💰 How To Pick Winning Lottery Numbers

📚 The Financial Literacy Library

The best investment you can ever make is in your own financial education. These 5 cornerstone books are what millionaires, financial advisors, and wealth-builders universally recommend for completely rewiring how you think about earning, saving, and investing money.

🧠 The Psychology of Money

Doing well with money isn't necessarily about what you know—it's about how you behave. Morgan Housel masterfully breaks down the emotional and psychological biases that secretly dictate our financial decisions, offering a true paradigm shift in how to view wealth.

🏠 Rich Dad Poor Dad

The #1 personal finance book of all time for a reason. This foundational read shatters the myth that you need to earn a high income to be rich, teaching you the critical difference between working for money and making your money work for you via assets.

📈 Atomic Habits

While not strictly a finance book, building wealth is absolutely dependent on the daily habits you cultivate. James Clear provides the definitive framework for breaking bad spending habits and effortlessly automating the good ones that lead to long-term success.

📊 The Simple Path to Wealth

The ultimate antidote to complex, intimidating financial advice. JL Collins provides an incredibly accessible, low-stress roadmap to financial independence through index fund investing, perfectly explaining why simplicity beats Wall Street complexity every time.

💳 I Will Teach You to Be Rich

A tactical, no-BS, 6-week program that actually works. Ramit Sethi teaches you how to crush debt, automate your savings, and negotiate your salary—all while guilt-free spending on the things you truly love. A must-read for modern money management.

Are you tired of playing the lottery, hoping for that one big win that will magically solve all your financial woes? What if I told you there’s a far more reliable, proven method to achieve financial freedom – a “lottery” where you control the odds, and the winnings are virtually guaranteed? This guide isn’t about predicting random numbers; it’s about picking the winning habits and mindset that will build true, lasting wealth.

Quick Overview

This guide will empower you to redefine “winning” and equip you with practical, actionable strategies to build a solid financial future, far more effectively than any lottery ticket ever could. You’ll learn to budget, save, invest, and cultivate a wealth-building mindset that transforms your financial reality.

Time needed: Approximately 60-90 minutes for initial setup and understanding, with ongoing commitment for lasting results.

Difficulty: Beginner

What you’ll need: A pen and paper (or digital equivalent), internet access, an open mind, and a genuine desire to take control of your financial destiny.

Step-by-Step Instructions

Step 1: Redefine Your “Winning Numbers”

Forget the 1 in a million odds of the actual lottery. The true “winning numbers” are your income, your savings rate, your investment returns, and your debt-to-income ratio. Your first step is to shift your perspective from passive hope to active empowerment. Understand that wealth isn’t primarily built on luck, but on consistent, smart financial decisions. This mindset shift is the most crucial “number” you’ll ever pick. It’s about understanding that every dollar saved and invested is a “winning number” that compounds over time, far more reliably than any jackpot.

Pro tip: Start by visualizing your ideal financial future. What does financial freedom look like to you? Is it debt-free living, early retirement, owning a home, or traveling the world? Having a clear vision makes the subsequent steps much more motivating.

