💰 50 30 20 Budget

📚 The Financial Literacy Library

The best investment you can ever make is in your own financial education. These 5 cornerstone books are what millionaires, financial advisors, and wealth-builders universally recommend for completely rewiring how you think about earning, saving, and investing money.

🧠 The Psychology of Money

Doing well with money isn't necessarily about what you know—it's about how you behave. Morgan Housel masterfully breaks down the emotional and psychological biases that secretly dictate our financial decisions, offering a true paradigm shift in how to view wealth.

🏠 Rich Dad Poor Dad

The #1 personal finance book of all time for a reason. This foundational read shatters the myth that you need to earn a high income to be rich, teaching you the critical difference between working for money and making your money work for you via assets.

📈 Atomic Habits

While not strictly a finance book, building wealth is absolutely dependent on the daily habits you cultivate. James Clear provides the definitive framework for breaking bad spending habits and effortlessly automating the good ones that lead to long-term success.

📊 The Simple Path to Wealth

The ultimate antidote to complex, intimidating financial advice. JL Collins provides an incredibly accessible, low-stress roadmap to financial independence through index fund investing, perfectly explaining why simplicity beats Wall Street complexity every time.

💳 I Will Teach You to Be Rich

A tactical, no-BS, 6-week program that actually works. Ramit Sethi teaches you how to crush debt, automate your savings, and negotiate your salary—all while guilt-free spending on the things you truly love. A must-read for modern money management.

Hey there, money-savvy friend! Are you tired of feeling like your finances are a tangled mess, leaving you stressed and unsure where your hard-earned cash actually goes? Do you dream of a simpler way to manage your money, one that doesn’t involve complicated spreadsheets or hours of number crunching? If so, you’re in for a treat!

Welcome to the world of the 50 30 20 Budget – a refreshingly straightforward and incredibly powerful budgeting method that has helped countless individuals gain control, clarity, and confidence over their financial lives. Forget rigid rules and overwhelming details; this approach is all about striking a healthy balance between your current needs, your desires, and your future financial security. It’s popular because it’s intuitive, flexible, and focuses on the big picture, making complex financial concepts feel surprisingly manageable. Ready to transform your money habits and build a brighter financial future? Let’s dive in!

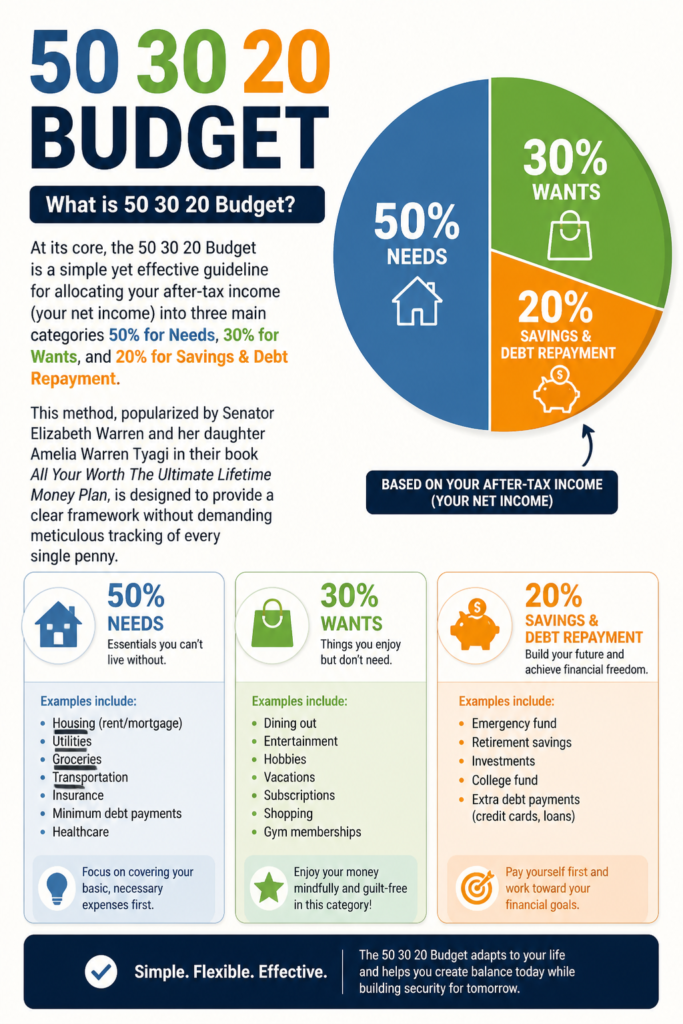

What is 50 30 20 Budget?

