How To Save Money Fast On A Low Income

📚 The Financial Literacy Library

The best investment you can ever make is in your own financial education. These 5 cornerstone books are what millionaires, financial advisors, and wealth-builders universally recommend for completely rewiring how you think about earning, saving, and investing money.

🧠 The Psychology of Money

Doing well with money isn't necessarily about what you know—it's about how you behave. Morgan Housel masterfully breaks down the emotional and psychological biases that secretly dictate our financial decisions, offering a true paradigm shift in how to view wealth.

🏠 Rich Dad Poor Dad

The #1 personal finance book of all time for a reason. This foundational read shatters the myth that you need to earn a high income to be rich, teaching you the critical difference between working for money and making your money work for you via assets.

📈 Atomic Habits

While not strictly a finance book, building wealth is absolutely dependent on the daily habits you cultivate. James Clear provides the definitive framework for breaking bad spending habits and effortlessly automating the good ones that lead to long-term success.

📊 The Simple Path to Wealth

The ultimate antidote to complex, intimidating financial advice. JL Collins provides an incredibly accessible, low-stress roadmap to financial independence through index fund investing, perfectly explaining why simplicity beats Wall Street complexity every time.

💳 I Will Teach You to Be Rich

A tactical, no-BS, 6-week program that actually works. Ramit Sethi teaches you how to crush debt, automate your savings, and negotiate your salary—all while guilt-free spending on the things you truly love. A must-read for modern money management.

I remember a time when every dollar felt like it had already been spent before it even landed in my bank account. It felt impossible to get ahead, let alone save anything meaningful. This guide is built on real strategies that helped me and many others turn that feeling around.

You absolutely can save money, even when your income feels tight. This guide will show you exactly how to do it, step by practical step. It’s about smart choices, not deprivation.

Quick Overview

This guide will empower you to take control of your finances and build a savings habit, no matter your current income. You will learn actionable strategies to cut expenses, increase your financial literacy, and start building a secure future. Get ready to transform your money habits.

- Time needed: 1-2 hours to read and plan, ongoing effort for implementation.

- Difficulty: Beginner

- What you’ll need: Pen and paper, a bank account, an open mind, and a little determination.

