🏡 2 Bedroom Bungalow Floor Plans

📚 The Financial Literacy Library

The best investment you can ever make is in your own financial education. These 5 cornerstone books are what millionaires, financial advisors, and wealth-builders universally recommend for completely rewiring how you think about earning, saving, and investing money.

🧠 The Psychology of Money

Doing well with money isn't necessarily about what you know—it's about how you behave. Morgan Housel masterfully breaks down the emotional and psychological biases that secretly dictate our financial decisions, offering a true paradigm shift in how to view wealth.

🏠 Rich Dad Poor Dad

The #1 personal finance book of all time for a reason. This foundational read shatters the myth that you need to earn a high income to be rich, teaching you the critical difference between working for money and making your money work for you via assets.

📈 Atomic Habits

While not strictly a finance book, building wealth is absolutely dependent on the daily habits you cultivate. James Clear provides the definitive framework for breaking bad spending habits and effortlessly automating the good ones that lead to long-term success.

📊 The Simple Path to Wealth

The ultimate antidote to complex, intimidating financial advice. JL Collins provides an incredibly accessible, low-stress roadmap to financial independence through index fund investing, perfectly explaining why simplicity beats Wall Street complexity every time.

💳 I Will Teach You to Be Rich

A tactical, no-BS, 6-week program that actually works. Ramit Sethi teaches you how to crush debt, automate your savings, and negotiate your salary—all while guilt-free spending on the things you truly love. A must-read for modern money management.

Stepping onto the property ladder, downsizing, or simply seeking a smarter way to live? The allure of a home that perfectly balances comfort, efficiency, and affordability is universal. Enter the 2-bedroom bungalow – a charming, practical, and increasingly popular choice that’s more than just a house; it’s a strategic move towards financial freedom. In a world where every dollar counts, embracing a lifestyle that prioritizes smart spending and mindful living can be the key to unlocking your wealth-building potential. This comprehensive guide will not only walk you through the ins and outs of 2-bedroom bungalow floor plans but will also equip you with the money-smart strategies to make this dream a reality, turning your home into a powerful asset in your financial journey. Get ready to discover how thoughtful design and savvy financial planning can go hand-in-hand to build the life you’ve always envisioned.

What is 2 Bedroom Bungalow Floor Plans?

At its heart, a bungalow is a single-story dwelling, celebrated for its compact footprint and efficient use of space. When we talk about “2 Bedroom Bungalow Floor Plans,” we’re referring to the architectural blueprints and layouts for these charming, single-level homes that feature two distinct sleeping areas. This specific configuration strikes a sweet spot for many homeowners, offering enough room for comfort and versatility without the financial and maintenance burdens often associated with larger properties.

Imagine a home where every square foot serves a purpose, where heating and cooling costs are naturally lower, and where accessibility is built into its very design. That’s the essence of a 2-bedroom bungalow. These homes typically feature an open-concept living area, seamlessly connecting the living room, dining space, and kitchen, fostering a sense of spaciousness and community. The two bedrooms are often strategically placed for privacy, with one serving as the primary suite and the other as a flexible space – perhaps a guest room, a home office, or a nursery.

From a money-smart perspective, the appeal of a 2-bedroom bungalow is immense. Its smaller size inherently translates to several financial advantages:

Lower Construction Costs: Less material, simpler foundation, and no need for complex staircases mean reduced building expenses if you’re constructing new.

Reduced Property Taxes: Generally, property taxes are calculated based on the home’s size and value. A smaller home often means a lower tax bill, freeing up more cash flow for savings or investments.

Lower Utility Bills: Heating and cooling a single-story, compact space is significantly more energy-efficient than a multi-story, sprawling home. This translates to substantial monthly savings on electricity and gas, putting money back into your pocket.

Easier and Cheaper Maintenance: Less exterior wall space to paint, fewer windows to clean, and simpler roofing means lower maintenance costs over the lifespan of the home. DIY repairs are often more manageable, saving on professional labor fees.

Enhanced Accessibility: With no stairs, bungalows are ideal for aging in place, those with mobility challenges, or families with young children. This long-term suitability can save future renovation costs or the expense of moving.

Versatility for Income Generation: The second bedroom can be a powerful asset. With proper zoning and planning, it could potentially be rented out for short-term stays (e.g., Airbnb) or long-term tenancy, providing a valuable income stream to offset mortgage payments or accelerate debt repayment. This transforms a functional space into a wealth-building tool.

In essence, a 2-bedroom bungalow isn’t just a dwelling; it’s a conscious financial decision that promotes efficient living, reduces ongoing expenses, and can serve as a solid foundation for your wealth-building journey. It’s about living smarter, not necessarily bigger, and channeling those savings into your financial future.

Key Features

The magic of 2-bedroom bungalow floor plans lies in their ability to combine practicality with charm, offering features that directly contribute to a money-smart and comfortable lifestyle. Understanding these key features helps you appreciate their value beyond just square footage.

Efficient, Open-Concept Layouts: Most 2-bedroom bungalows embrace open-concept living, where the kitchen, dining, and living areas flow seamlessly into one another. This design makes the home feel larger and more airy, maximizing usable space. From a financial standpoint, less wasted space means you’re paying for functionality, not just empty corridors. It also encourages a minimalist lifestyle, reducing the temptation to accumulate unnecessary clutter, which can save you money on storage solutions and impulse buys.

Optimized Energy Efficiency: Due to their compact, single-story nature, bungalows are inherently easier to heat and cool. Modern 2-bedroom bungalow plans often integrate features like strategically placed windows for natural light and ventilation, high-quality insulation, and efficient HVAC systems. This translates directly to lower utility bills month after month. Imagine freeing up an extra $50-$100 (or more!) each month that you can then funnel into your emergency fund, investment portfolio, or towards paying down your mortgage faster.

Flexibility of the Second Bedroom: This isn’t just an extra sleeping space; it’s a versatile financial asset.

Home Office: For remote workers, this space becomes a dedicated office, potentially allowing for tax deductions related to home office expenses.

Guest Room/Rental Income: As mentioned, if local regulations permit, it can serve as a guest room or be rented out on platforms like Airbnb, generating supplementary income. This passive income stream can significantly boost your savings or help you reach financial milestones faster.

Hobby Space/Gym: It provides dedicated space for hobbies, reducing the need for expensive external memberships (e.g., gym, art studio).

Accessibility and Longevity: The absence of stairs makes bungalows ideal for all stages of life, from young families to empty nesters and retirees. This “aging-in-place” capability is a significant financial benefit, as it eliminates the potential future costs of extensive renovations to add accessibility features or the expensive process of moving to a more suitable home later in life.

