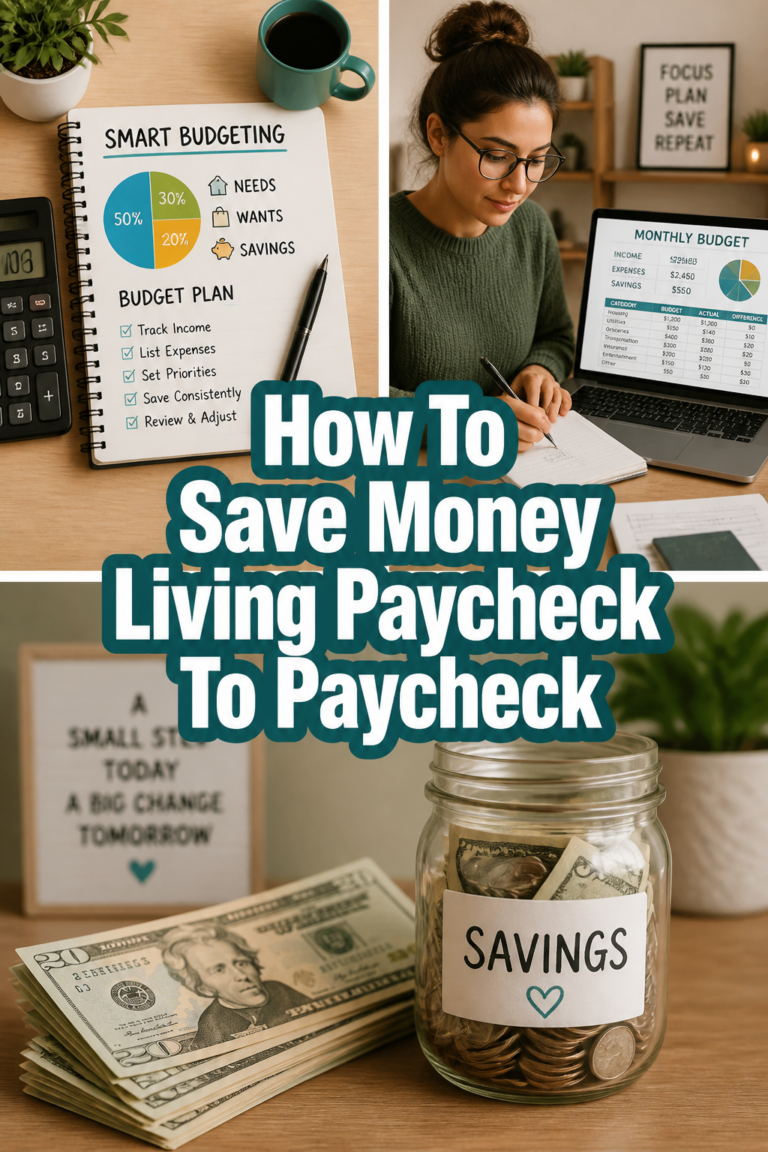

Ever feel like your money vanishes before you even understand where it went? Or that achieving your financial dreams, like buying a home, traveling the world, or retiring early, feels like an impossible uphill battle? The truth is, mastering your money isn’t about earning a million dollars overnight; it’s about making smart, intentional choices with every dollar you have. This guide will show you how to embrace frugality not as a restrictive chore, but as an empowering lifestyle that unlocks financial freedom and peace of mind.

Quick Overview

This comprehensive guide will equip you with the mindset and practical strategies to take control of your finances, reduce unnecessary spending, and build a solid foundation for your financial future. You’ll learn how to identify your spending patterns, optimize your budget, and implement sustainable saving habits that genuinely make a difference.

Time needed: Initial setup (1-2 hours); ongoing practice (30 mins/week)

Difficulty: Beginner

What you’ll need: A pen and paper or a digital spreadsheet, access to your bank statements, and an open mind!

Step-by-Step Instructions

Step 1: Discover Your “Why” and Uncover Your Spending Habits

Before you can change your financial trajectory, you need to understand two crucial things: why you want to be frugal, and where your money is currently going. Your “why” is your motivation – whether it’s to pay off debt, save for a down payment, retire early, or simply reduce financial stress. This personal anchor will keep you motivated when challenges arise.

Next, it’s time for a financial autopsy. Gather your bank statements, credit card bills, and any cash receipts from the last 1-3 months. Categorize every single expense. Don’t judge, just observe. You might be surprised by how much you spend on things you barely remember, like daily coffees, forgotten subscriptions, or impulse buys. This exercise isn’t about shame; it’s about gaining clarity and identifying “money leaks.”