At its core, the 50 30 20 Budget is a simple yet effective guideline for allocating your after-tax income (your net income) into three main categories: 50% for Needs, 30% for Wants, and 20% for Savings & Debt Repayment. This method, popularized by Senator Elizabeth Warren and her daughter Amelia Warren Tyagi in their book “All Your Worth: The Ultimate Lifetime Money Plan,” is designed to provide a clear framework without demanding meticulous tracking of every single penny.

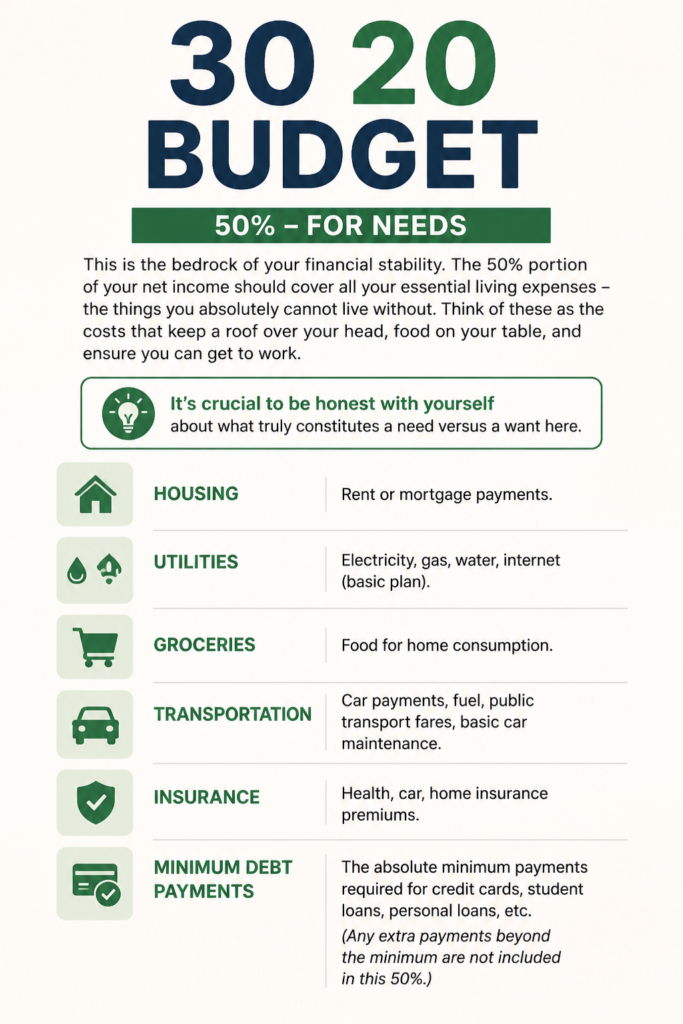

50% for Needs

This is the bedrock of your financial stability. The 50% portion of your net income should cover all your essential living expenses – the things you absolutely cannot live without. Think of these as the costs that keep a roof over your head, food on your table, and ensure you can get to work. It’s crucial to be honest with yourself about what truly constitutes a need versus a want here.

- Housing: Rent or mortgage payments.

- Utilities: Electricity, gas, water, internet (basic plan).

- Groceries: Food for home consumption.

- Transportation: Car payments, fuel, public transport fares, basic car maintenance.

- Insurance: Health, car, home insurance premiums.

- Minimum Debt Payments: The absolute minimum payments required for credit cards, student loans, personal loans, etc. (Any extra payments beyond the minimum go into the 20% category).

- Basic Communication: A functional phone plan.

If your needs exceed 50% of your income, it’s a strong signal to re-evaluate where you can cut back, perhaps by finding a more affordable living situation, reducing transportation costs, or exploring ways to increase your income.

30% for Wants

Ah, the fun stuff! This 30% category is for all the discretionary spending that enhances your life but isn’t strictly essential. Wants are things you could technically live without, even if they bring you immense joy or convenience. This category provides flexibility and allows you to enjoy life without guilt, as long as you stay within your allocated percentage.