Strong Connection to Outdoor Living: With a smaller indoor footprint, bungalows often place a greater emphasis on integrating indoor and outdoor spaces. Large windows, sliding glass doors, and direct access to patios or decks expand your living area affordably. A well-designed outdoor space can serve as an extension of your entertaining area, a tranquil retreat, or even a productive garden, adding value and enjoyment without the high costs of adding interior square footage.

Investment Potential and Resale Value: Two-bedroom bungalows are consistently in demand across various demographics – first-time buyers, small families, and downsizers. Their affordability, efficiency, and ease of maintenance make them highly attractive. This broad appeal often translates into strong resale value and potential for appreciation, making them a sound long-term investment in your wealth-building portfolio.

These features collectively paint a picture of a home that is not only comfortable and stylish but also a smart financial decision, designed to minimize expenses and maximize your ability to save and invest for the future.

How to Get Started

Embarking on the journey to own or build a 2-bedroom bungalow is an exciting step towards financial independence. Like any significant investment, it requires a clear roadmap, starting with a solid financial foundation. Here’s how to get started, focusing on actionable, money-smart strategies:

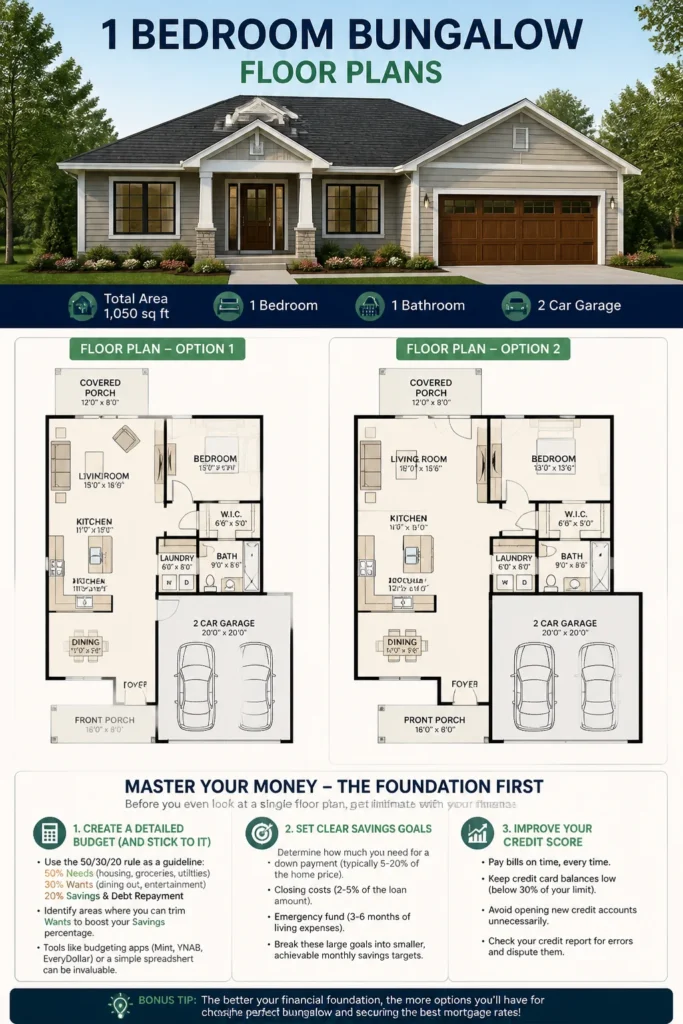

1. Master Your Money: The Foundation First

Before you even look at a single floor plan, get intimate with your finances. This is arguably the most critical step.

Create a Detailed Budget (and Stick to It!): This isn’t just about tracking spending; it’s about intentional living. Use the 50/30/20 rule as a guideline: 50% of your income for Needs (housing, groceries, utilities), 30% for Wants (dining out, entertainment), and 20% for Savings & Debt Repayment. Identify areas where you can trim “Wants” to boost your “Savings” percentage. Tools like budgeting apps (Mint, YNAB, EveryDollar) or a simple spreadsheet can be invaluable.

Set Clear Savings Goals: Determine how much you need for a down payment (typically 5-20% of the home price), closing costs (2-5% of the loan amount), and an emergency fund (3-6 months of living expenses). Break these down into monthly targets. For example, if you need $30,000 for a down payment in 3 years, that’s $833 per month.

Automate Your Savings: Set up automatic transfers from your checking account to a dedicated high-yield savings account on payday. “Out of sight, out of mind” works wonders for consistent saving. Treat this transfer like a non-negotiable bill.

Tackle High-Interest Debt: Prioritize paying off credit card debt or personal loans. The interest saved can be redirected towards your home fund. A lower debt-to-income ratio also strengthens your mortgage application.

Boost Your Credit Score: A higher credit score (generally 740+) can qualify you for better interest rates, saving you tens of thousands of dollars over the life of a mortgage. Pay bills on time, keep credit utilization low, and avoid opening new lines of credit.