Pro tip: Use a spreadsheet, a budgeting app (like Mint, YNAB, or Personal Capital), or even just a notebook to meticulously track every dollar. Seeing the numbers in black and white is often the most powerful catalyst for change. Be honest with yourself about discretionary spending versus true necessities.

Step 2: Craft a Realistic and Empowering Budget

A budget isn’t a straitjacket; it’s a roadmap to your financial goals. Based on your spending audit from Step 1, create a budget that allocates every dollar of your income. The goal is to ensure your income exceeds your expenses, leaving room for savings and investments. A popular method is the 50/30/20 rule:

- 50% for Needs: Housing, utilities, groceries, transportation, insurance, minimum loan payments.

- 30% for Wants: Dining out, entertainment, hobbies, travel, shopping, subscriptions (beyond essentials).

- 20% for Savings & Debt Repayment: Emergency fund, retirement, investments, extra debt payments.

Adjust these percentages to fit your unique situation, but always prioritize savings and debt repayment. Be realistic about your “wants” to avoid feeling deprived, which can lead to budget burnout. The key is to find a balance that feels sustainable and empowering, not restrictive.

Pro tip: Start with a “zero-based budget” where every dollar has a job. This ensures you’re intentional with your money. If you have variable income, budget for your lowest expected income and save any extra. Review and adjust your budget monthly; life happens, and your budget should be flexible enough to accommodate changes.

Step 3: Optimize Your Housing and Utility Costs

For most people, housing is the single largest expense. Significant savings here can dramatically impact your financial health.

- Housing: If you own, explore refinancing options for a lower interest rate. If you rent, consider negotiating your lease renewal, finding a roommate, or even moving to a more affordable area when your lease is up. Could you downsize? Rent out a spare room on Airbnb?

- Utilities: Be mindful of your energy consumption. Unplug electronics when not in use (phantom load), use smart thermostats, switch to energy-efficient light bulbs (LEDs), and take shorter showers. Compare providers for internet, cable, and phone services regularly; loyalty rarely pays off. Call your current providers to see if they can match competitor offers.

These changes might require a bit of effort upfront, but the recurring monthly savings can be substantial, freeing up hundreds of dollars over a year.

Pro tip: Schedule an annual “utility audit.” Go through all your utility bills (electricity, gas, water, internet, phone) and see if you can find cheaper plans, bundles, or ways to reduce usage. Even small adjustments compound over time.

Step 4: Master Mindful Grocery Shopping and Home Cooking

Food is another major expense that offers fertile ground for frugality. Eating out frequently, convenience foods, and food waste can quickly deplete your budget.

- Meal Planning: Plan your meals for the week, create a precise grocery list, and stick to it. This prevents impulse buys and ensures you use what you buy.

- Shop Smart: Buy in bulk for non-perishables when items are on sale. Compare unit prices. Opt for store brands, which are often just as good as name brands but cheaper. Shop seasonal produce, which is typically less expensive and fresher.

- Reduce Waste: Learn to store food properly to extend its shelf life. Repurpose leftovers into new meals. Embrace “ugly” produce, which is often discounted. Compost food scraps if possible.

- Cook at Home: Cooking your own meals is almost always cheaper and healthier than eating out. Pack lunches and snacks for work or school. Learn a few basic, versatile recipes that use inexpensive ingredients.

Pro tip: Never shop on an empty stomach – hunger leads to impulse buys. Also, check your pantry and fridge before you shop to avoid buying duplicates. Consider doing a “pantry challenge” where you commit to eating only what you already have for a week or two to clear out forgotten items and save money.

Step 5: Rethink Transportation and Commuting

The cost of getting around can be a significant drain on your finances, especially if you own a car.

- Public Transport/Biking/Walking: If feasible, explore alternatives to driving. Public transportation passes are often much cheaper than gas, insurance, and maintenance. Biking or walking offers health benefits and is completely free.

- Car Maintenance: If you must drive, stay on top of regular maintenance to prevent costly repairs down the road. Shop around for cheaper car insurance rates annually.

- Fuel Efficiency: Drive smarter – avoid aggressive acceleration and braking. Carpool with colleagues or friends. Combine errands into one trip to reduce mileage.

- Consider Downsizing: Could you sell a second car you rarely use? Or trade in an expensive vehicle for a more fuel-efficient, reliable, and affordable one? The total cost of car ownership (depreciation, insurance, fuel, maintenance) is often underestimated.

Pro tip: Use apps like GasBuddy to find the cheapest gas prices in your area. If you live in an urban area, evaluate if owning a car is truly necessary. The money saved from car payments, insurance, gas, and parking could be substantial and redirected towards your financial goals.