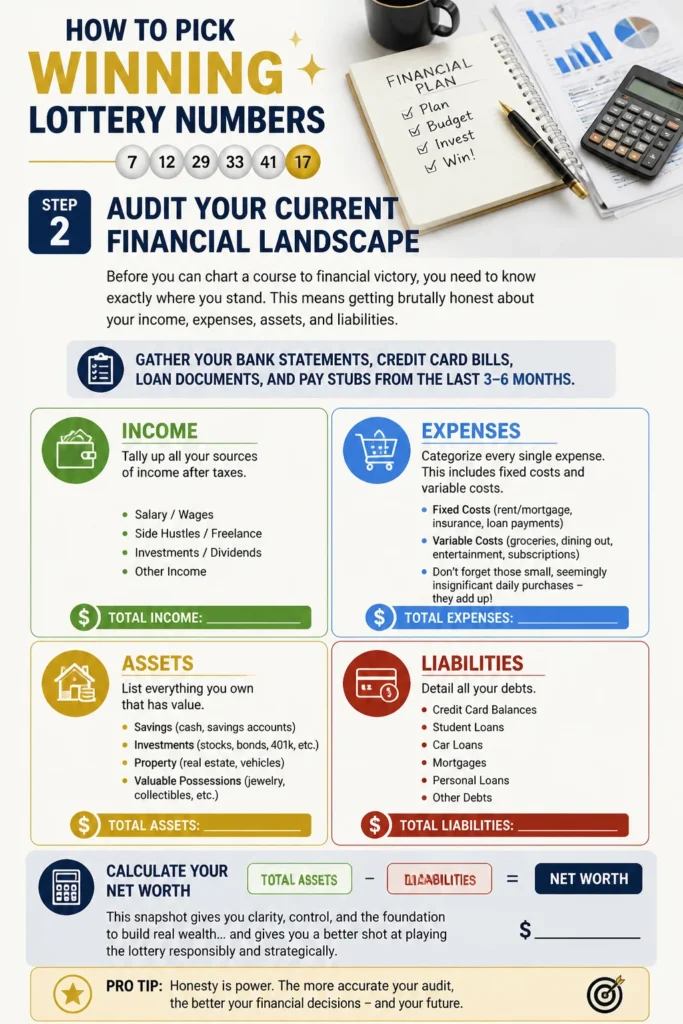

Step 2: Audit Your Current Financial Landscape

Before you can chart a course to financial victory, you need to know exactly where you stand. This means getting brutally honest about your income, expenses, assets, and liabilities. Gather your bank statements, credit card bills, loan documents, and pay stubs from the last 3-6 months.

Income: Tally up all your sources of income after taxes.

Expenses: Categorize every single expense. This includes fixed costs (rent/mortgage, insurance, loan payments) and variable costs (groceries, dining out, entertainment, subscriptions). Don’t forget those small, seemingly insignificant daily purchases – they add up!

Assets: List everything you own that has value (savings, investments, property, valuable possessions).

Liabilities: Detail all your debts (credit card balances, student loans, car loans, mortgage).

This step can be eye-opening, revealing exactly where your money is going and identifying potential “leaks” in your financial bucket.

Pro tip: Use a spreadsheet, a budgeting app (like Mint, YNAB, or Personal Capital), or even a simple notebook to track everything. The key is consistency and accuracy. Don’t judge yourself; just observe the data.