- Dining Out: Restaurant meals, takeout, coffee shop visits.

- Entertainment: Movies, concerts, sporting events, streaming services (Netflix, Spotify, etc.).

- Hobbies & Recreation: Gym memberships, yoga classes, craft supplies, gaming.

- Shopping: New clothes, gadgets, home decor (beyond essentials).

- Travel & Vacations: Flights, hotels, excursions.

- Premium Services: High-tier internet plans, expensive phone upgrades.

- Gifts: Presents for friends and family.

This is often the most flexible category, and where many people find room to adjust their budget when needed. If you’re struggling to meet your 20% savings goal, this is the first place to look for potential cuts.

20% for Savings & Debt Repayment

This 20% is your future-building fund and arguably the most critical component for long-term financial health. It’s dedicated to securing your financial future and accelerating your journey to freedom.

- Emergency Fund: Building a cash reserve to cover unexpected expenses (e.g., job loss, medical emergency, car repair). Aim for 3-6 months of living expenses.

- Retirement Savings: Contributions to a 401(k), IRA, Roth IRA, or other retirement accounts.

- Investments: Money put into brokerage accounts, mutual funds, stocks, etc., for wealth growth.

- Extra Debt Payments: Any payments above the minimum required for credit cards, student loans, car loans, or other debts. This accelerates debt payoff and saves you interest.

- Future Goals: Saving for a down payment on a house, a child’s education, a new car, or any other significant future purchase.

Prioritizing this 20% ensures you’re not just living for today but actively building a robust financial foundation for tomorrow. It’s the engine that drives your financial independence.

Key Features

The 50 30 20 Budget isn’t just another budgeting method; it’s a philosophy that empowers you with clarity and control. Here are some of its standout features:

- Simplicity and Flexibility: Unlike highly detailed budgets that track every single expenditure, the 50 30 20 method focuses on broad categories. This makes it incredibly easy to understand, implement, and stick with. It offers flexibility within each category, allowing you to tailor your spending to your personal preferences without feeling overly restricted.

- Promotes Financial Balance: This budget encourages a healthy balance between living in the present and planning for the future. It ensures you’re covering your essentials, enjoying your life, and consistently saving and paying down debt – all at the same time. This holistic approach prevents common pitfalls like overspending on wants or neglecting future security.

- Action-Oriented and Goal-Driven: By clearly defining percentages for savings and debt repayment, the 50 30 20 budget inherently pushes you towards your financial goals. It’s not just about tracking; it’s about actively allocating funds to achieve your aspirations, whether that’s an emergency fund, early retirement, or becoming debt-free.

- Reduces Financial Stress: When you know exactly where your money is going and that you’re hitting your savings targets, a huge weight is lifted. The clarity provided by this budget can significantly reduce financial anxiety and empower you to make smarter spending decisions with confidence.

- Adaptable to All Income Levels: Because it’s based on percentages of your income, the 50 30 20 Budget is highly adaptable. Whether you earn a little or a lot, the framework remains relevant. The specific dollar amounts will change, but the healthy financial proportions stay the same, making it a universal tool for financial well-being.