Step-by-Step Instructions

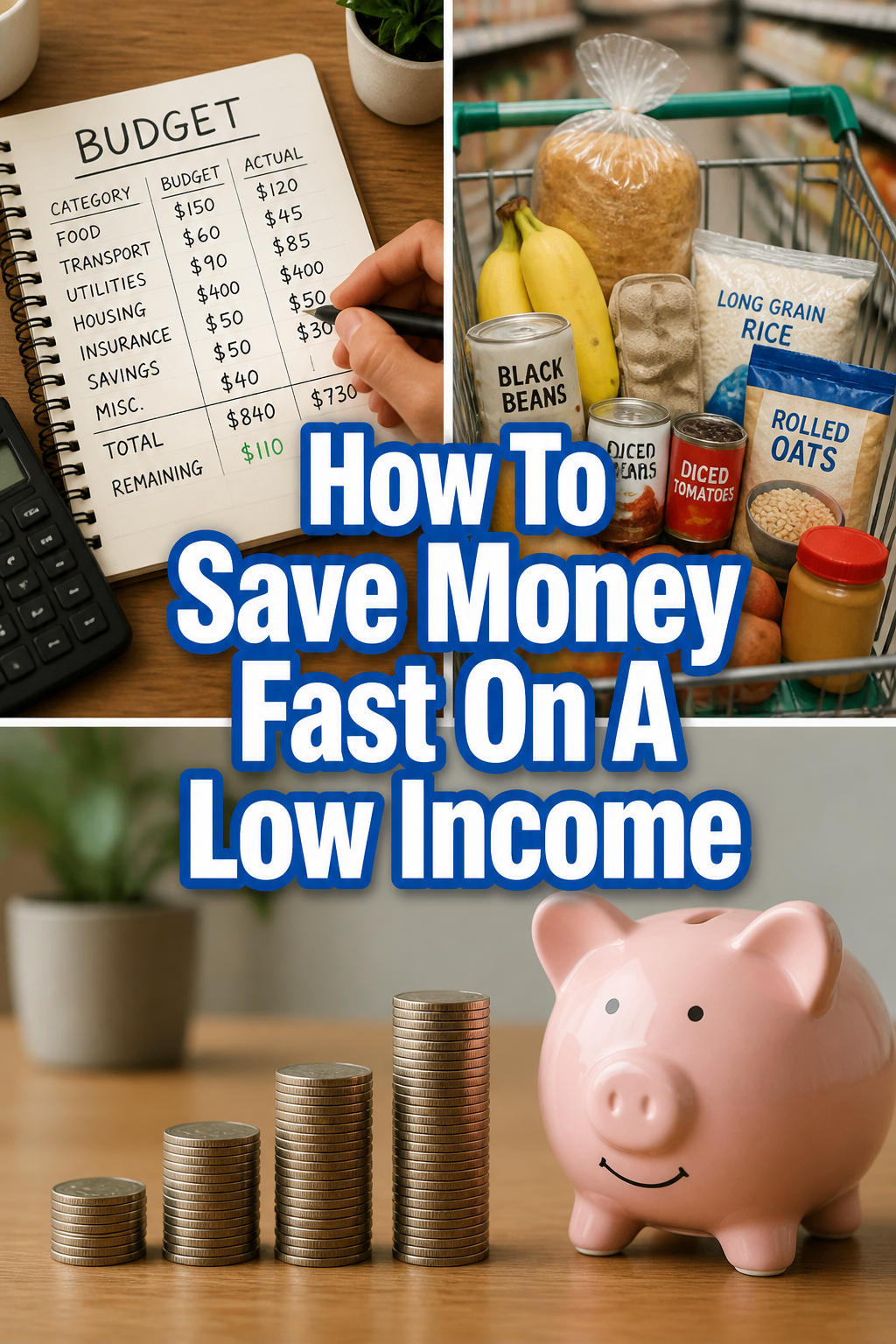

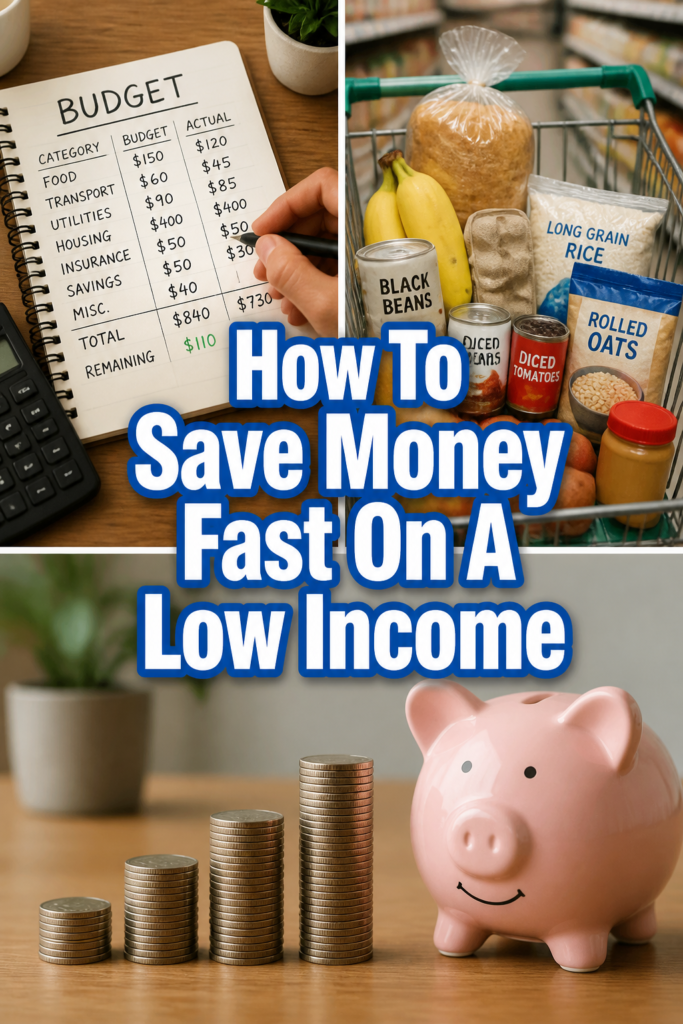

Step 1: Get Crystal Clear on Your Cash Flow

You can’t manage what you don’t measure. Start by understanding exactly where every penny of your income goes. This isn’t about judgment; it’s about information gathering.

Gather all your bank statements, credit card bills, and receipts from the last month or two. Categorize every single expense, from rent and utilities to groceries, transport, and even that impulse snack. This creates your financial snapshot.

Track every dollar. Write down your total take-home income. Then, list all your fixed expenses like rent, loan payments, and subscriptions. Finally, list your variable expenses like food, entertainment, and personal care.

Use a simple spreadsheet or notebook. Many free apps can help, but a basic pen-and-paper method works just as well. The goal is clarity, not complexity.

Pro Tip: Don’t skip this step. It’s the foundation for all effective saving. Many people are shocked to see where their money truly goes once they track it diligently. It’s an eye-opening experience.

Step 2: Create a Bare-Bones Budget (The “Zero-Based” Approach)

Now that you know your cash flow, it’s time to give every dollar a job. A zero-based budget means your income minus your expenses equals zero. This doesn’t mean you spend everything; it means you assign every dollar to a category, including savings.

Start by listing your income for the month. Then, subtract your essential expenses first: housing, food, transportation, and utilities. These are non-negotiables to keep you safe and fed.

Allocate funds for essentials. Ensure these critical areas are covered. Look for the absolute minimum you need to spend in each category.

Assign remaining money to savings and wants. Whatever is left goes to savings goals or discretionary spending. If you have nothing left for savings, you know you need to cut deeper into variable expenses.

