💰 How To Make Extra Money To Pay Off Debt

📚 The Financial Literacy Library

The best investment you can ever make is in your own financial education. These 5 cornerstone books are what millionaires, financial advisors, and wealth-builders universally recommend for completely rewiring how you think about earning, saving, and investing money.

🧠 The Psychology of Money

Doing well with money isn't necessarily about what you know—it's about how you behave. Morgan Housel masterfully breaks down the emotional and psychological biases that secretly dictate our financial decisions, offering a true paradigm shift in how to view wealth.

🏠 Rich Dad Poor Dad

The #1 personal finance book of all time for a reason. This foundational read shatters the myth that you need to earn a high income to be rich, teaching you the critical difference between working for money and making your money work for you via assets.

📈 Atomic Habits

While not strictly a finance book, building wealth is absolutely dependent on the daily habits you cultivate. James Clear provides the definitive framework for breaking bad spending habits and effortlessly automating the good ones that lead to long-term success.

📊 The Simple Path to Wealth

The ultimate antidote to complex, intimidating financial advice. JL Collins provides an incredibly accessible, low-stress roadmap to financial independence through index fund investing, perfectly explaining why simplicity beats Wall Street complexity every time.

💳 I Will Teach You to Be Rich

A tactical, no-BS, 6-week program that actually works. Ramit Sethi teaches you how to crush debt, automate your savings, and negotiate your salary—all while guilt-free spending on the things you truly love. A must-read for modern money management.

Feeling weighed down by debt can be incredibly stressful, a constant hum of worry in the background.

I’ve been there, staring at statements and wondering how to ever get ahead.

This guide shares the exact strategies I used to find extra cash and tackle my debt head-on, giving you a clear path to financial freedom.

Quick Overview

This guide will equip you with practical steps and a resilient mindset to earn more and pay off your debt faster.

You’ll discover how to identify income opportunities, optimize your spending, and build lasting financial habits.

- Time needed: 4-6 hours (initial setup & strategy), ongoing commitment for results

- Difficulty: Beginner

- What you’ll need: A pen and paper or spreadsheet, internet access, a clear mind, and a strong desire for change

Step-by-Step Instructions

Step 1: Get Crystal Clear on Your Debt & Budget

Before you can make extra money to pay off debt, you need to understand your current financial landscape.

Knowledge is power here, so gather all your statements for credit cards, loans, and any other outstanding balances.

- List every single debt you have, noting the outstanding balance, interest rate, and minimum monthly payment.

- Create a detailed budget that tracks all your income and expenses. This shows you exactly where your money goes.

- Identify areas where you can cut back, even temporarily, to free up cash for debt payments.

Pro Tip: Use a simple spreadsheet or a budgeting app like YNAB (You Need A Budget) to get a true picture of your finances. Seeing the numbers clearly helps with motivation.

Step 2: Slash Unnecessary Spending (The Quick Wins)

Finding extra money doesn’t always mean earning more; sometimes it means spending less.

Look for immediate areas where you can reduce your outflow without sacrificing your quality of life too much.

- Cancel unused subscriptions, from streaming services to gym memberships you rarely visit.

- Cook more meals at home instead of eating out. This can save hundreds of dollars each month.

- Review your utility bills and look for ways to conserve energy or switch to cheaper providers.

- Pause non-essential shopping for a set period, like a “no-spend month,” to jumpstart your savings.

Step 3: Dive into the Gig Economy & Side Hustles

This is where you actively start bringing in new money beyond your main job.

The gig economy offers countless opportunities to leverage your skills or time for extra cash.

- Offer freelance services based on your professional skills, such as writing, graphic design, web development, or virtual assistance. Platforms like Upwork or Fiverr can connect you with clients.

- Drive for rideshare companies like Uber or Lyft during evenings or weekends.

- Deliver food with services such as DoorDash, Uber Eats, or Grubhub.

- Walk dogs or pet-sit through apps like Rover.

- Tutor students online or in person if you have expertise in a particular subject.

Pro Tip: Start small with one or two side hustles that fit your schedule. As you gain confidence and see results, you can expand your efforts.

Step 4: Monetize Your Possessions (Declutter & Earn)

Look around your home; chances are you have items gathering dust that could be converted into cash.

Selling unused items is a fantastic way to quickly inject money into your debt repayment plan.

- Sell old electronics, furniture, or designer clothes on platforms like Facebook Marketplace, eBay, or Poshmark.

- Host a garage sale or participate in a community yard sale to clear out multiple items at once.

- Consign gently used clothing or accessories at local consignment shops.

- Rent out a spare room or your entire home for short periods on Airbnb if local regulations allow.

Step 5: Leverage Your Skills for Local Opportunities

Sometimes the best opportunities are right in your neighborhood.