How to Get Started

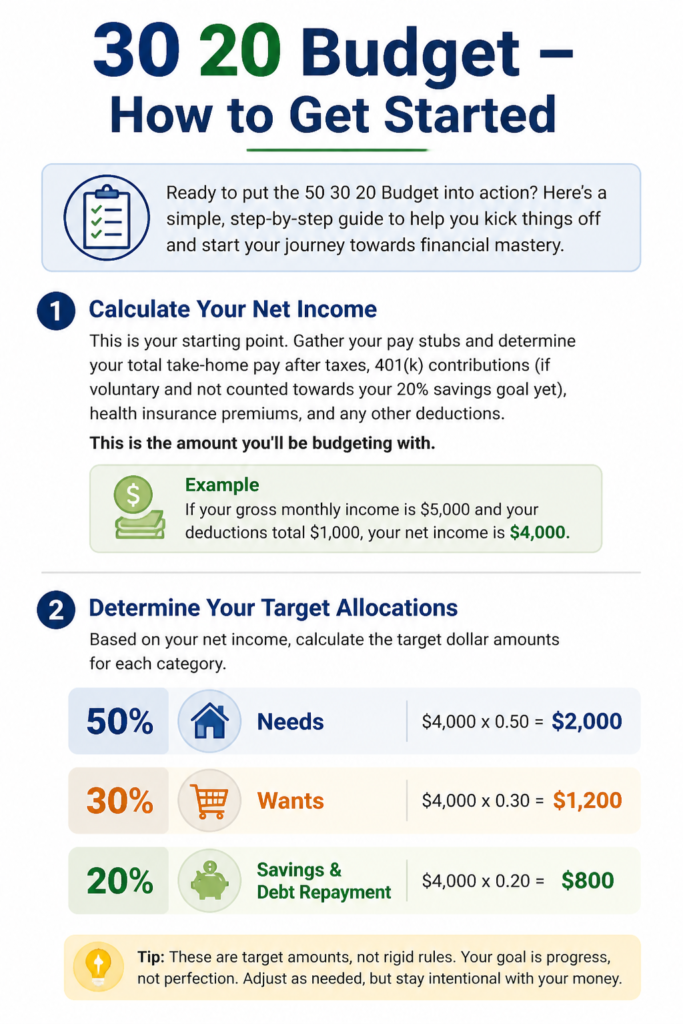

Ready to put the 50 30 20 Budget into action? Here’s a simple, step-by-step guide to help you kick things off and start your journey towards financial mastery:

- Calculate Your Net Income: This is your starting point. Gather your pay stubs and determine your total take-home pay after taxes, 401(k) contributions (if voluntary and not counted towards your 20% savings goal yet), health insurance premiums, and any other deductions. This is the amount you’ll be budgeting with.

- Example: If your gross monthly income is $5,000 and your deductions total $1,000, your net income is $4,000.

- Determine Your Target Allocations: Based on your net income, calculate the target dollar amounts for each category:

- 50% Needs: $4,000 x 0.50 = $2,000

- 30% Wants: $4,000 x 0.30 = $1,200

- 20% Savings & Debt Repayment: $4,000 x 0.20 = $800

These are your monthly spending limits for each category.

- Track Your Current Spending (Initially): For one to three months, diligently track every dollar you spend. This step is crucial for understanding your current habits. You can use budgeting apps (like Mint, YNAB, Personal Capital), a simple spreadsheet, or even a notebook. Categorize each expense as a Need, Want, or Savings/Debt Repayment. Don’t try to change anything yet; just observe.

- Compare and Adjust: Once you have a clear picture of your actual spending, compare it to your target allocations.

- Are your Needs exceeding 50%? Look for areas to cut back, like negotiating bills, finding cheaper insurance, or reducing grocery waste.

- Are your Wants gobbling up too much? This is usually the easiest place to make immediate changes. Can you cook more at home, reduce subscriptions, or find free entertainment?

- Are you hitting your 20% for Savings & Debt? If not, identify where you can pull money from the Needs or Wants categories to meet this vital goal.

This is where the real work happens – making conscious choices to align your spending with your budget.

- Automate Your Savings & Debt Payments: This is a game-changer. Set up automatic transfers from your checking account to your savings, investment, and debt repayment accounts immediately after you get paid. If you pay yourself first, you won’t even miss the money, and your future self will thank you.

- Review and Refine Regularly: Your life and financial situation will change. Make it a habit to review your budget at least monthly, or quarterly. Are your needs still the same? Have your income or goals changed? Be prepared to adjust your allocations as needed. This isn’t a one-and-done task; it’s an ongoing process.

Tips for Success

Embarking on a new budgeting journey can feel daunting, but with these pro tips, you’ll be well on your way to mastering the 50 30 20 Budget and achieving your financial goals:

- Be Brutally Honest with “Needs” vs. “Wants”: This is perhaps the most critical tip. It’s easy to rationalize a “want” as a “need.” That daily gourmet coffee? A want. The latest smartphone? Often a want, not a need. A basic internet connection for work is a need, but the premium fastest-speed package might be a want. Challenge every expense and ask yourself: “Could I genuinely live without this, or find a cheaper alternative, without compromising my basic survival or ability to earn income?” Honesty here sets the foundation for your entire budget.