Pro Tip: Be realistic but firm. If you only have $50 left after essentials, decide if that $50 is going entirely to savings or if a small portion can be for a treat. Every dollar has a purpose.

Step 3: Slash Variable Expenses Ruthlessly

This is where fast savings happen on a low income. Variable expenses are the easiest to control and offer the quickest wins. Think about areas like dining out, entertainment, and impulse purchases.

Review your tracked expenses from Step 1. Identify categories where you spend money without much thought. These are often the easiest places to cut back immediately.

Cook at home, always. Eating out is a budget killer. Meal prepping for the week can save hundreds. Pack your lunch, make your coffee at home, and plan your dinners.

Find free or low-cost entertainment. Instead of movies or concerts, try parks, libraries, free community events, or board game nights with friends. Get creative with your leisure time.

Eliminate impulse buys. Before buying anything non-essential, wait 24 hours. Often, the urge passes. Unsubscribe from marketing emails that tempt you to spend.

Pro Tip: Challenge yourself to a “no-spend” week or even a “no-spend” month on non-essentials. It’s a powerful way to reset spending habits and see how much you can truly save.

Step 4: Optimize Fixed Expenses (Even on a Low Income)

While harder to change quickly, fixed expenses can offer significant long-term savings. Think about rent, utilities, insurance, and subscriptions. These require a bit more effort but pay off big.

Look at your utility bills. Can you reduce your electricity or water usage? Turn off lights, take shorter showers, unplug unused electronics. Small changes add up.

Shop around for insurance. Car insurance, renter’s insurance – always compare quotes from different providers. Even a small saving each month adds up over a year.

Review subscriptions. Do you really use every streaming service, gym membership, or app subscription? Cancel anything you don’t use regularly or that doesn’t bring significant value.

