💵 2 Dollar Bill Value

📚 The Financial Literacy Library

The best investment you can ever make is in your own financial education. These 5 cornerstone books are what millionaires, financial advisors, and wealth-builders universally recommend for completely rewiring how you think about earning, saving, and investing money.

🧠 The Psychology of Money

Doing well with money isn't necessarily about what you know—it's about how you behave. Morgan Housel masterfully breaks down the emotional and psychological biases that secretly dictate our financial decisions, offering a true paradigm shift in how to view wealth.

🏠 Rich Dad Poor Dad

The #1 personal finance book of all time for a reason. This foundational read shatters the myth that you need to earn a high income to be rich, teaching you the critical difference between working for money and making your money work for you via assets.

📈 Atomic Habits

While not strictly a finance book, building wealth is absolutely dependent on the daily habits you cultivate. James Clear provides the definitive framework for breaking bad spending habits and effortlessly automating the good ones that lead to long-term success.

📊 The Simple Path to Wealth

The ultimate antidote to complex, intimidating financial advice. JL Collins provides an incredibly accessible, low-stress roadmap to financial independence through index fund investing, perfectly explaining why simplicity beats Wall Street complexity every time.

💳 I Will Teach You to Be Rich

A tactical, no-BS, 6-week program that actually works. Ramit Sethi teaches you how to crush debt, automate your savings, and negotiate your salary—all while guilt-free spending on the things you truly love. A must-read for modern money management.

Have you ever received a two-dollar bill as change and felt like you’d just found a four-leaf clover? There is a certain mystique surrounding the $2 bill. Some people tuck them away in their wallets for good luck, while others believe they are rare relics from a bygone era that must be worth a fortune. But beyond the curiosity of the physical currency, the concept of the 2 Dollar Bill Value serves as a powerful metaphor for modern wealth-building: it’s about finding hidden value in the unexpected and understanding that small, consistent actions lead to massive financial freedom.

In a world of digital payments and high-speed trading, the humble two-dollar bill reminds us to slow down and look at the “small change” in our lives. Whether you are a collector looking for a rare “Star Note” or a savvy saver looking to optimize your budget, understanding the true value of your money—regardless of the denomination—is the first step toward a “money-smart” lifestyle. Let’s explore the history, the collector’s market, and the wealth-building mindset that this unique piece of American currency inspires.

What is 2 Dollar Bill Value?

When we talk about 2 Dollar Bill Value, we are looking at two distinct things: the numismatic (collector) value and the functional financial value. Most two-dollar bills in circulation today are worth exactly two dollars. You can take them to the grocery store, use them at a vending machine, or deposit them at your bank. However, because they represent less than 1% of all currency in circulation, they feel “rare,” which creates a psychological value that far exceeds their face value.

From a numismatic perspective, certain $2 bills can be worth hundreds or even thousands of dollars. Factors such as the year of series, the color of the seal (red, brown, or blue), and the serial number play a massive role. For example, an uncirculated 1890 Treasury Note can fetch over $4,000 at auction. But for the average person, the “value” of the $2 bill is often found in its ability to jumpstart a savings habit. Because people are hesitant to spend them, they become an accidental “savings account” in your pocket.

Think of it as the “unconventional asset.” Just as a smart investor looks for undervalued stocks that others are overlooking, a person with a wealth-building mindset looks for small ways to save and invest that others might ignore. The $2 bill is the perfect symbol for this strategy: it’s common enough to find if you look, but unique enough to make you think twice before spending it.

Key Features

To truly understand the 2 Dollar Bill Value, you need to know what makes these bills special. Whether you’re looking at your bank account or a physical bill, detail-oriented observation is a key trait of the financially successful. Here are the primary features that define the value of a $2 bill:

- The Portrait of Thomas Jefferson: Since 1928, the third U.S. President has graced the front of the bill. Jefferson was a man of many talents and a proponent of individual liberty—a fitting face for a bill that encourages independent financial thinking.

- The Declaration of Independence Back: The reverse side features a beautiful engraving of the signing of the Declaration of Independence. This replaced the “Monticello” design in 1976 for the Bicentennial. This design makes the bill a piece of portable art.