- Automate Everything You Can: “Set it and forget it” is your mantra for savings and debt repayment. Schedule automatic transfers to your savings accounts, investment accounts, and extra debt payments for the day after your paycheck hits. This ensures your future self is paid first, making it less likely you’ll accidentally spend that money on wants. You can also automate bill payments for your needs category.

- Find Creative Ways to Trim Your Wants: Instead of cutting out all fun, get creative! Meal prepping can drastically reduce dining-out expenses. Explore free entertainment options like parks, libraries, or free community events. Look for subscription services you no longer use and cancel them. Every small cut in your “wants” category frees up money for your “savings” or can even slightly reduce pressure on your “needs.”

- Embrace the “Why” Behind Your Budget: Don’t just budget because someone told you to. Connect your budget to your deepest financial goals. Do you want to buy a house? Travel the world? Retire early? Become debt-free? When you have a strong “why,” sticking to your allocations becomes less about deprivation and more about purposeful progress towards a dream. Keep your “why” visible and let it motivate you through challenging moments.

- Celebrate Small Wins and Be Kind to Yourself: Budgeting is a journey, not a sprint. You’ll have good months and not-so-good months. Don’t beat yourself up over occasional slip-ups. Learn from them, adjust, and move forward. Celebrate every milestone – paying off a small debt, hitting a savings goal, or simply sticking to your budget for a month. Positive reinforcement keeps you motivated and makes the process enjoyable.

Common Mistakes to Avoid

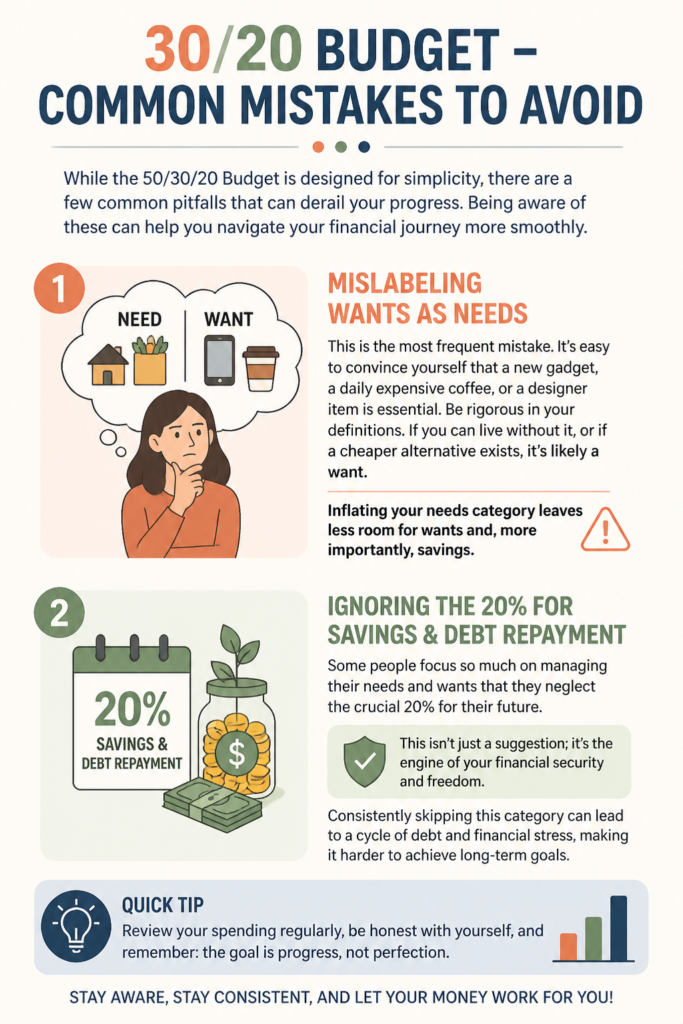

While the 50 30 20 Budget is designed for simplicity, there are a few common pitfalls that can derail your progress. Being aware of these can help you navigate your financial journey more smoothly:

- Mislabeling Wants as Needs: This is the most frequent mistake. It’s easy to convince yourself that a new gadget, a daily expensive coffee, or a designer item is essential. Be rigorous in your definitions. If you can live without it, or if a cheaper alternative exists, it’s likely a want. Inflating your “needs” category leaves less room for “wants” and, more importantly, “savings.”

