💳 12 Online Banking Billing Format

📚 The Financial Literacy Library

The best investment you can ever make is in your own financial education. These 5 cornerstone books are what millionaires, financial advisors, and wealth-builders universally recommend for completely rewiring how you think about earning, saving, and investing money.

🧠 The Psychology of Money

Doing well with money isn't necessarily about what you know—it's about how you behave. Morgan Housel masterfully breaks down the emotional and psychological biases that secretly dictate our financial decisions, offering a true paradigm shift in how to view wealth.

🏠 Rich Dad Poor Dad

The #1 personal finance book of all time for a reason. This foundational read shatters the myth that you need to earn a high income to be rich, teaching you the critical difference between working for money and making your money work for you via assets.

📈 Atomic Habits

While not strictly a finance book, building wealth is absolutely dependent on the daily habits you cultivate. James Clear provides the definitive framework for breaking bad spending habits and effortlessly automating the good ones that lead to long-term success.

📊 The Simple Path to Wealth

The ultimate antidote to complex, intimidating financial advice. JL Collins provides an incredibly accessible, low-stress roadmap to financial independence through index fund investing, perfectly explaining why simplicity beats Wall Street complexity every time.

💳 I Will Teach You to Be Rich

A tactical, no-BS, 6-week program that actually works. Ramit Sethi teaches you how to crush debt, automate your savings, and negotiate your salary—all while guilt-free spending on the things you truly love. A must-read for modern money management.

Hey, financial wizards and budget baddies! Ever stared at your online banking statement, trying to decipher what’s what? It’s like a secret code, right? But fear not, my digitally savvy friends. We’re diving deep into the glorious, sometimes bewildering, world of online banking billing formats. Let’s make sense of those numbers without needing a financial dictionary.

1. Transaction Dates

Oh, the timeline of your spending! This little detail tells you exactly when a transaction hit your account, not necessarily when you swiped your card. It’s crucial for tracking your daily financial flow.

Pro tip: always cross-reference these dates with your own records for accuracy. Catching discrepancies early can save you major headaches later.

Knowing the exact date helps you pinpoint spending habits and ensures you’re never guessing when that coffee addiction really started.

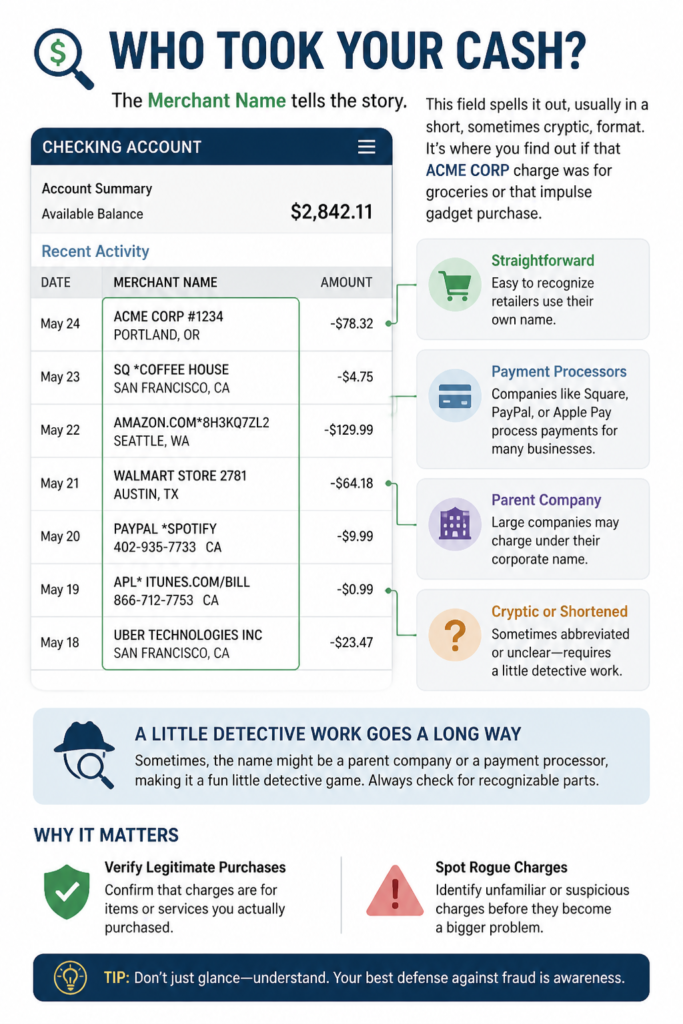

2. Merchant Names

Who took your cash? This field spells it out, usually in a short, sometimes cryptic, format. It’s where you find out if that “ACME CORP” charge was for groceries or that impulse gadget purchase.