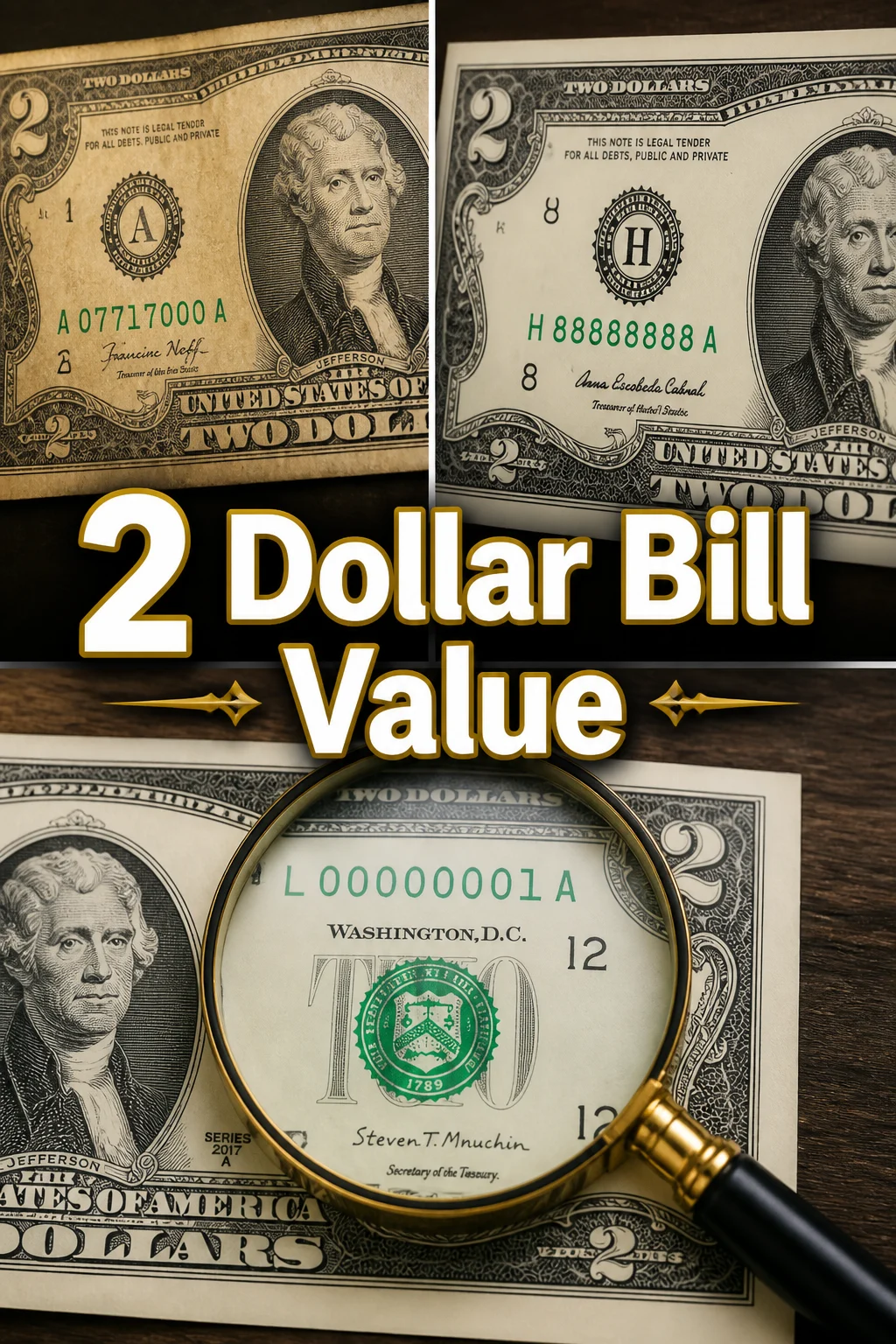

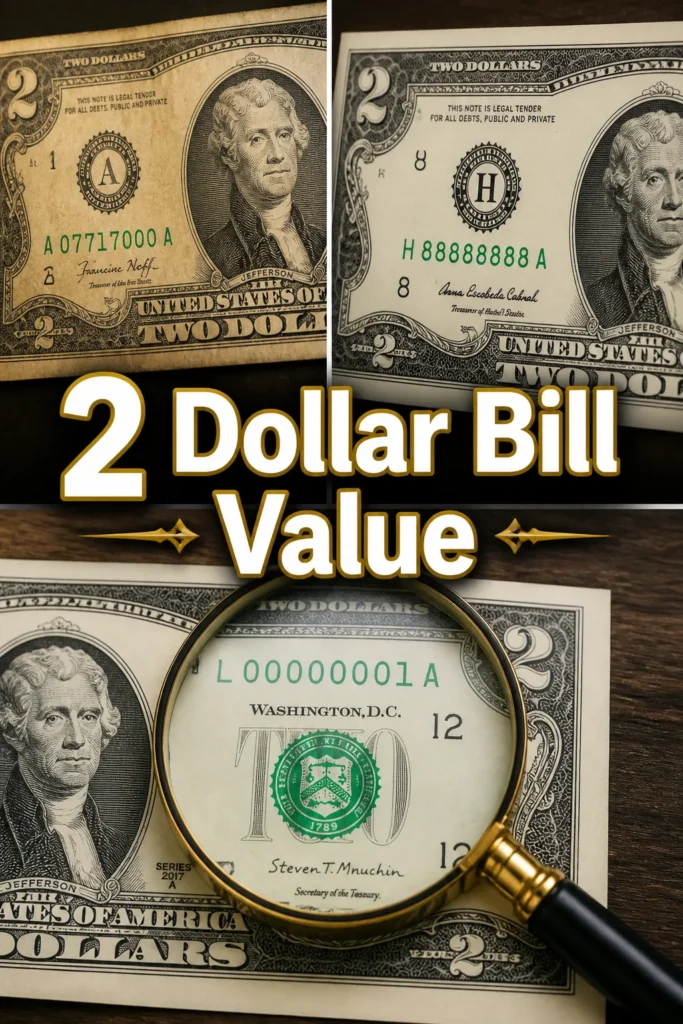

- Seal Colors: This is a major value driver. Modern bills have a green seal. Older versions might have a red seal (United States Notes) or a blue seal (Silver Certificates). Red seals from the 1928, 1953, and 1963 series are highly sought after by collectors.

- The “Star Note” Symbol: If you see a small star at the end of the serial number, you’ve found a replacement note. These are printed to replace bills that were damaged during the printing process. Because they are rarer, they almost always carry a premium value.

- Serial Number Patterns: Collectors love “fancy” serial numbers. This includes “ladders” (12345678), “solids” (88888888), or “radars” (numbers that read the same forward and backward). A bill with a unique serial number can turn a $2 investment into a $500 windfall.

How to Get Started

Applying the lessons of the 2 Dollar Bill Value to your personal finances doesn’t require a degree in economics. It requires a willingness to start small and stay consistent. Here is how you can get started with a “2 Dollar Mindset” to build your wealth:

- Visit Your Local Bank: Most people think $2 bills aren’t made anymore. In reality, the Federal Reserve still orders them. Simply go to your bank and ask the teller if they have any $2 bills. This is a great way to start a “fun” savings fund. By converting your $20 bills into $2 bills, you create a psychological barrier to spending, as we tend to view these bills as “special.”

- Launch the “Jefferson Challenge”: Every time you receive a $2 bill (or any specific small denomination), commit to never spending it. Put it in a jar or a separate savings account. Over a year, you’ll be shocked at how these “small” amounts add up. This is the foundation of micro-saving.