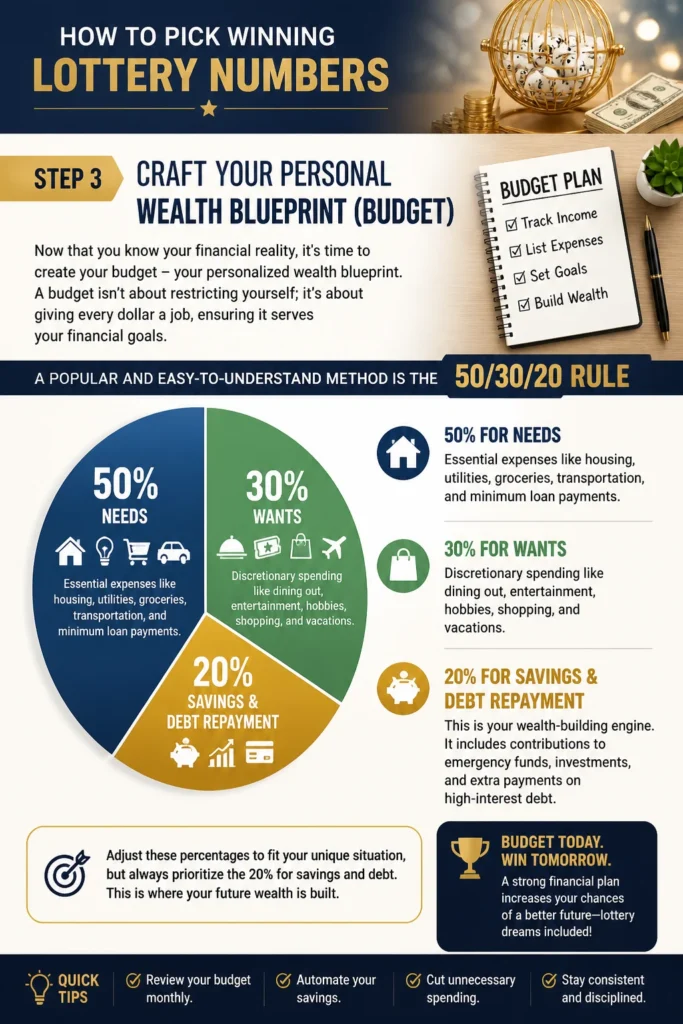

Step 3: Craft Your Personal “Wealth Blueprint” (Budget)

Now that you know your financial reality, it’s time to create your budget – your personalized “wealth blueprint.” A budget isn’t about restricting yourself; it’s about giving every dollar a job, ensuring it serves your financial goals. A popular and easy-to-understand method is the 50/30/20 rule:

50% for Needs: Essential expenses like housing, utilities, groceries, transportation, and minimum loan payments.

30% for Wants: Discretionary spending like dining out, entertainment, hobbies, shopping, and vacations.

20% for Savings & Debt Repayment: This is your wealth-building engine. It includes contributions to emergency funds, investments, and extra payments on high-interest debt.

Adjust these percentages to fit your unique situation, but always prioritize the 20% for savings and debt. This is where your true “winnings” accumulate.

Pro tip: Be realistic! An overly restrictive budget is hard to stick to. Start with a budget that feels manageable, then look for small areas to optimize over time. For example, can you cut one streaming service or pack your lunch twice a week? These small wins build momentum.

Step 4: Automate Your “Winning” Contributions (Savings)

One of the most powerful “winning numbers” you can pick is automation. Set up automatic transfers from your checking account to your savings and investment accounts on payday. This “pay yourself first” strategy ensures that your financial goals are prioritized before you even have a chance to spend the money. Even small, consistent contributions add up significantly over time thanks to the magic of compound interest. If you can automate 10-15% of your income towards savings and investments, you’re already picking winning numbers daily.

Pro tip: Treat your savings transfer like a non-negotiable bill. If you don’t see the money, you won’t miss it. Start small if you need to, perhaps just $50 a month, and gradually increase it as your income grows or you find more areas to save.

Step 5: Strategize Your Debt Annihilation

High-interest debt (like credit card debt or personal loans) is like a financial black hole, sucking away your potential “winnings.” Eliminating it should be a top priority after securing a small emergency fund. Two popular strategies are:

Debt Snowball: List your debts from smallest balance to largest. Pay minimums on all but the smallest, then throw every extra dollar at the smallest debt until it’s gone. Then roll that payment amount into the next smallest debt. The psychological wins keep you motivated.

Debt Avalanche: List your debts from highest interest rate to lowest. Pay minimums on all but the highest interest debt, then attack that one aggressively. This method saves you the most money on interest.

Choose the method that best suits your personality and stick with it. Every dollar you free from interest payments is a dollar you can put towards building wealth.

Pro tip: Negotiate with creditors! Sometimes, you can get a lower interest rate or set up a more manageable payment plan just by asking. Don’t be afraid to explore options like balance transfer cards (if you can pay it off within the promotional period) or debt consolidation loans.

Step 6: Cultivate Your “Investment Garden”

Once you have an emergency fund (3-6 months of living expenses) and a plan for high-interest debt, it’s time to put your money to work through investing. This is where your money truly starts to make money for you, picking up speed like a snowball rolling downhill. You don’t need to be rich to start investing.

Start Simple: Begin with low-cost index funds or ETFs (Exchange Traded Funds) that track broad market indices like the S&P 500. These offer diversification and typically outperform actively managed funds over the long term.