Sometimes, the name might be a parent company or a payment processor, making it a fun little detective game. Always check for recognizable parts.

Understanding these names helps you verify legitimate purchases and spot any rogue charges trying to sneak past your radar.

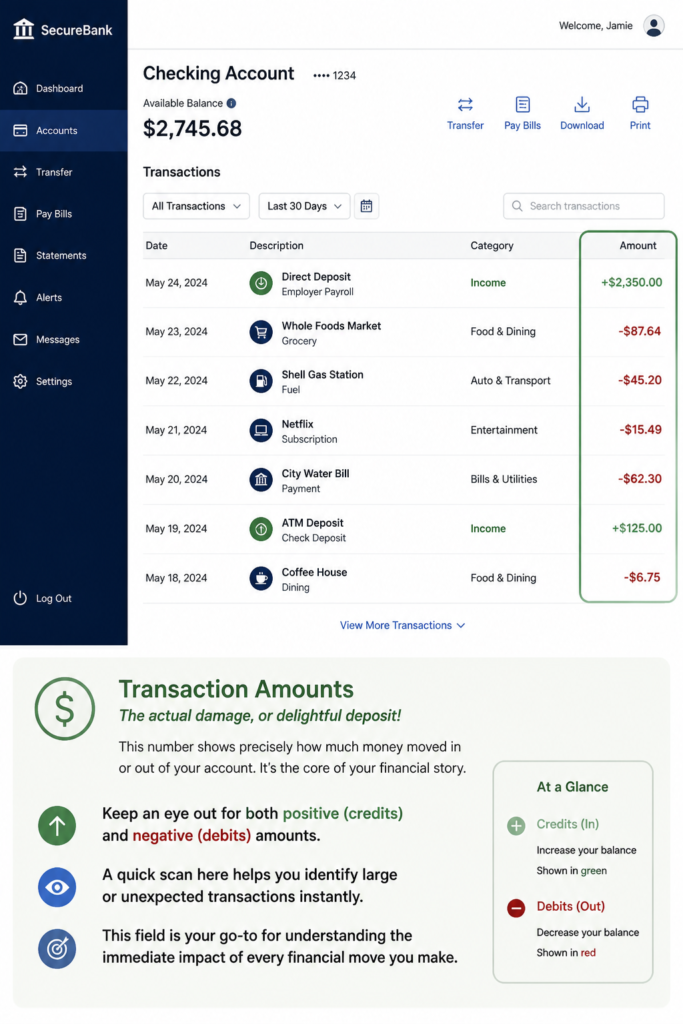

3. Transaction Amounts

The actual damage, or delightful deposit! This number shows precisely how much money moved in or out of your account. It’s the core of your financial story.

Keep an eye out for both positive (credits) and negative (debits) amounts. A quick scan here helps you identify large or unexpected transactions instantly.

This field is your go-to for understanding the immediate impact of every financial move you make.

4. Transaction Types

Debit, credit, transfer, ATM withdrawal – what kind of money magic just happened? This tells you the nature of each transaction. It clarifies the “how” behind the money movement.

Knowing the type helps you categorize your spending and track where your money is flowing. Is it a bill payment or a refund? This column holds the answer.

This detail is super helpful for budgeting, ensuring you know if you’re spending, saving, or just moving funds around.