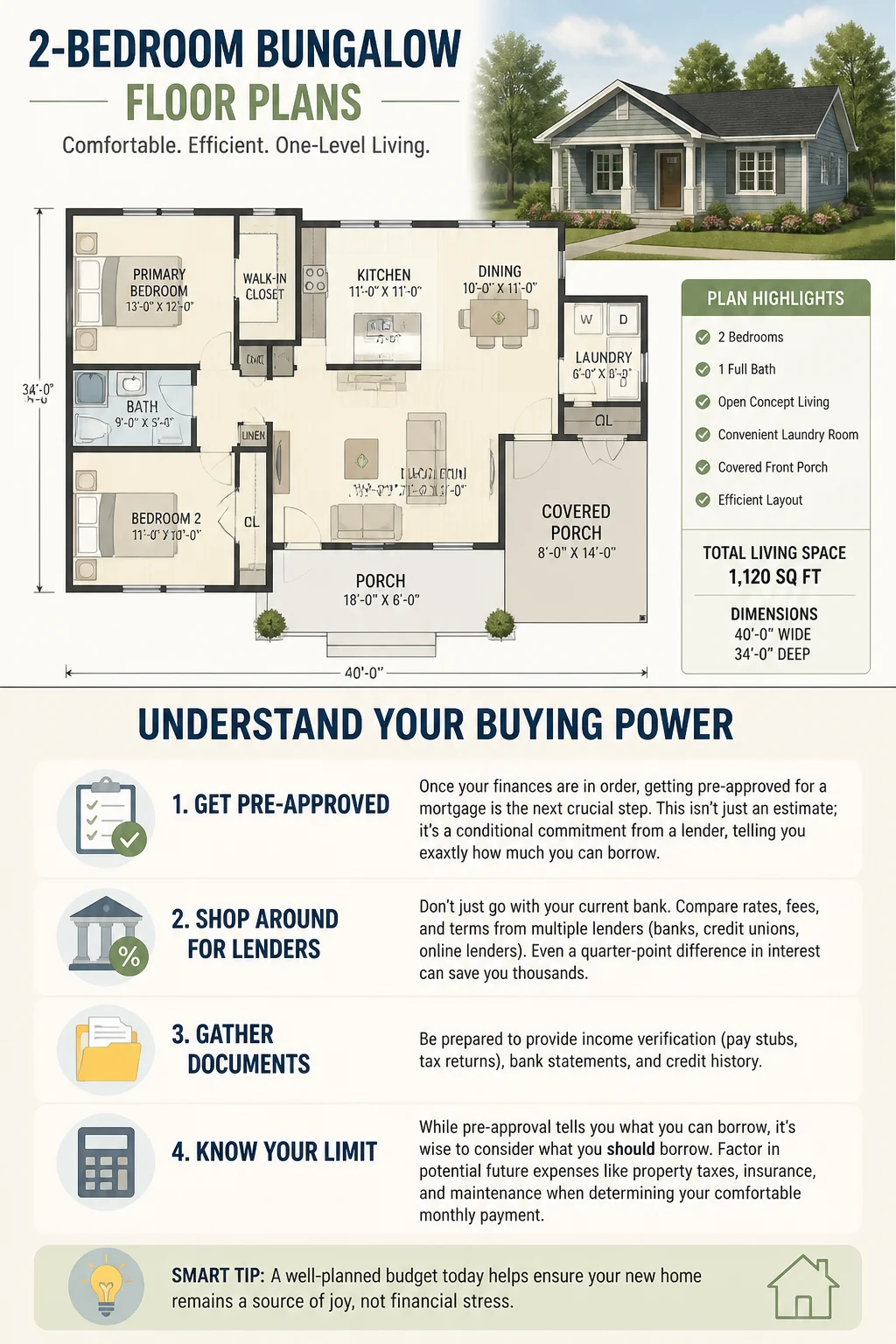

2. Understand Your Buying Power: Get Pre-Approved

Once your finances are in order, getting pre-approved for a mortgage is the next crucial step. This isn’t just an estimate; it’s a conditional commitment from a lender, telling you exactly how much you can borrow.

Shop Around for Lenders: Don’t just go with your current bank. Compare rates, fees, and terms from multiple lenders (banks, credit unions, online lenders). Even a quarter-point difference in interest can save you thousands.

Gather Documents: Be prepared to provide income verification (pay stubs, tax returns), bank statements, and credit history.

Know Your Limit: While pre-approval tells you what you can borrow, it’s wise to consider what you should borrow. Factor in potential future expenses like property taxes, insurance, and maintenance when determining your comfortable monthly payment.

3. Research and Define Your Dream Bungalow

Now for the fun part – envisioning your future home!

Needs vs. Wants List: What are your non-negotiables (e.g., specific number of bathrooms, a dedicated home office space)? What are nice-to-haves but not deal-breakers (e.g., granite countertops, a large backyard)? Prioritizing helps keep you grounded and on budget.

Explore Floor Plans: Dive into online resources (Pinterest, architectural plan websites, home design magazines). Look at different layouts, consider how natural light flows, and imagine your daily routine in various configurations. Pay attention to how the two bedrooms are situated for privacy and functionality.

Consider Location & Lifestyle: How does the bungalow fit into your desired community? Proximity to work, schools, amenities, and public transport can impact your daily expenses (e.g., gas, childcare).

Think Long-Term: While a 2-bedroom bungalow is perfect now, consider your 5-10 year plan. Is there potential to expand, add a sunroom, or finish a basement if your needs change?

4. Assemble Your Team

You don’t have to navigate this journey alone.

Real Estate Agent: Find an agent experienced with bungalows in your target areas. They can offer valuable insights, negotiate on your behalf, and guide you through the buying process. Look for someone who understands your financial goals.

Financial Advisor (Optional but Recommended): For comprehensive wealth planning, a financial advisor can help integrate your home purchase into your broader investment strategy, retirement planning, and tax considerations.

Contractor/Architect (If Building): If you plan to build, engage with reputable professionals early. They can help refine your chosen floor plan to optimize costs and functionality.

By systematically addressing these steps, you’ll build a strong financial foundation, gain clarity on your budget, and be well-prepared to confidently pursue your 2-bedroom bungalow dream.

Tips for Success

Making your 2-bedroom bungalow a cornerstone of your financial well-being requires more than just buying it; it’s about smart living and continuous wealth-building. Here are some pro tips to ensure long-term success:

1. Master the Art of Smart Saving & Budgeting

Your financial discipline shouldn’t end once you’ve secured your home.

Automate Everything Possible: Beyond your initial home savings, automate transfers for future home maintenance (e.g., $50-$100/month), property taxes (if not escrowed), and investment contributions. This consistent, hands-off approach builds wealth effortlessly.

Embrace the “Sinking Fund” Strategy: Create separate savings buckets (sinking funds) for predictable but infrequent expenses like home insurance premiums, appliance replacements, or future renovation projects. This prevents financial shocks and keeps your main emergency fund intact.

Audit Your Expenses Regularly: Treat your budget as a living document. Review it quarterly to identify areas where you can cut back or where spending has crept up. Small adjustments can lead to significant annual savings.

Meal Prep Like a Pro: Eating out is a major budget killer. Planning and preparing meals at home, even for just a few days a week, can save hundreds monthly. This money can then be funneled into your mortgage principal or investments.