Consider housing adjustments. While a big step, could you find a cheaper place, get a roommate, or negotiate your rent if you’re a good tenant? This is a larger shift but offers massive savings.

Pro Tip: Call your internet and phone providers. Ask if they have any cheaper plans or loyalty discounts. Often, they will offer a better deal to keep your business.

Step 5: Automate Your Savings

Make saving money effortless by setting it up to happen automatically. This removes the need for willpower each time you get paid. It ensures you “pay yourself first.”

Set up an automatic transfer from your checking account to a separate savings account every payday. Even a small amount, like $10 or $20, is a great start. The key is consistency.

Treat savings like a bill. Just as you pay your rent, pay your savings account. This psychological shift is incredibly powerful.

Start small, then increase. If $20 feels like too much, start with $5. Once you adjust, try to increase the amount slightly each month. Small, consistent increases build momentum.

Pro Tip: Open a separate savings account, ideally at a different bank, to make it harder to access and spend your savings impulsively. Out of sight, out of mind.

Step 6: Boost Your Income (Even Slightly)

Saving is half the equation; increasing income is the other. Even a small additional income stream can significantly accelerate your savings goals, especially on a low income.

Think about skills you have or tasks you could do for others. This isn’t about finding a new career, but about finding quick ways to earn a few extra dollars.

Sell unused items. Declutter your home and sell clothes, electronics, books, or furniture you no longer need. Use platforms like Facebook Marketplace or local consignment shops.

Take on small gigs. Offer to babysit, pet-sit, do yard work, or run errands for neighbors. Look for odd jobs that pay cash.

Explore online micro-tasks. Websites offer small payments for surveys, data entry, or transcription. While not a huge earner, it can contribute.

Pro Tip: Put 100% of any extra income directly into your savings. This money wasn’t part of your regular budget, so you won’t miss it. It’s pure bonus savings.

Step 7: Embrace the Power of “Found Money”

“Found money” is any unexpected cash you receive. This includes tax refunds, work bonuses, gifts, or even a $5 bill you find in an old coat pocket. The rule for found money is simple.

Every dollar of found money goes straight into your savings account. Resist the urge to spend it on something frivolous. This is your opportunity to boost your savings significantly.

Treat it as sacred. This money wasn’t expected, so it won’t impact your regular budget if it goes directly to savings. It’s a powerful accelerator.

Don’t budget for it. Never rely on found money to cover regular expenses. It’s extra, and it should always be treated as such for savings purposes.

Pro Tip: Even small amounts count. If you get a $20 birthday gift, save it. If you get a $50 tax refund, save it. Consistency with found money adds up quickly.

Step 8: Set Clear, Motivating Savings Goals

Saving without a purpose can feel draining. Having clear, exciting goals provides the motivation to stick with your plan, especially when times get tough. What are you saving for?

Your goals could be an emergency fund, a down payment for something important, or even a small treat you’ve wanted for a long time. Make them specific and measurable.

Define your “why.” Do you want a three-month emergency fund? To replace an old appliance? To take a small, well-deserved trip? Write it down.

Break down large goals. If you need $1,000, figure out how much you need to save each week or month. This makes it feel achievable.

Track your progress visually. Use a thermometer chart, an app, or a simple tally in your notebook. Seeing your progress fuels your motivation.

Pro Tip: Celebrate small milestones. Saved your first $100? Acknowledge it! This positive reinforcement helps keep you engaged and motivated for the long haul.

Common Mistakes to Avoid

Trying to Do Too Much, Too Soon

Many people get excited and try to cut every expense and save a huge amount all at once. This often leads to burnout and giving up entirely. Saving is a marathon, not a sprint.

Instead, start with one or two manageable changes. Once those become habits, add another. Gradual changes are more sustainable and lead to lasting success.