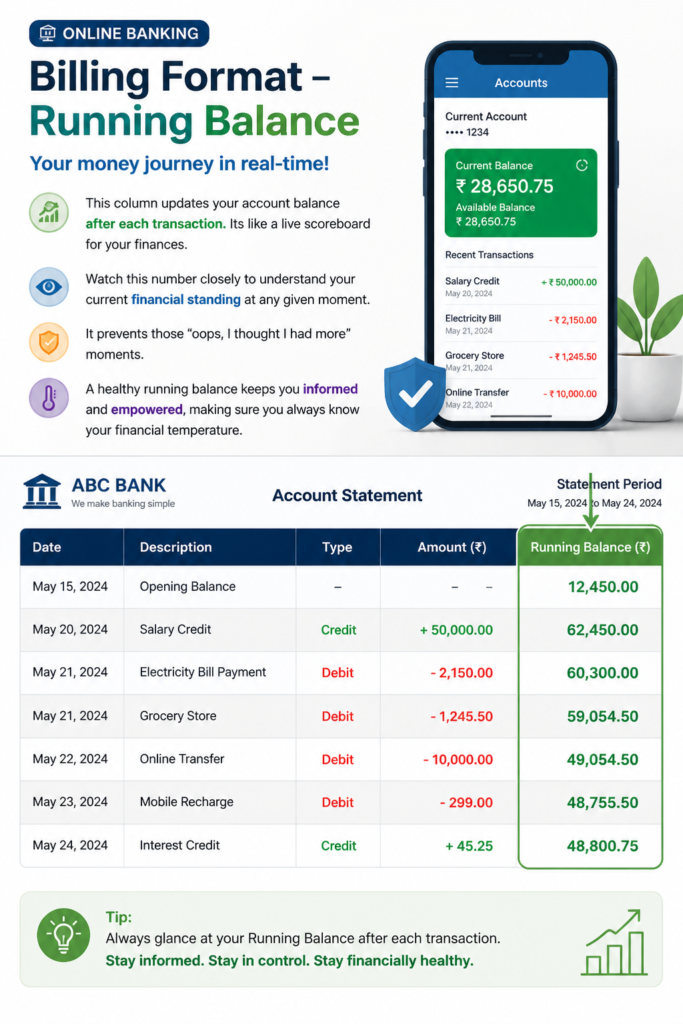

5. Running Balance

Your money journey in real-time! This column updates your account balance after each transaction. It’s like a live scoreboard for your finances.

Watch this number closely to understand your current financial standing at any given moment. It prevents those “oops, I thought I had more” moments.

A healthy running balance keeps you informed and empowered, making sure you always know your financial temperature.

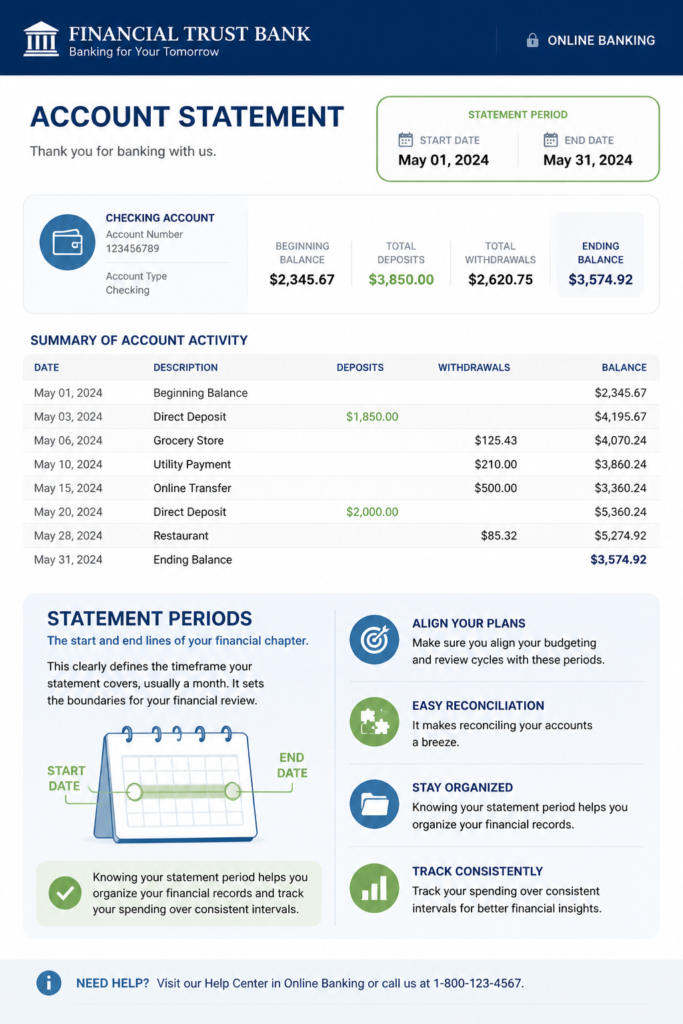

6. Statement Periods

The start and end lines of your financial chapter. This clearly defines the timeframe your statement covers, usually a month. It sets the boundaries for your financial review.