- Audit Your “Digital Change”: Use the same logic for your bank account. Many apps allow you to “round up” your purchases to the nearest dollar and invest the difference. If you spend $4.50 on a coffee, $0.50 goes into an investment account. This is the modern version of saving $2 bills.

- Educate Yourself on Scarcity: Learn to identify what is actually rare versus what is just perceived as rare. In the world of investing, this means distinguishing between a “hype” stock and a truly valuable company. In the world of currency, it means knowing that a 1976 $2 bill is common, but a 1928 red seal is a treasure.

Tips for Success

Building wealth is a marathon, not a sprint. To maximize your financial potential and understand the 2 Dollar Bill Value in your own life, follow these pro tips:

1. Focus on the “Condition” of Your Finances

In the world of currency collecting, “condition is everything.” A crisp, uncirculated bill is worth significantly more than a torn, wrinkled one. Apply this to your credit score and your debt-to-income ratio. Keep your financial records “crisp” by paying bills on time and keeping your debt low. A “clean” financial profile is your most valuable asset when you want to buy a home or start a business.

2. Look for the “Star Notes” in Life

Just as a Star Note is a rare find in a stack of cash, look for “Star Note” opportunities in your career and investments. These are the side hustles, the high-yield savings accounts, or the skills you can learn that set you apart from the crowd. Don’t just settle for the “standard issue” life; look for the unique opportunities that add extra value to your time.

3. Use the Power of Compound Interest

If you saved just two dollars a day starting at age 20 and invested it in a standard index fund with an 8% return, you would have nearly $250,000 by the time you retire. The 2 Dollar Bill Value isn’t just about the paper; it’s about the time-value of money. Never underestimate the power of a small amount of money given a long period of time to grow.