Ignoring Small Expenses

It’s easy to focus on big bills and overlook the daily small purchases like coffee, snacks, or impulse buys. These “small leaks” in your budget can drain hundreds of dollars each month without you realizing it.

Track every single expense, no matter how small. You might be surprised to see how much those little purchases add up. Cutting back on these can yield significant savings quickly.

Not Having a Clear “Why”

Saving money just for the sake of it can feel restrictive and joyless. Without a compelling reason or goal, it’s easy to lose motivation and revert to old spending habits.

Define what you are saving for. An emergency fund, a down payment, a special experience – articulate your goals clearly. This “why” will be your driving force when willpower wanes.

Comparing Yourself to Others

It’s easy to look at friends or social media and feel like you’re not doing enough or that your low income makes saving impossible. Everyone’s financial journey is unique.

Focus on your own progress and celebrate your own wins. Your situation is different, and your success will be defined by your own consistent efforts and adherence to your plan.

Troubleshooting

“I feel deprived and miserable.”

This is a common feeling when starting to save aggressively. It means you might be cutting too much too quickly or not allowing for any small treats.

Revisit your budget and allocate a small amount for discretionary spending. It’s okay to have a little “fun money” to avoid burnout. The goal is sustainable saving, not misery.

“I keep dipping into my savings.”

This usually happens because your savings account is too accessible or your goals aren’t strong enough. It indicates a lack of mental separation between your savings and checking.

Open a separate savings account at a different bank if possible. Make transfers take a day or two. Reinforce your “why” for saving, and remind yourself of your goals before making a withdrawal.

“My income is so low, there’s nothing left to save.”

This feeling is frustrating, but often there are still small changes possible. It requires a very deep look into every expense and potentially seeking income boosts.

Go back to Step 1 and 2. Scrutinize every single variable expense. Can you cut even $5 from groceries? Can you sell one item? Can you earn an extra $10? Every small amount counts and builds momentum.

Key Takeaways

- Knowledge is power: Understand exactly where your money goes before making changes.

- Budget with purpose: Give every dollar a job, including saving.

- Prioritize ruthlessly: Slash variable expenses first for quick impact.

- Automate your progress: Set up regular, automatic transfers to savings.

- Boost income creatively: Even small extra earnings significantly accelerate savings.

- Stay motivated: Set clear goals and celebrate every milestone along the way.

Frequently Asked Questions

Is it really possible to save on a very low income?

Yes, it absolutely is. It requires discipline and smart strategies, but even small amounts saved consistently add up. The key is to optimize every dollar and prioritize savings. It’s about making deliberate choices with your limited resources.

How much should I aim to save each month?

The ideal amount varies for everyone, but start with whatever you comfortably can, even if it’s just $5 or $10. Once that becomes a habit, try to increase it. The most important thing is consistency, not the initial amount.

What’s the best type of savings account?

For fast savings on a low income, a high-yield savings account is ideal if you can find one without minimum balance requirements or fees. Otherwise, any separate savings account that is slightly inconvenient to access will work. The goal is to separate the money.

How long will it take to see results?

You can start seeing results almost immediately by implementing expense cuts. Building a significant savings cushion takes time and consistency, but you’ll feel more in control and less stressed about money very quickly. Celebrate every small gain.

Our Top Recommended Finds

- A simple budgeting notebook: Perfect for tracking expenses and income without needing apps or complex software.

- Reusable water bottle and coffee cup: Cut down on daily impulse buys for drinks, saving you money every single day.

- Meal prep containers: Makes cooking at home and packing lunches easy and efficient, preventing costly takeout.

Embrace Your Financial Power Today

You have the power to change your financial situation, no matter your income level. This guide provides the practical steps you need to start saving money fast and build a more secure future. It won’t always be easy, but every smart choice you make brings you closer to your goals.

Start with one step today. Track your spending, set up a small automatic transfer, or challenge yourself to a no-spend day. Small actions create big results over time. Your financial freedom begins right now, with these deliberate choices.