Step 6: Ruthlessly Cut Unnecessary Subscriptions and Services

In the age of digital convenience, it’s easy to accumulate a pile of recurring subscriptions you barely use. These “money leaks” can add up to hundreds of dollars annually.

- Audit Your Subscriptions: Go through your bank and credit card statements and list every recurring charge. This includes streaming services (Netflix, Hulu, Spotify), gym memberships, software subscriptions, app subscriptions, and even delivery services.

- Eliminate the Unused: Cancel anything you don’t use regularly or don’t derive significant value from. Be honest with yourself. Do you really need three streaming services and a gym membership you never use?

- Downgrade or Bundle: For services you do use, can you downgrade to a cheaper plan? Or bundle services for a discount? Share family plans where appropriate (e.g., streaming services with family members).

- Library Cards: Don’t forget the power of your local library! You can often borrow books, movies, audiobooks, and even digital magazines for free, replacing costly entertainment subscriptions.

Pro tip: Set a calendar reminder to review your subscriptions every six months. Companies often raise prices, and your usage habits might change. Many banks and apps now offer tools to help you identify and manage recurring payments.

Step 7: Embrace DIY, Second-Hand, and Resourcefulness

Frugality isn’t just about cutting expenses; it’s about being resourceful and making the most of what you have.

- DIY (Do It Yourself): Learn basic home repairs, cooking, cleaning, and gardening. Instead of paying for services, try to do it yourself. Watch YouTube tutorials for almost anything! This saves money and builds valuable skills.

- Second-Hand Treasures: For clothing, furniture, books, and even electronics, explore thrift stores, consignment shops, garage sales, Facebook Marketplace, and online classifieds (e.g., Craigslist, eBay). You can find high-quality items at a fraction of the cost of new.

- Borrow and Share: Instead of buying tools or equipment you’ll only use once, borrow them from friends, family, or a local tool library. Consider sharing resources like lawnmowers or pressure washers with neighbors.

- Repair, Don’t Replace: Before buying something new, ask if the old item can be repaired. A little glue, a stitch, or a spare part can often extend the life of an item significantly.

Pro tip: Before making any purchase, implement the “30-day rule.” If it’s not an essential item, wait 30 days. Often, the urge to buy passes, or you find a better, cheaper alternative. This helps curb impulse spending and gives you time to consider if the purchase truly adds value.

Step 8: Automate Savings and Invest for the Future

Once you’ve trimmed your expenses, the next crucial step is to ensure those savings are put to work for you. Frugality isn’t just about saving money; it’s about using that saved money to build wealth.

- Automate Your Savings: Set up automatic transfers from your checking account to your savings account (and investment accounts) every payday. Treat savings as a non-negotiable “bill.” Even small, consistent transfers add up significantly over time due to compounding.

- Build an Emergency Fund: Aim for 3-6 months’ worth of essential living expenses in an easily accessible, high-yield savings account. This fund acts as a financial safety net, preventing you from going into debt when unexpected costs arise.

- Invest for Growth: Once your emergency fund is solid, start investing. Contribute to retirement accounts like a 401(k) (especially if your employer offers a match – that’s free money!), an IRA, or a Roth IRA. Explore low-cost index funds or ETFs. Even modest investments, made consistently, can grow substantially over decades.

- Educate Yourself: Read books, listen to podcasts, and follow reputable financial blogs to deepen your understanding of investing, debt management, and wealth building. The more you know, the more confident you’ll be in making smart financial decisions.

Pro tip: Pay yourself first. This means setting aside money for savings and investments before you pay any other bills or spend on discretionary items. This psychological shift is incredibly powerful and ensures your financial future is a priority. Review your investment performance and adjust your strategy periodically, but avoid frequent tinkering based on market fluctuations.

Common Mistakes to Avoid

Embarking on a frugal journey is exciting, but it’s easy to stumble into common pitfalls. Here’s how to navigate them:

-

The Deprivation Mindset: Thinking of frugality as “doing without” rather than “doing with less but better.” This leads to burnout and giving up.

Correct Approach: Frame frugality as choosing intentionally. Focus on the value you gain (financial freedom, peace of mind) rather than what you’re “losing.” Allow for occasional, budgeted splurges to keep motivation high. -

Ignoring Small Leaks: Focusing only on big expenses while letting small, daily costs (like a daily coffee or vending machine snacks) go unchecked. These “latte factors” add up to significant amounts over time.

Correct Approach: Track all your spending, no matter how small. Use a budgeting app or a simple notebook for a few weeks to identify these subtle drains. You might be surprised. -

Not Tracking Progress: Setting a budget and making changes, but never checking back to see if they’re working or if you’re sticking to them.