- Ignoring the 20% for Savings & Debt Repayment: Some people focus so much on managing their needs and wants that they neglect the crucial 20% for their future. This isn’t just a suggestion; it’s the engine of your financial freedom. Without consistent savings and aggressive debt repayment, you’ll struggle to build wealth and achieve long-term security. Make this 20% non-negotiable.

- Not Tracking Spending (at Least Initially): While the 50 30 20 Budget isn’t about micro-managing every penny forever, skipping the initial tracking phase is a big mistake. You can’t adjust what you don’t measure. For the first few months, diligently track where your money is actually going. This insight is invaluable for identifying problem areas and making informed adjustments.

- Being Too Rigid or Getting Discouraged by Setbacks: Life happens! There will be unexpected expenses, temptations, and months where you might go over budget in one category. Don’t throw in the towel. The 50 30 20 Budget is a guideline, not a prison sentence. Learn from your mistakes, make adjustments, and get back on track. Flexibility and resilience are key to long-term success.

- Comparing Your Budget to Others: Your financial journey is unique to you. What works for your friend, colleague, or family member might not work for you, and vice-versa. Avoid the trap of comparing your spending habits or financial progress to others. Focus on your own goals, your own income, and your own progress. Your definition of a “want” or a “need” might differ, and that’s perfectly fine.

FAQ

Q1: What if my needs exceed 50% of my income?

A: This is a common challenge, especially in high-cost-of-living areas or with lower incomes. If your needs consistently exceed 50%, you have a few options: 1) Reduce “Needs”: Can you downsize your living situation, get a roommate, cut transportation costs, or find cheaper insurance? 2) Aggressively Cut “Wants”: Temporarily reduce your wants to free up more money for needs and savings. 3) Increase Income: Explore side hustles, ask for a raise, or seek a higher-paying job. It might take time, but adjusting these factors is crucial for long-term financial health.

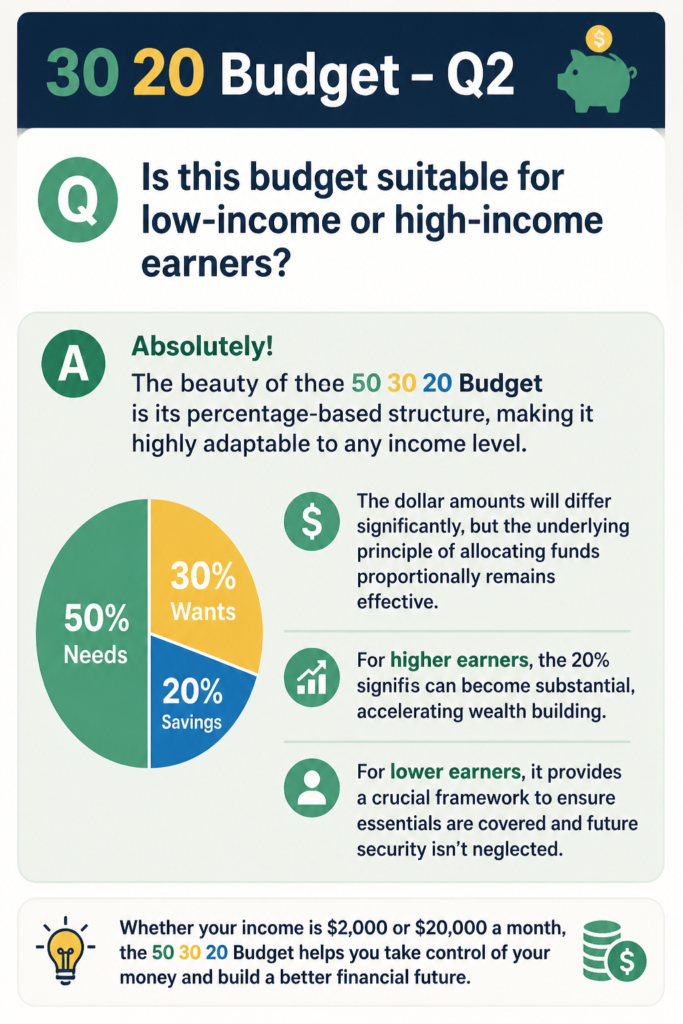

Q2: Is this budget suitable for low-income or high-income earners?