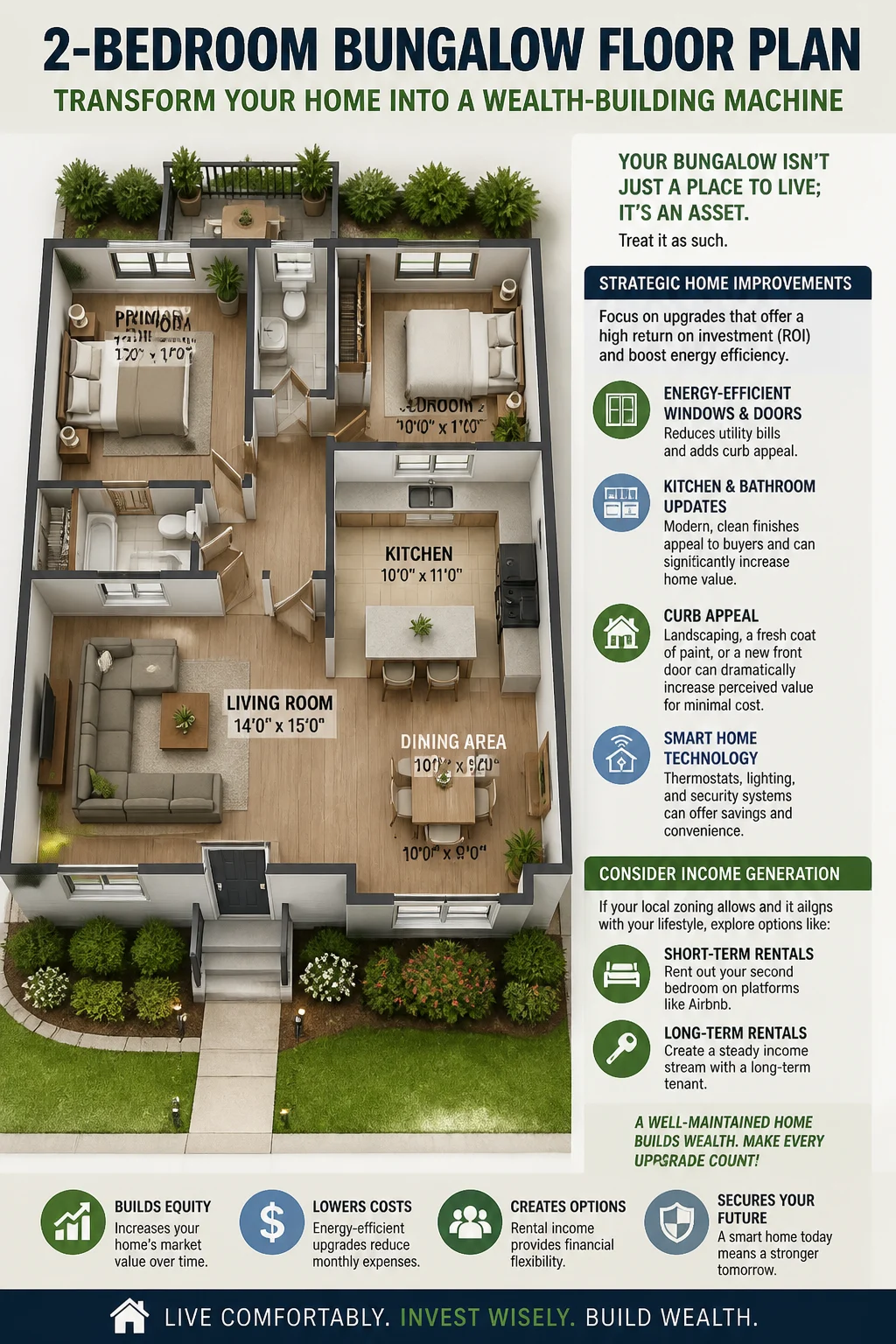

2. Transform Your Home into a Wealth-Building Machine

Your bungalow isn’t just a place to live; it’s an asset. Treat it as such.

Strategic Home Improvements: Focus on upgrades that offer a high return on investment (ROI) and boost energy efficiency.

Energy-Efficient Windows & Doors: Reduces utility bills and adds curb appeal.

Kitchen & Bathroom Updates: Modern, clean finishes appeal to buyers and can significantly increase home value.

Curb Appeal: Landscaping, a fresh coat of paint, or a new front door can dramatically increase perceived value for minimal cost.

Smart Home Technology: Thermostats, lighting, and security systems can offer savings and convenience.

Consider Income Generation: If your local zoning allows and it aligns with your lifestyle, explore options like short-term rentals for your second bedroom or even long-term rental if you consider moving out temporarily. This supplementary income can accelerate mortgage repayment or fund other investments.

Understand Equity: As you pay down your mortgage and your property value potentially appreciates, you build equity. This equity can be leveraged responsibly in the future for major life events or further investments, but always consult a financial advisor before tapping into it.

3. Be Your Own Handyperson (Within Reason)

Labor costs for home repairs can be staggering.

Learn Basic DIY Skills: Simple tasks like changing air filters, fixing leaky faucets, patching drywall, or basic landscaping can save hundreds. YouTube tutorials are your best friend here.

Regular Preventative Maintenance: Proactively cleaning gutters, checking for leaks, and servicing HVAC systems can prevent minor issues from becoming costly major repairs. A small investment of time can save a lot of money.

Know When to Call a Pro: Don’t attempt complex electrical, plumbing, or structural work if you’re not qualified. Mistakes can be dangerous and far more expensive to fix. Build a network of trusted, reasonably priced local contractors.

4. Negotiate Fearlessly and Wisely

From buying the home to hiring contractors, negotiation is a powerful money-saving skill.

Home Purchase: Don’t be afraid to negotiate the asking price, closing costs, or request specific repairs based on the home inspection report. Every dollar saved upfront is a dollar in your pocket.

Contractor Quotes: Always get at least three quotes for any major repair or renovation project. Compare not just price, but also scope of work, timeline, and contractor reviews.

Insurance Policies: Review your homeowner’s insurance annually and shop around for better rates. Bundling with auto insurance often provides discounts.

By integrating these tips into your approach, your 2-bedroom bungalow will not only provide a comfortable, efficient home but will actively contribute to your financial growth and security.

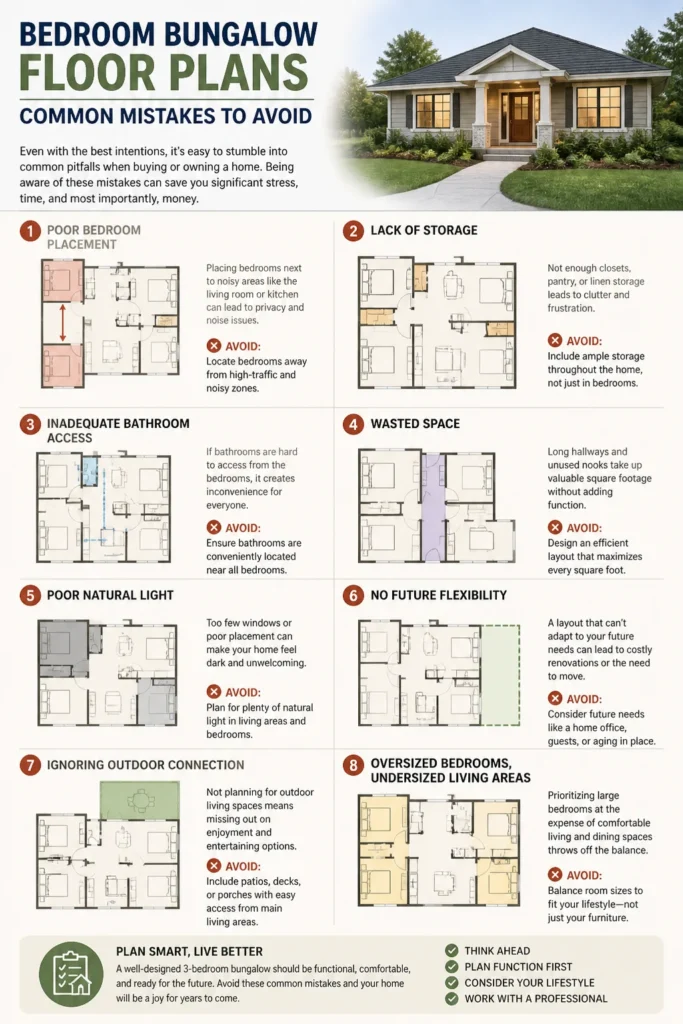

Common Mistakes to Avoid

Even with the best intentions, it’s easy to stumble into common pitfalls when buying or owning a home. Being aware of these mistakes can save you significant stress, time, and most importantly, money.