Utilize Retirement Accounts: Max out tax-advantaged accounts like a 401(k) (especially if your employer offers a match – that’s free money!) or an IRA (Traditional or Roth).

Time in the Market: The most crucial factor in investing is time. Start as early as possible and invest consistently. Don’t try to “time the market.”

Understanding compound interest is key here. A small amount invested early can grow into a substantial sum over decades.

Pro tip: Don’t let fear or lack of knowledge hold you back. Many robo-advisors (like Betterment or Wealthfront) can help you get started with a diversified portfolio based on your risk tolerance, with very low minimums and fees. Invest in what you understand, and keep learning.

Step 7: Master the Art of Mindful Spending

This step is about refining your spending habits to align with your values and financial goals. Instead of blindly spending, pause and ask yourself: “Does this purchase align with my wealth blueprint? Is this a need or a want? Is there a more cost-effective alternative?” Mindful spending isn’t about deprivation; it’s about conscious choices that empower you.

Delay Gratification: For non-essential purchases, try a “30-day rule.” If you still want it after 30 days, consider if it fits your budget.

Seek Value: Look for quality over quantity, and consider second-hand options for certain items.

Batch Errands: Save on gas and impulse buys by planning your shopping trips efficiently.

Cook at Home: Eating out is a major budget killer for many. Learning to cook a few simple meals can save hundreds each month.

Pro tip: Identify your “money leaks” – those categories where you consistently overspend. For many, it’s dining out, subscriptions, or impulse online shopping. Once identified, create specific strategies to reduce spending in those areas.

Step 8: Continuously Learn and Adapt

The financial landscape is always evolving, and so should your financial knowledge. Make a habit of regularly educating yourself. Read books on personal finance, follow reputable financial blogs, listen to podcasts, and stay informed about economic trends. The more you learn, the more confident and capable you’ll become in making smart financial decisions. Review your budget and financial goals quarterly or annually, making adjustments as your life circumstances change (e.g., new job, marriage, children).

Pro tip: Start with a classic like “The Total Money Makeover” by Dave Ramsey for debt elimination motivation, or “The Simple Path to Wealth” by J.L. Collins for straightforward investing advice. Even 15 minutes of learning a day can make a huge difference over time.

Common Mistakes to Avoid

1. Ignoring Your Budget or Not Having One:

Why it’s problematic: Without a budget, your money effectively disappears without a clear purpose. You’re flying blind, making it impossible to track progress or identify areas for improvement. This leads to living paycheck-to-paycheck, regardless of income.

Correct approach: Embrace budgeting as your financial GPS. Review it regularly, adjust it as needed, and make it a dynamic tool for your financial journey. Treat it as a spending plan that gives you freedom, not restriction.

2. Falling Victim to Lifestyle Creep:

Why it’s problematic: As your income increases, so does your spending. Instead of saving or investing the extra money, you upgrade your car, house, or dining habits. This ensures you never get ahead, always needing more to maintain your lifestyle.

Correct approach: When you get a raise or bonus, resist the urge to immediately upgrade your lifestyle. Instead, automatically direct a significant portion (e.g., 50-80%) of that extra income towards savings, investments, or debt repayment. Enjoy a small portion, but prioritize your financial goals.

3. Delaying Saving and Investing:

Why it’s problematic: The greatest advantage in wealth building is time, thanks to compound interest. Every year you delay starting, you lose out on exponential growth that can never be fully recovered. “I’ll start when I earn more” is a common trap.

Correct approach: Start now, even if it’s just a small amount. The power of compounding means that consistent, early contributions far outweigh larger, later contributions. Make savings and investing a non-negotiable part of your monthly financial plan.

4. Carrying High-Interest Debt:

Why it’s problematic: High-interest debt (especially credit card debt) acts as a severe drag on your finances. The interest payments consume money that could otherwise be used for savings or investments, keeping you in a cycle of debt.

Correct approach: Prioritize paying off high-interest debt aggressively. View it as an immediate investment with a guaranteed high return (the interest rate you avoid paying). Freeing yourself from this burden will unlock significant financial potential.