Think about services people commonly need and how you can provide them.

- Offer lawn care, snow removal, or gardening services to neighbors.

- Provide handyman services if you’re skilled with home repairs.

- Babysit for busy parents in your community.

- Clean houses or run errands for elderly neighbors.

- Teach a skill you possess, such as playing an instrument or a foreign language.

Step 6: Optimize Your Main Income Stream

While side hustles are great, don’t forget about your primary source of income.

Sometimes, a little effort here can yield significant results.

- Ask for a raise at your current job if you haven’t had one recently and have taken on more responsibility.

- Negotiate a higher salary if you’re offered a new position elsewhere.

- Take on extra shifts or overtime if available and you have the capacity.

- Seek out bonuses or performance incentives within your role.

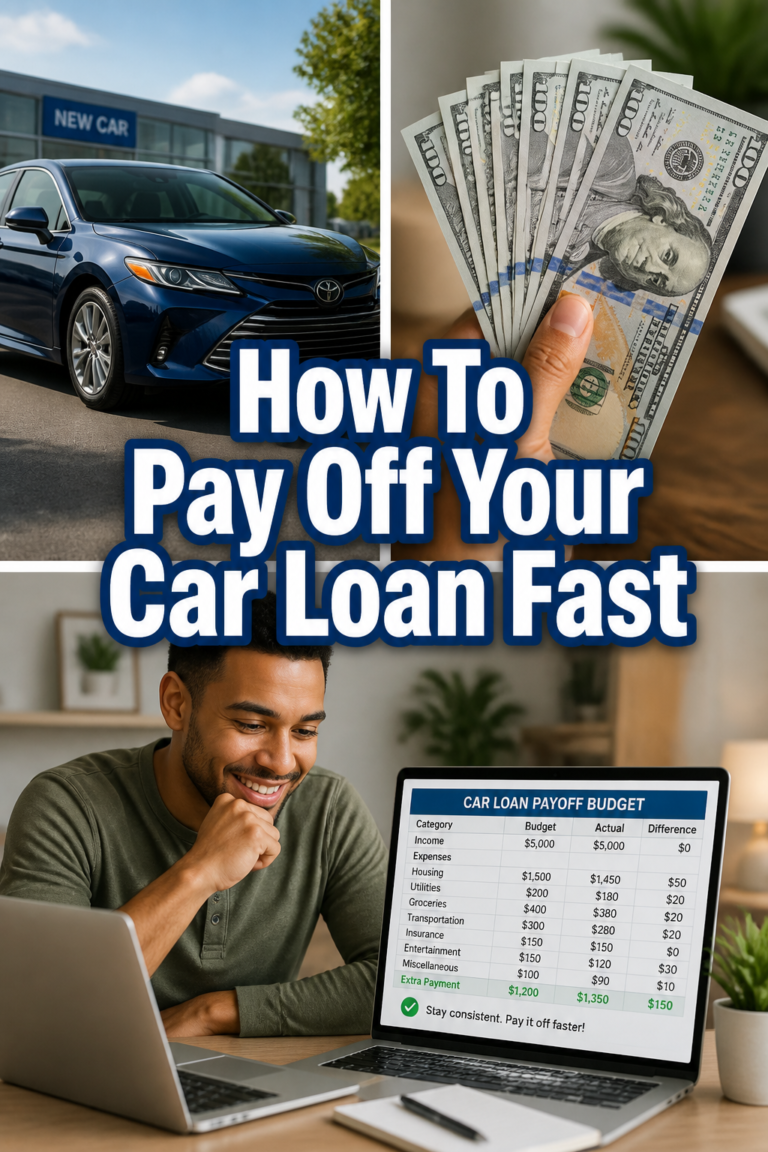

Step 7: Implement a Debt Repayment Strategy

Once you start generating extra money, direct it strategically towards your debt.

Having a clear plan will keep you motivated and maximize your progress.

- Choose the “debt snowball” method: pay minimums on all debts, but put all extra money towards the smallest debt first. Once that’s paid, roll its payment into the next smallest.

- Consider the “debt avalanche” method: pay minimums on all debts, but put all extra money towards the debt with the highest interest rate first. This saves you more money on interest in the long run.

- Automate your extra payments as soon as your income comes in. This prevents you from accidentally spending the money.

Step 8: Stay Consistent & Celebrate Milestones

Paying off debt is a marathon, not a sprint.

Consistency is key, and acknowledging your progress will help you stay motivated.

- Review your budget and debt progress weekly or monthly to stay on track.

- Set small, achievable goals and reward yourself (non-monetarily) when you hit them.

- Connect with others on a similar journey for support and accountability.

- Remind yourself of your “why” – the freedom and peace of mind you’ll gain.