Make sure you align your budgeting and review cycles with these periods. It makes reconciling your accounts a breeze.

Knowing your statement period helps you organize your financial records and track your spending over consistent intervals.

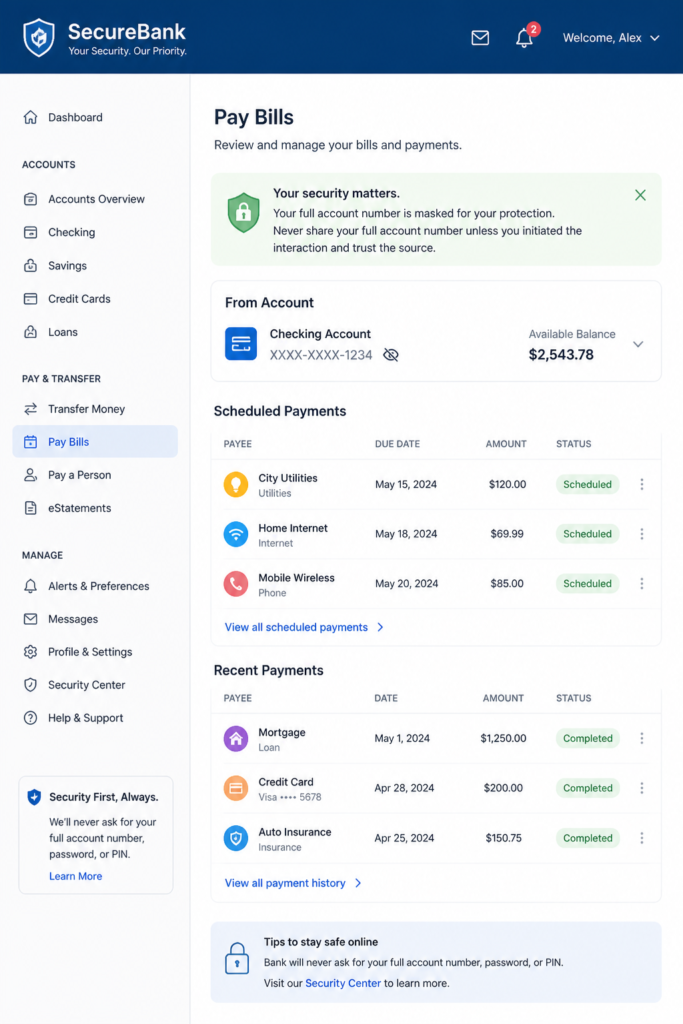

7. Account Numbers (Masked)

Security first, always! Your full account number usually appears masked (think `XXXX-XXXX-1234`) for obvious safety reasons. It confirms which account you’re actually looking at.

Never share your full account number unless you absolutely trust the source and initiated the interaction. Your bank will almost never ask for it.

This masked display offers peace of mind, letting you confirm your account without exposing sensitive data.