Troubleshooting

1. “I can’t stick to my budget!”

Quick Solution: Don’t view your budget as a rigid prison. It’s a living document. If you’re consistently overspending in one category, it might be unrealistic. Adjust it! Cut back in another area, or simply acknowledge that you’re spending more there and see if it aligns with your values. Also, try different budgeting methods (e.g., envelope system, zero-based budget) until you find one that clicks. Focus on progress, not perfection.

2. “Unexpected expenses keep derailing my progress!”

Quick Solution: This is precisely why an emergency fund is crucial! If you don’t have one, make building a starter fund ($1,000 or one month’s expenses) your absolute top priority. Once you have a safety net, these “unexpected” costs become less disruptive, allowing you to stay on track with your long-term goals. For predictable “unexpected” expenses (like car maintenance or holiday gifts), create sinking funds by saving a small amount each month.

3. “I feel overwhelmed by all this financial information.”

Quick Solution: You don’t have to tackle everything at once. Pick one step from this guide – maybe auditing your finances or setting up an automatic savings transfer – and focus on mastering it for a week or two. Small, consistent actions lead to big results. Break down large goals into tiny, manageable tasks. Remember, every financial expert started somewhere.

Key Takeaways

Redefine Winning: True financial freedom comes from smart habits, not lottery luck.

Know Your Numbers: Audit your income, expenses, assets, and liabilities to understand your financial reality.

Budget Smart: Create a personalized “wealth blueprint” (budget) to give every dollar a purpose.

Automate Savings: “Pay yourself first” by setting up automatic transfers to savings and investment accounts.

Crush Debt: Aggressively eliminate high-interest debt to free up funds for wealth building.

Invest Early & Consistently: Leverage compound interest by investing in low-cost index funds or ETFs.

Spend Mindfully: Make conscious purchasing decisions that align with your values and financial goals.

Learn & Adapt: Continuously educate yourself and adjust your financial plan as life changes.

Frequently Asked Questions

1. Is it too late to start saving and investing?

Absolutely not! While starting early offers the greatest advantage, the best time to start is always now. Every day you delay is a missed opportunity for your money to grow. Even small contributions today are better than nothing.

2. How much should I be saving each month?

A good general guideline is to aim for 20% of your after-tax income for savings and debt repayment, as per the 50/30/20 rule. However, if you’re just starting or have high-interest debt, prioritize getting a starter emergency fund and aggressively paying down debt first. Gradually increase your savings rate as you can.

3. What’s the “best” investment for beginners?

For most beginners, investing in low-cost, diversified index funds or ETFs that track the total stock market (like the S&P 500) is an excellent starting point. They offer broad market exposure, diversification, and historically strong returns without requiring you to pick individual stocks. Consider using tax-advantaged retirement accounts like a 401(k) or IRA first.

4. How can I stay motivated when progress feels slow?

Celebrate small wins! Paid off a credit card? Saved an extra $100 this month? Acknowledge your efforts. Regularly review your financial progress (e.g., quarterly) to see how far you’ve come. Remind yourself of your long-term financial goals and visualize the freedom they will bring. Connect with a supportive community or accountability partner if needed.

What’s Next?

Congratulations on taking the first steps to pick your real winning numbers! Your journey to financial freedom is a marathon, not a sprint, but every step you take brings you closer to the finish line.

Now that you have a solid foundation, consider diving deeper into specific areas:

Explore Advanced Investing: Learn about different asset classes, real estate investing, or even starting your own side hustle to boost income.

Retirement Planning: Research the nuances of different retirement accounts, Social Security, and how to plan for your golden years.

Estate Planning: Understand the importance of wills, trusts, and power of attorney to protect your assets and loved ones.

* Financial Coaching: If you feel stuck or need personalized guidance, consider working with a fee-only financial advisor.

Don’t wait for luck to change your life. Start picking your winning financial numbers today, and watch your wealth grow, securely and consistently. Your future self will thank you!