Overspending on the “Dream”

It’s easy to get caught up in the emotional excitement of homeownership and fall in love with features or a property that stretches your budget too thin. The Mistake: Buying at the absolute top of your pre-approved limit, or worse, going over it. This leaves no financial wiggle room for unexpected expenses or future goals.

Money-Smart Solution: Stick to your budget like glue. Remember, your pre-approval amount is the maximum a bank will lend you, not necessarily what you should spend. Aim to buy comfortably below your maximum to leave breathing room for an emergency fund, investments, and life’s little pleasures. Distinguish between “needs” and “wants” and be prepared to compromise on non-essentials.

Ignoring Hidden Costs and Future Expenses

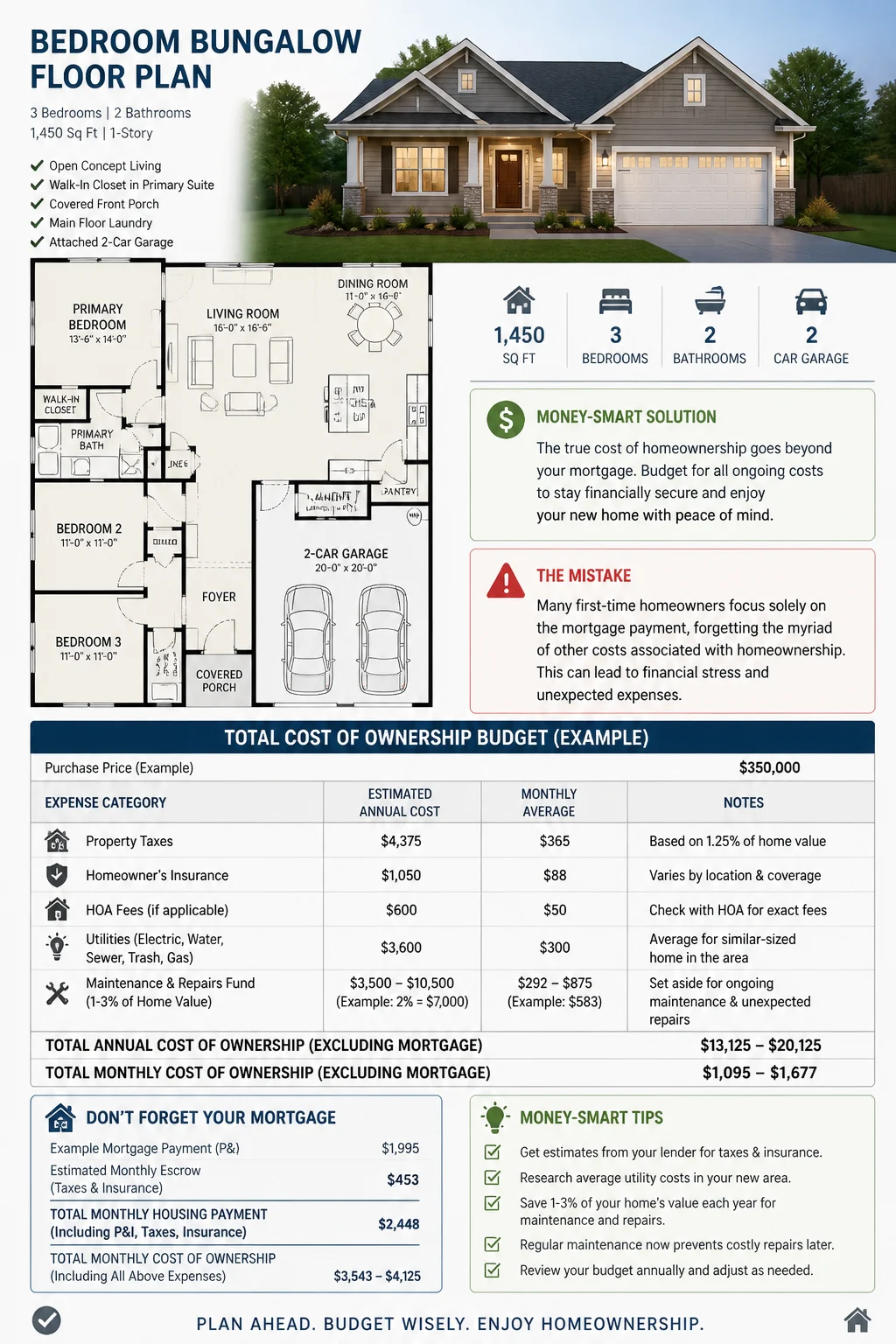

Many first-time homeowners focus solely on the mortgage payment, forgetting the myriad of other costs associated with homeownership. The Mistake: Not budgeting for property taxes, homeowner’s insurance, HOA fees (if applicable), utilities, and crucially, an ongoing maintenance fund.

Money-Smart Solution: Create a comprehensive “total cost of ownership” budget. Factor in estimated property taxes and insurance (your lender can provide these), average utility costs for a similar-sized home in the area, and allocate at least 1-3% of the home’s value annually for maintenance and repairs. This proactive budgeting prevents financial surprises.

Skipping or Rushing the Home Inspection

A home inspection might seem like an extra expense, but it’s a critical investment. The Mistake: Waiving a home inspection to make your offer more attractive in a competitive market, or choosing a cheap, inexperienced inspector.

Money-Smart Solution: Always, always get a thorough home inspection by a qualified professional. This can uncover costly structural issues, plumbing problems, electrical hazards, or roof damage that could cost you tens of thousands down the line. Use the inspection report as a negotiation tool for repairs or a price reduction.