4. Practice “Mindful Spending”

Before you spend any money, ask yourself: “Is this purchase worth the hours of my life I spent earning it?” When you treat every dollar (or two-dollar bill) as a seed for a future money tree, you become much more intentional about where your money goes. This is the hallmark of a wealth-building mindset.

Common Mistakes to Avoid

Even the most well-intentioned savers can fall into traps. When exploring the 2 Dollar Bill Value, be sure to avoid these common pitfalls:

- Overpaying for “Rare” Bills: You might see $2 bills listed on auction sites for hundreds of dollars. Often, these are common bills that unscrupulous sellers are trying to offload on unsuspecting buyers. Always check a reputable price guide before “investing” in physical currency.

- The “Hoarding” Trap: While saving is great, holding too much physical cash can actually lose you money due to inflation. If you have a mountain of $2 bills under your mattress, they are losing purchasing power every day. Once your “fun fund” reaches a certain size, move it into a high-yield savings account or an investment portfolio where it can work for you.

- Ignoring Small Expenses: Many people think, “It’s only $2, it doesn’t matter.” But those small leaks can sink a big ship. Subscription services you don’t use, daily gourmet coffees, and impulse buys are the “reverse” of the $2 bill challenge—they quietly drain your wealth.

- Emotional Investing: Don’t buy something (a bill, a stock, or a collectible) just because it has a “cool” story. Base your financial decisions on data, historical performance, and your long-term goals.

FAQ

Are $2 bills still being printed?

Yes! The Bureau of Engraving and Printing still produces them. They are not discontinued; they are simply printed in lower quantities than $1 or $20 bills because they don’t circulate as frequently.

How much is a 1976 $2 bill worth?

Most 1976 $2 bills are only worth their face value ($2). Because millions were printed for the Bicentennial and many people saved them thinking they would be rare, the supply remains very high. However, if it has a unique serial number or a “Star,” it could be worth more.

Is it true that $2 bills are unlucky?

This is an old superstition with no basis in reality. In fact, many people today consider them “lucky” because they are so unique. In terms of your finances, you create your own luck through preparation and smart decision-making!

Can I use $2 bills at any store?

Absolutely. They are legal tender for all debts, public and private. While some younger cashiers might be confused because they don’t see them often, they are perfectly valid currency.

💼 The Money Management Toolkit

Knowledge is power, but proper execution requires the right tools. Getting your financial life organized doesn't have to be overwhelming. These 5 physical management tools are exactly what successful households use to budget, track cash, and secure their most important assets.

📝 Clever Fox Budget Planner & Bill Organizer

The ultimate analog command center for your finances. Sometimes keeping your budget in an app just doesn't stick. Physically writing down your goals, tracking expenses, and planning for debt payoff creates a level of accountability that digital spreadsheets simply can't match.

💵 A6 Leather Cash Stuffing Binder

The viral tool that made the cash-envelope budgeting system popular again. By allocating actual physical cash to designated envelopes (groceries, dining out, fun money), you physically cap your spending, making it virtually impossible to overdraft or overspend.

🔥 Fireproof & Waterproof Document Safe

A critical piece of financial security that many families overlook. Protecting your passports, birth certificates, property deeds, and estate planning documents from disaster is just as important as protecting the money in your bank account.

🏷️ Brother P-Touch Digital Label Maker

The unsung hero of a functional home office. When tax season rolls around or you need to find an important receipt, having perfectly labeled and categorized filing cabinets or accordion folders saves hours of frustrating searches and potential late fees.

🔒 SentrySafe Compact Fireproof Lock Box

For the physical assets that need extra heavy-duty protection—think emergency cash reserves, hard drives with Bitcoin cold wallets, or physical precious metals. This compact, locking safe provides peace of mind that your physical wealth is secure at home.

Conclusion

The 2 Dollar Bill Value is about more than just a piece of green paper with Thomas Jefferson’s face on it. It is a reminder that value is often found in the places we least expect. It teaches us that being “different” in our financial habits—saving when others spend, and looking for opportunities when others are distracted—is the key to building lasting wealth.

Whether you decide to start collecting rare notes or simply use the $2 bill as a catalyst to start your first savings account, the lesson remains the same: every dollar counts. Wealth isn’t built overnight; it’s built $2 at a time, through discipline, education, and a bit of curiosity. So, the next time you see a two-dollar bill, don’t just see it as pocket change. See it as a symbol of your financial potential and a reminder that you have the power to turn small beginnings into a legendary financial future. Start your wealth-building journey today—your “future self” will thank you for every $2 you saved!