Correct Approach: Review your budget and spending regularly (weekly or bi-weekly). Celebrate small wins, identify areas for improvement, and adjust your plan as needed. Seeing your savings grow is a huge motivator. -

Falling for “Frugal Traps”: Buying something you don’t truly need just because it’s on sale or you perceive it as a “good deal.”

Correct Approach: Always ask yourself, “Do I need this? Do I have something similar? Will this add value to my life?” A “deal” is only a deal if you were going to buy the item anyway. Prioritize needs over wants, regardless of the discount. -

Going It Alone: Not involving your partner or family in your financial goals, leading to friction or undermining efforts.

Correct Approach: Have open, honest conversations with your household members about your financial goals and how frugality will help achieve them. Get everyone on board and make it a shared journey, understanding that collective effort yields greater results.

Troubleshooting

Even with the best intentions, you might encounter bumps in the road. Here are solutions to common issues:

-

“I feel overwhelmed and discouraged.”

Solution: Frugality is a marathon, not a sprint. Don’t try to change everything at once. Pick one or two areas (e.g., groceries, subscriptions) to focus on for a month. Once those habits are solid, move on to the next. Celebrate small victories and remind yourself of your “why.” -

“I keep overspending in certain categories.”

Solution: Your budget might be too restrictive or unrealistic in that category. Adjust the allocation. If it’s a “want” category, consider setting up an “envelope system” (physical or digital) where you only spend the cash allocated for that specific item. If the money runs out, you stop spending in that category until the next budget cycle. -

“Social pressure makes it hard to be frugal.”

Solution: Be honest with your friends and family about your financial goals without making them feel guilty. Suggest frugal alternatives for social outings (e.g., potlucks, free park visits, coffee at home before an event). True friends will understand and support your journey. Remember, your financial well-being is more important than keeping up appearances.

Key Takeaways

- Frugality is about intentional spending and living within your means to achieve financial freedom.

- Understanding your “why” is crucial for long-term motivation.

- A realistic budget is your roadmap; track your spending meticulously.

- Prioritize big-impact savings like housing, utilities, and transportation.

- Mastering grocery shopping and home cooking offers significant daily savings.

- Regularly audit and cut unnecessary subscriptions and services.

- Embrace resourcefulness: DIY, second-hand, borrowing, and repairing.

- Automate your savings and invest consistently to build wealth over time.

- Avoid deprivation, track progress, and don’t fall for “frugal traps.”

Frequently Asked Questions

Here are some common questions people have about adopting a frugal lifestyle:

-

Is frugality just about being cheap?

Not at all! Frugality is about valuing your money and making smart choices that align with your long-term goals. Being “cheap” often implies sacrificing quality or value for the lowest price, sometimes at the expense of others. Frugality is about maximizing value, minimizing waste, and being intentional with every dollar you spend, not just hoarding money. -

How long does it take to see results?

You can start seeing small results immediately, especially if you cut unnecessary subscriptions or reduce impulse buys. Significant results, like paying off debt or building a substantial emergency fund, take consistent effort over months or even a few years. The key is consistency and patience. -

Can I still have fun while being frugal?

Absolutely! Frugality isn’t about eliminating fun; it’s about finding fun in smarter, often more creative ways. This might mean exploring free local events, having potlucks with friends, enjoying nature, or pursuing hobbies that don’t cost a fortune. Many frugal activities (like cooking at home or outdoor adventures) can be incredibly enjoyable and fulfilling. -

What’s the difference between frugality and minimalism?

While they often overlap, frugality focuses on saving money and optimizing spending to achieve financial goals. Minimalism, on the other hand, is a lifestyle choice centered on intentionally living with less to reduce clutter, stress, and consumerism, often for environmental or mental well-being reasons. You can be frugal without being a minimalist, and vice versa, though many find they complement each other well.

What’s Next?

Congratulations on taking the first steps toward a more financially empowered life! Frugality is a journey, not a destination. To continue building on this momentum:

- Deep Dive into Debt: If you have high-interest debt, research strategies like the debt snowball or debt avalanche methods to accelerate repayment.

- Explore Passive Income: Once your finances are stable, consider ways to earn extra income, such as starting a side hustle, investing in dividend stocks, or real estate.

- Educate Your Loved Ones: Share what you’ve learned with your family and friends. Financial literacy is a gift everyone deserves.

Remember, every small, intentional choice you make today paves the way for a more secure and abundant tomorrow. Don’t wait for “someday” – start making those money-smart decisions right now!