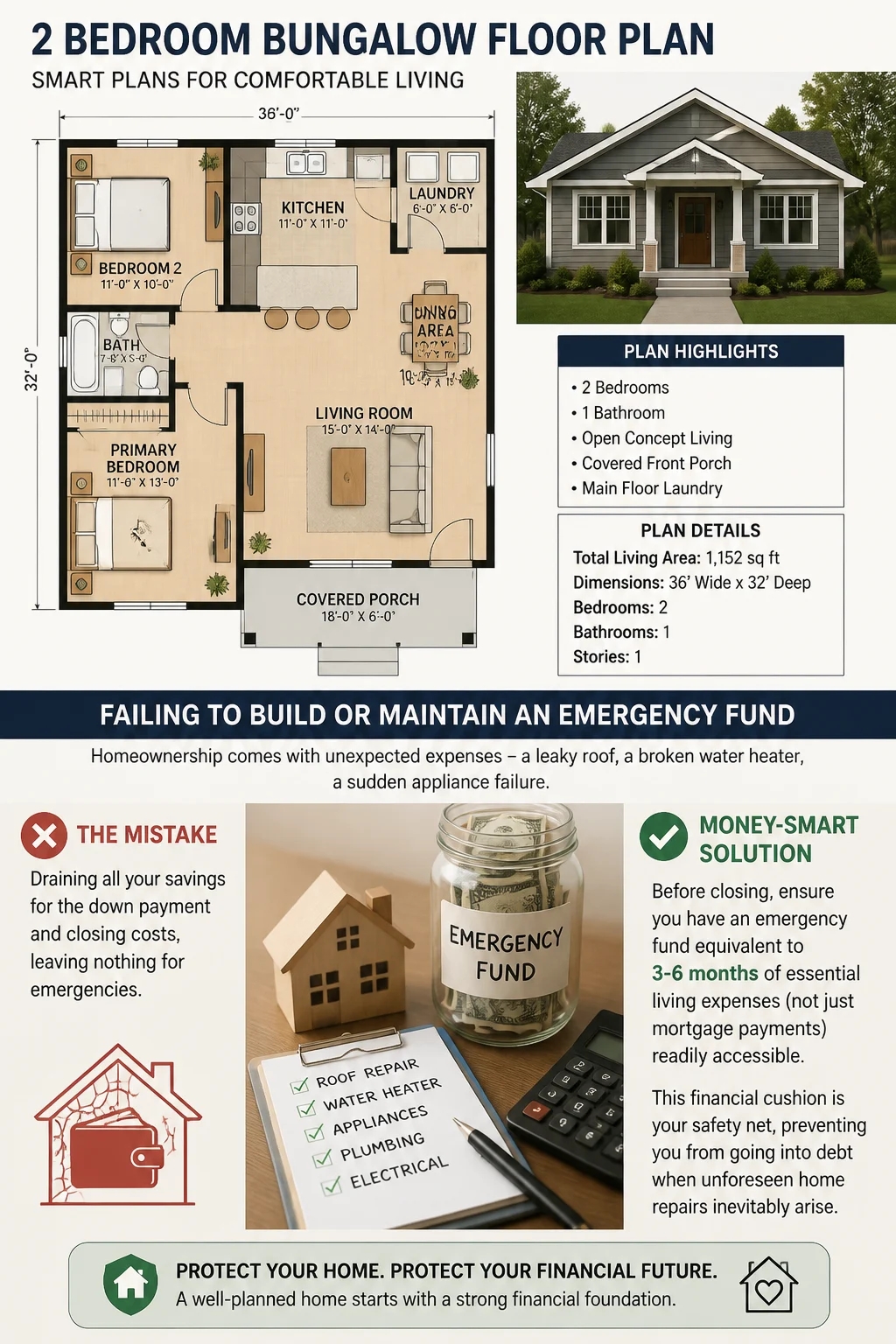

Failing to Build or Maintain an Emergency Fund

Homeownership comes with unexpected expenses – a leaky roof, a broken water heater, a sudden appliance failure. The Mistake: Draining all your savings for the down payment and closing costs, leaving nothing for emergencies.

Money-Smart Solution: Before closing, ensure you have an emergency fund equivalent to 3-6 months of essential living expenses (not just mortgage payments) readily accessible. This financial cushion is your safety net, preventing you from going into debt when unforeseen home repairs inevitably arise.

Neglecting Regular Maintenance

A “set it and forget it” approach to home maintenance can lead to expensive problems. The Mistake: Ignoring small issues like a dripping faucet, clogged gutters, or a drafty window, which can escalate into major repairs.

Money-Smart Solution: Develop a seasonal maintenance checklist. Spend a few hours each spring and fall addressing minor upkeep tasks. Regular preventative maintenance, like cleaning gutters, checking smoke detectors, and servicing your HVAC system, can significantly extend the life of your home’s components and prevent costly breakdowns.

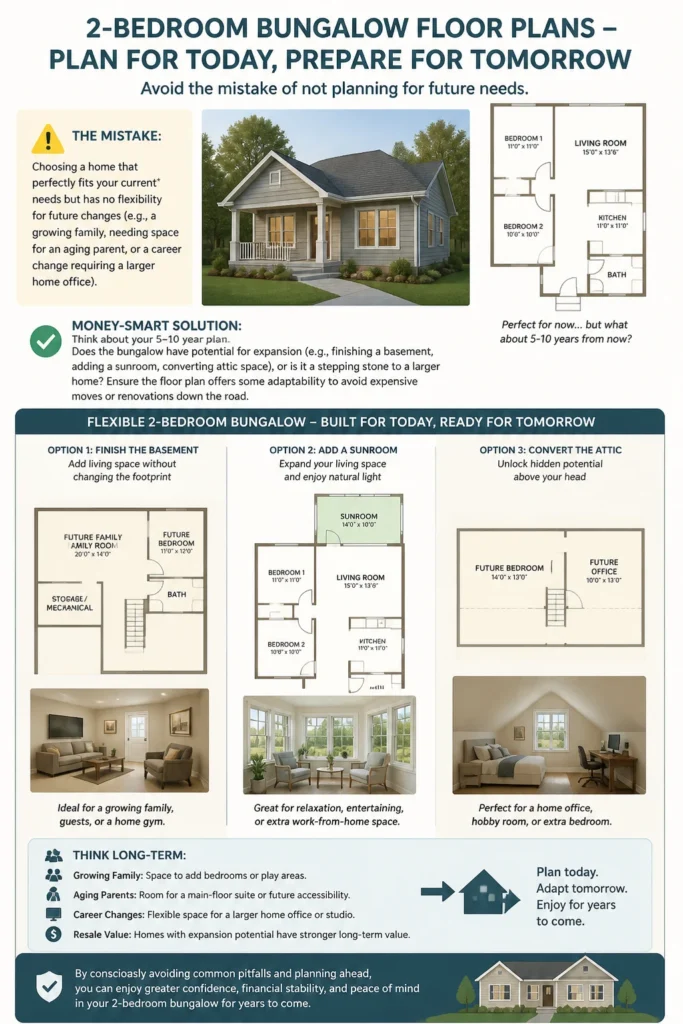

Not Planning for Future Needs

While a 2-bedroom bungalow is perfect for many, consider your long-term life trajectory. The Mistake: Choosing a home that perfectly fits your current* needs but has no flexibility for future changes (e.g., a growing family, needing space for an aging parent, or a career change requiring a larger home office).

Money-Smart Solution: Think about your 5-10 year plan. Does the bungalow have potential for expansion (e.g., finishing a basement, adding a sunroom, converting attic space), or is it a stepping stone to a larger home? Ensure the floor plan offers some adaptability to avoid expensive moves or renovations down the line.