Common Mistakes to Avoid

Burning Out Too Quickly

It’s easy to get excited and try to do too much too fast. Taking on too many side hustles or working excessive hours can lead to exhaustion and giving up altogether.

Instead, start with one or two manageable activities. Gradually increase your efforts as you adapt, ensuring you maintain a sustainable pace for the long haul.

Ignoring Your Budget

Making extra money is only half the battle; knowing where it goes is the other. Many people earn more but then allow their spending to creep up, negating their efforts.

Consistently track your income and expenses. Ensure every extra dollar you earn is intentionally directed towards your debt, not absorbed by new wants or needs.

Not Having a Clear Debt Plan

Just throwing extra money at debt without a strategy can feel overwhelming and less effective. Without a plan, you might not see the progress needed to stay motivated.

Decide on either the debt snowball or avalanche method and stick to it. This focused approach provides clear milestones and helps you see your debt diminish systematically.

Forgetting an Emergency Fund

While paying off debt is crucial, completely neglecting an emergency fund can be risky. Life happens, and unexpected expenses can force you back into debt.

Aim to save a small starter emergency fund, perhaps $1,000, before going full throttle on debt repayment. This small buffer prevents new debt from forming when emergencies arise.

Troubleshooting

“I Can’t Find Any Extra Time”

It often feels like there aren’t enough hours in the day, especially if you have a demanding job or family responsibilities. This is a common hurdle for many.

Conduct a “time audit” for a week. Track every hour to see where your time truly goes. You might find small pockets, like an hour after dinner or early mornings, that can be repurposed for a side hustle. Consider involving family members in chores to free up some of your time.

“My Debt Is So Big, It Feels Hopeless”

Looking at a large debt total can be incredibly discouraging, making the task seem insurmountable. This feeling can paralyze your efforts.

Break your debt down into smaller, manageable chunks. Focus on paying off just one small debt or reaching a specific payment milestone. Celebrate these small victories. The momentum from these successes will build, making the larger goal feel more achievable over time.

“I Keep Spending the Extra Money I Earn”

It’s tempting to reward yourself immediately when you earn extra cash, especially after hard work. However, this defeats the purpose of making money for debt repayment.

Automate your debt payments. As soon as your extra income hits your account, have it automatically transferred to your debt payment. This removes the temptation to spend it. Consider using a separate bank account for your side hustle income that is specifically linked to your debt payments.

Key Takeaways

- Understand Your Finances: Clearly list all debts and create a detailed budget to see where your money goes.

- Cut Spending First: Before earning more, identify and reduce unnecessary expenses for quick cash flow improvements.

- Diversify Income Streams: Explore various side hustles and gig economy opportunities that align with your skills and schedule.

- Sell Unused Items: Monetize possessions you no longer need to generate immediate funds for debt.

- Strategic Repayment: Choose a debt repayment strategy (snowball or avalanche) and stick to it for focused progress.

- Stay Consistent: Debt repayment is a journey; regular effort and celebrating small wins are vital for long-term success.

Frequently Asked Questions

How much extra money do I really need to make?

The amount depends on your debt load and how quickly you want to pay it off. Even an extra $50-$100 per week can make a significant difference over time, especially when applied consistently to high-interest debts. Every dollar you put towards debt beyond the minimum payment accelerates your progress.

Should I save for an emergency fund or pay off debt first?

Most financial experts recommend building a small starter emergency fund (e.g., $1,000) first. This protects you from unexpected expenses that could force you to take on new debt. Once you have that buffer, you can aggressively tackle your debt, knowing you have a safety net in place.

What if I don’t have any special skills for a side hustle?

You might be surprised! Many side hustles require general reliability and a willingness to learn, rather than highly specialized skills. Think about services like dog walking, house sitting, cleaning, or running errands. You can also develop new skills through free online courses to open up more opportunities.

How do I stay motivated when the debt seems overwhelming?

Break your debt into smaller, more manageable goals. Focus on paying off one small debt, or reaching a specific balance reduction. Celebrate these small victories. Regularly review your progress and remind yourself of the freedom and peace of mind that comes with being debt-free. Connect with supportive communities for encouragement.

Our Top Recommended Finds

- Budgeting App: An intuitive budgeting app helps you track spending, set goals, and see your progress visually.

- Side Hustle Idea Book: A guide filled with practical, low-barrier side hustle suggestions can spark inspiration and help you find the right fit.

- Noise-Cancelling Headphones: These can be a game-changer for focus, allowing you to concentrate on your side hustle work without distractions.

Your Path to Financial Freedom Starts Now

Taking control of your debt and building a healthier financial future isn’t just a dream; it’s an achievable reality.

The journey might require dedication and smart choices, but the rewards of financial peace are immeasurable.

Don’t wait for the “perfect” moment. Pick one step from this guide and take action today, even a small one. Your future self will thank you for it.