A: Absolutely! The beauty of the 50 30 20 Budget is its percentage-based structure, making it highly adaptable to any income level. The dollar amounts will differ significantly, but the underlying principle of allocating funds proportionally remains effective. For higher earners, the 20% savings can become substantial, accelerating wealth building. For lower earners, it provides a crucial framework to ensure essentials are covered and future security isn’t neglected.

Q3: How often should I review and adjust my budget?

A: It’s a good idea to review your budget at least once a month, especially when you’re first starting out. This allows you to catch any deviations early and make necessary adjustments. A more thorough review, perhaps quarterly or semi-annually, is also beneficial to account for bigger life changes like a new job, a move, or shifting financial goals. Your budget should be a living document that evolves with your life.

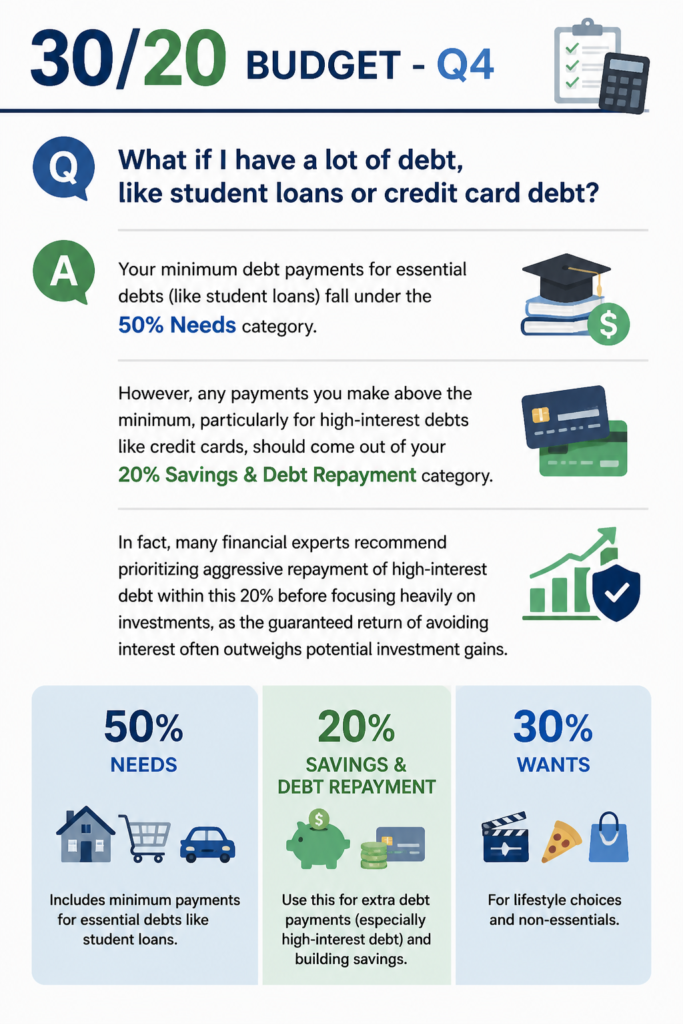

Q4: What if I have a lot of debt, like student loans or credit card debt?

A: Your minimum debt payments for essential debts (like student loans) fall under the 50% “Needs” category. However, any payments you make above the minimum, particularly for high-interest debts like credit cards, should come out of your 20% “Savings & Debt Repayment” category. In fact, many financial experts recommend prioritizing aggressive repayment of high-interest debt within this 20% before focusing heavily on investments, as the guaranteed return of avoiding interest often outweighs potential investment gains.

💼 The Money Management Toolkit

Knowledge is power, but proper execution requires the right tools. Getting your financial life organized doesn't have to be overwhelming. These 5 physical management tools are exactly what successful households use to budget, track cash, and secure their most important assets.

📝 Clever Fox Budget Planner & Bill Organizer

The ultimate analog command center for your finances. Sometimes keeping your budget in an app just doesn't stick. Physically writing down your goals, tracking expenses, and planning for debt payoff creates a level of accountability that digital spreadsheets simply can't match.