By consciously avoiding these common pitfalls, you can navigate the journey of buying and owning a 2-bedroom bungalow with greater confidence, financial stability, and peace of mind, truly making it a smart investment in your future.

FAQ

Here are answers to some common questions about 2-bedroom bungalow floor plans, with a money-smart perspective.

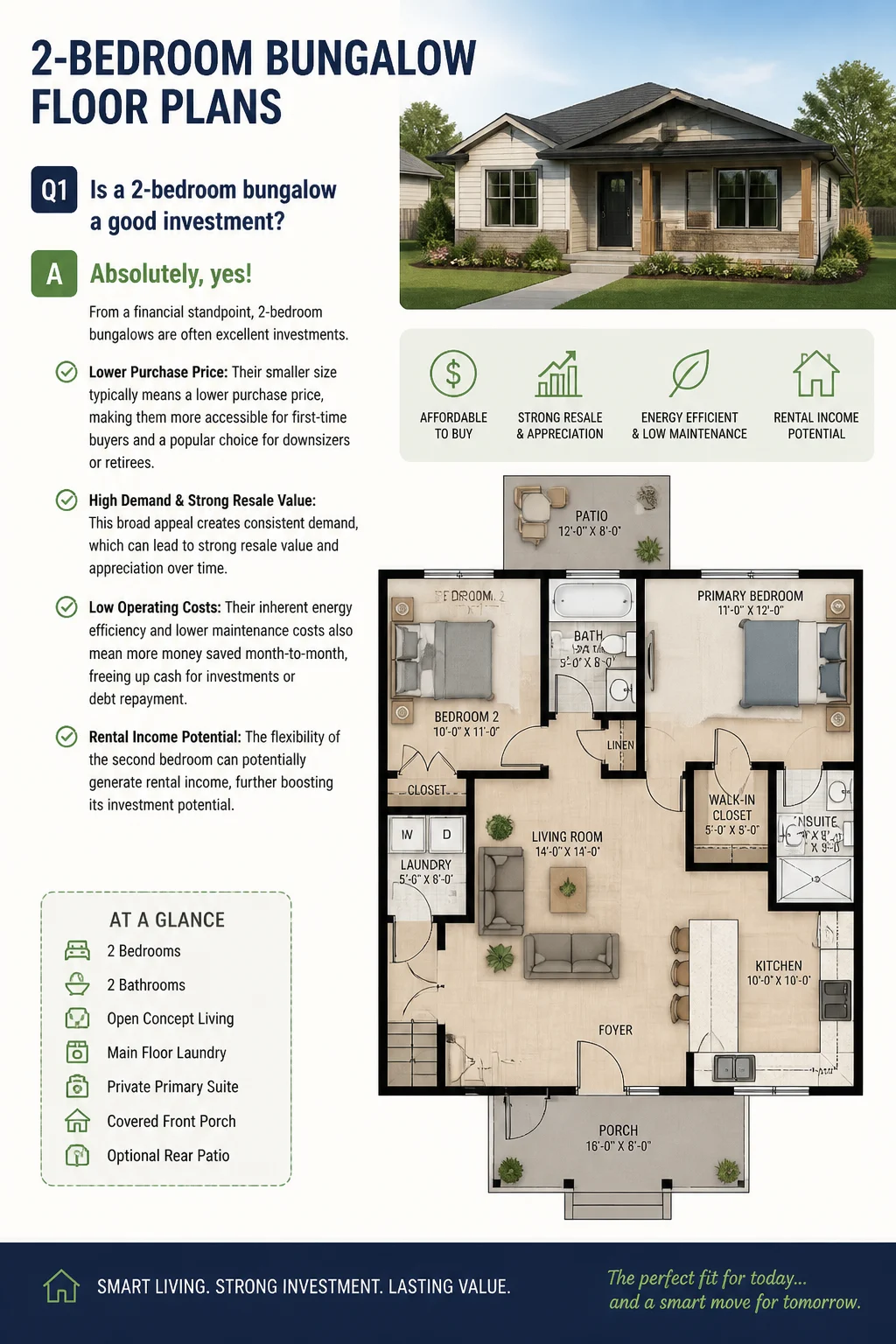

Q1: Is a 2-bedroom bungalow a good investment?

A: Absolutely, yes! From a financial standpoint, 2-bedroom bungalows are often excellent investments. Their smaller size typically means a lower purchase price, making them more accessible for first-time buyers and a popular choice for downsizers or retirees. This broad appeal creates consistent demand, which can lead to strong resale value and appreciation over time. Their inherent energy efficiency and lower maintenance costs also mean more money saved month-to-month, freeing up cash for investments or debt repayment. Plus, the flexibility of the second bedroom can potentially generate rental income, further boosting its investment potential.

Q2: How much does it cost to build a 2-bedroom bungalow versus buying an existing one?

A: It varies significantly based on location, material costs, labor, and the complexity of your chosen floor plan and finishes. Generally, building new can sometimes be more expensive upfront due to land costs, permits, and construction, but it offers the advantage of modern energy efficiency, personalized design, and often lower immediate maintenance. Buying an existing bungalow might be more affordable initially, but you might inherit older systems that require future repairs or renovations. To make a money-smart decision, get detailed quotes from multiple builders if considering new construction, and thoroughly research comparable sales (comps) and get a comprehensive inspection if buying existing. Always budget for a 10-15% contingency fund when building.

Q3: Can I add value to a 2-bedroom bungalow?

A: Definitely! Strategic upgrades can significantly increase your bungalow’s value and appeal. Focus on improvements with high ROI:

- Energy-Efficient Upgrades: New windows, doors, insulation, and an updated HVAC system reduce utility bills and are highly attractive to buyers.

- Kitchen and Bathroom Renovations: These areas often yield the highest returns. Focus on fresh, modern, and neutral finishes.

- Curb Appeal: Landscaping, a fresh coat of exterior paint, a new front door, or a well-maintained porch instantly boost perceived value.

- Outdoor Living Spaces: Adding a deck, patio, or well-designed garden expands your usable living area affordably.

- Maximizing Interior Space: Smart storage solutions, built-in shelving, or opening up a wall (if non-load-bearing) can enhance functionality.

Always research local market trends and consult with a real estate agent to ensure your renovations align with what buyers in your area are looking for.

Q4: Are 2-bedroom bungalows suitable for families?

A: Yes, for many families! While they might not suit very large families, 2-bedroom bungalows are ideal for small families, single parents, or families with young children. The single-story layout offers excellent accessibility and safety, as there are no stairs for toddlers to navigate. The open-concept living often found in bungalows encourages family interaction. The second bedroom can serve as a child’s room, a nursery, or even a shared space for two younger children. For families, the lower carrying costs and maintenance free up more funds for childcare, education, and family experiences, making it a very practical and money-smart choice.

💼 The Money Management Toolkit

Knowledge is power, but proper execution requires the right tools. Getting your financial life organized doesn't have to be overwhelming. These 5 physical management tools are exactly what successful households use to budget, track cash, and secure their most important assets.

📝 Clever Fox Budget Planner & Bill Organizer

The ultimate analog command center for your finances. Sometimes keeping your budget in an app just doesn't stick. Physically writing down your goals, tracking expenses, and planning for debt payoff creates a level of accountability that digital spreadsheets simply can't match.

💵 A6 Leather Cash Stuffing Binder

The viral tool that made the cash-envelope budgeting system popular again. By allocating actual physical cash to designated envelopes (groceries, dining out, fun money), you physically cap your spending, making it virtually impossible to overdraft or overspend.

🔥 Fireproof & Waterproof Document Safe

A critical piece of financial security that many families overlook. Protecting your passports, birth certificates, property deeds, and estate planning documents from disaster is just as important as protecting the money in your bank account.

🏷️ Brother P-Touch Digital Label Maker

The unsung hero of a functional home office. When tax season rolls around or you need to find an important receipt, having perfectly labeled and categorized filing cabinets or accordion folders saves hours of frustrating searches and potential late fees.

🔒 SentrySafe Compact Fireproof Lock Box

For the physical assets that need extra heavy-duty protection—think emergency cash reserves, hard drives with Bitcoin cold wallets, or physical precious metals. This compact, locking safe provides peace of mind that your physical wealth is secure at home.

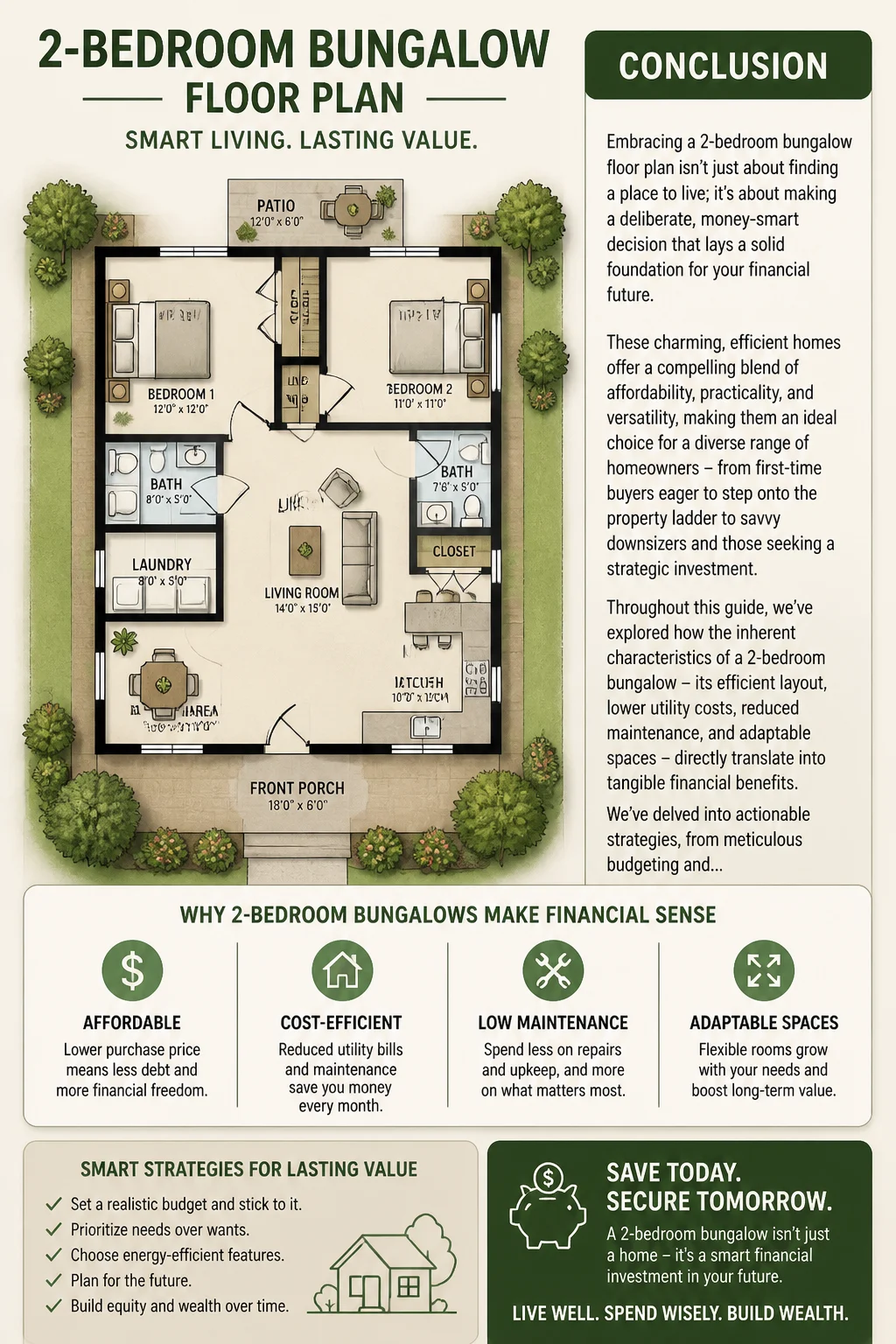

Conclusion

Embracing a 2-bedroom bungalow floor plan isn’t just about finding a place to live; it’s about making a deliberate, money-smart decision that lays a solid foundation for your financial future. These charming, efficient homes offer a compelling blend of affordability, practicality, and versatility, making them an ideal choice for a diverse range of homeowners – from first-time buyers eager to step onto the property ladder to savvy downsizers and those seeking a strategic investment.

Throughout this guide, we’ve explored how the inherent characteristics of a 2-bedroom bungalow – its efficient layout, lower utility costs, reduced maintenance, and adaptable spaces – directly translate into tangible financial benefits. We’ve delved into actionable strategies, from meticulous budgeting and automated savings to strategic home improvements and fearless negotiation, all designed to help you not just acquire a home, but to build lasting wealth.

Remember, the journey to financial freedom is paved with smart choices. By understanding the true value of a 2-bedroom bungalow, avoiding common pitfalls, and adopting a proactive, money-smart mindset, you transform a simple dwelling into a powerful asset. It’s about living intentionally, maximizing your resources, and creating a comfortable, sustainable lifestyle that fuels your long-term financial goals.

So, are you ready to take the reins of your financial destiny? Start today. Begin by scrutinizing your budget, setting clear savings goals, and exploring the myriad of 2-bedroom bungalow floor plans that await. Your dream of a beautiful, efficient home and a robust financial future is not just achievable; it’s within your reach. Take that first step, and watch your wealth grow, one smart decision at a time.