💵 A6 Leather Cash Stuffing Binder

The viral tool that made the cash-envelope budgeting system popular again. By allocating actual physical cash to designated envelopes (groceries, dining out, fun money), you physically cap your spending, making it virtually impossible to overdraft or overspend.

🔥 Fireproof & Waterproof Document Safe

A critical piece of financial security that many families overlook. Protecting your passports, birth certificates, property deeds, and estate planning documents from disaster is just as important as protecting the money in your bank account.

🏷️ Brother P-Touch Digital Label Maker

The unsung hero of a functional home office. When tax season rolls around or you need to find an important receipt, having perfectly labeled and categorized filing cabinets or accordion folders saves hours of frustrating searches and potential late fees.

🔒 SentrySafe Compact Fireproof Lock Box

For the physical assets that need extra heavy-duty protection—think emergency cash reserves, hard drives with Bitcoin cold wallets, or physical precious metals. This compact, locking safe provides peace of mind that your physical wealth is secure at home.

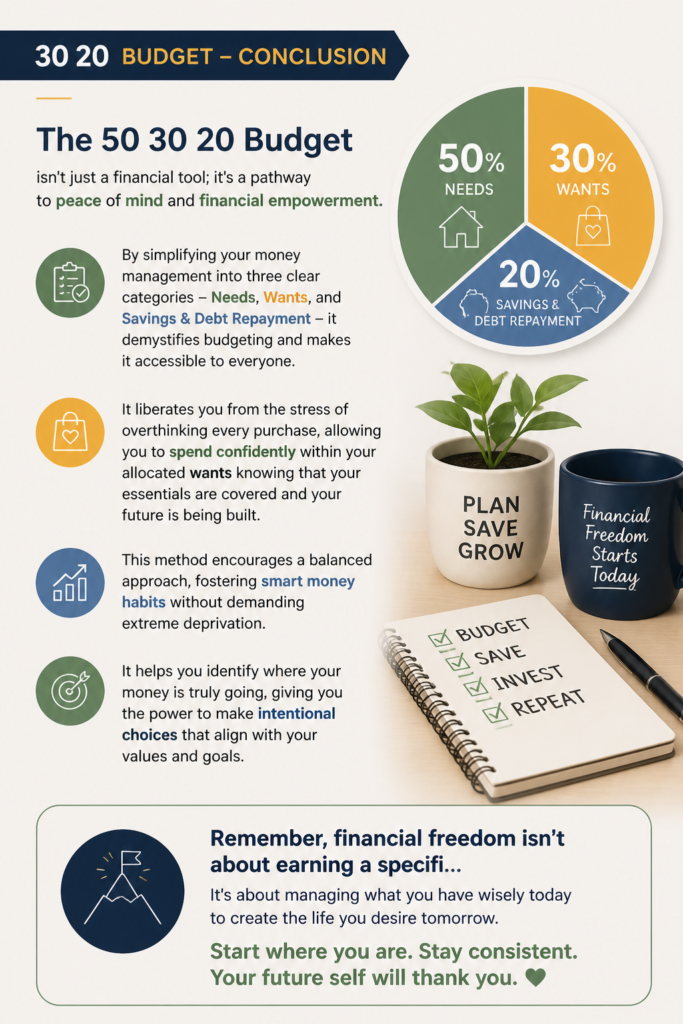

Conclusion

The 50 30 20 Budget isn’t just a financial tool; it’s a pathway to peace of mind and financial empowerment. By simplifying your money management into three clear categories – Needs, Wants, and Savings & Debt Repayment – it demystifies budgeting and makes it accessible to everyone. It liberates you from the stress of overthinking every purchase, allowing you to spend confidently within your allocated “wants” knowing that your essentials are covered and your future is being built.

This method encourages a balanced approach, fostering smart money habits without demanding extreme deprivation. It helps you identify where your money is truly going, giving you the power to make intentional choices that align with your values and goals. Remember, financial freedom isn’t about earning a specific amount; it’s about mastering the art of managing what you have effectively.

So, what are you waiting for? Take that first step today. Calculate your net income, track your spending for a month, and start allocating your money with purpose. The journey to financial clarity and wealth building begins with a single, smart decision. Embrace the 50 30 20 Budget, and watch as your financial future transforms before your eyes. You’ve got this!