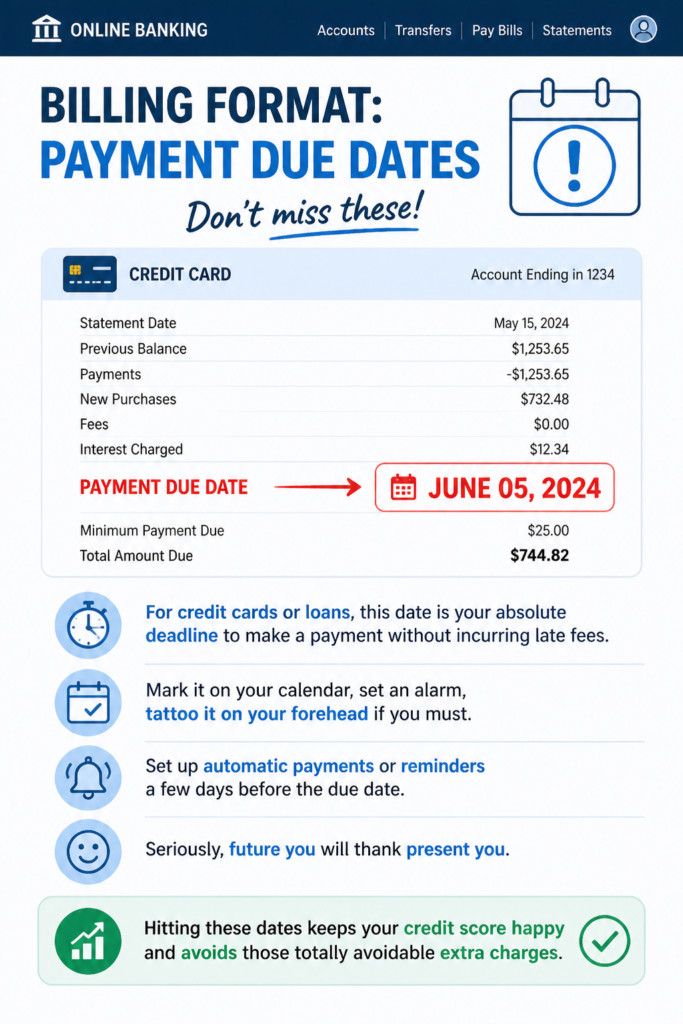

8. Payment Due Dates

Don’t miss these! For credit cards or loans, this date is your absolute deadline to make a payment without incurring late fees. Mark it on your calendar, set an alarm, tattoo it on your forehead if you must.

Set up automatic payments or reminders a few days before the due date. Seriously, future you will thank present you.

Hitting these dates keeps your credit score happy and avoids those totally avoidable extra charges.

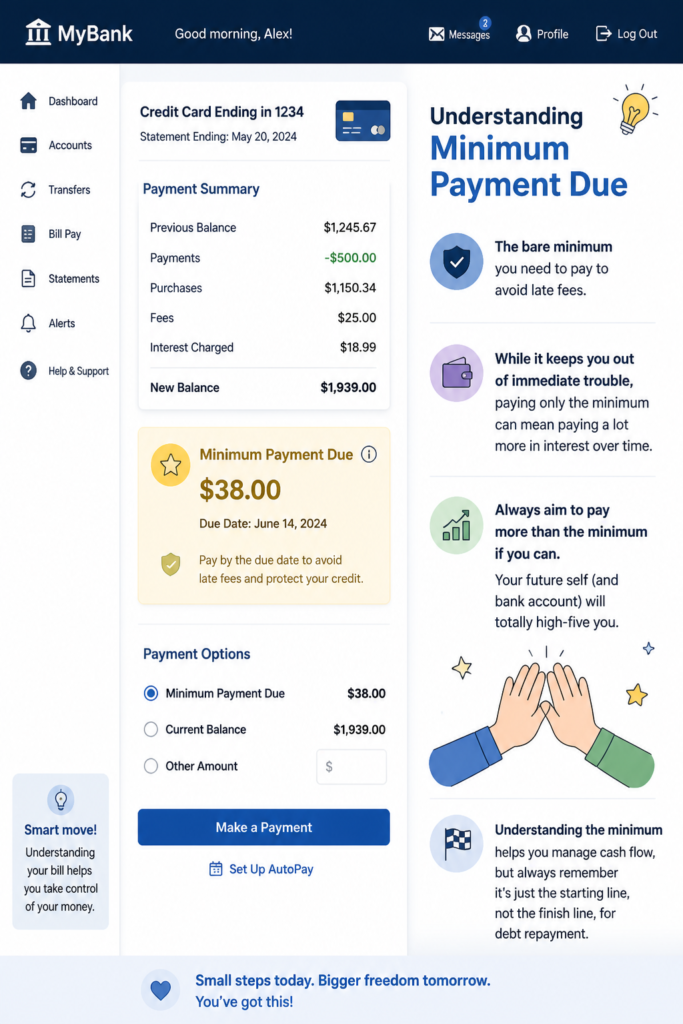

9. Minimum Payment Due

The bare minimum you need to pay to avoid late fees. While it keeps you out of immediate trouble, paying only the minimum can mean paying a lot more in interest over time.

Always aim to pay more than the minimum if you can. Your future self (and bank account) will totally high-five you.

Understanding the minimum helps you manage cash flow, but always remember it’s just the starting line, not the finish line, for debt repayment.

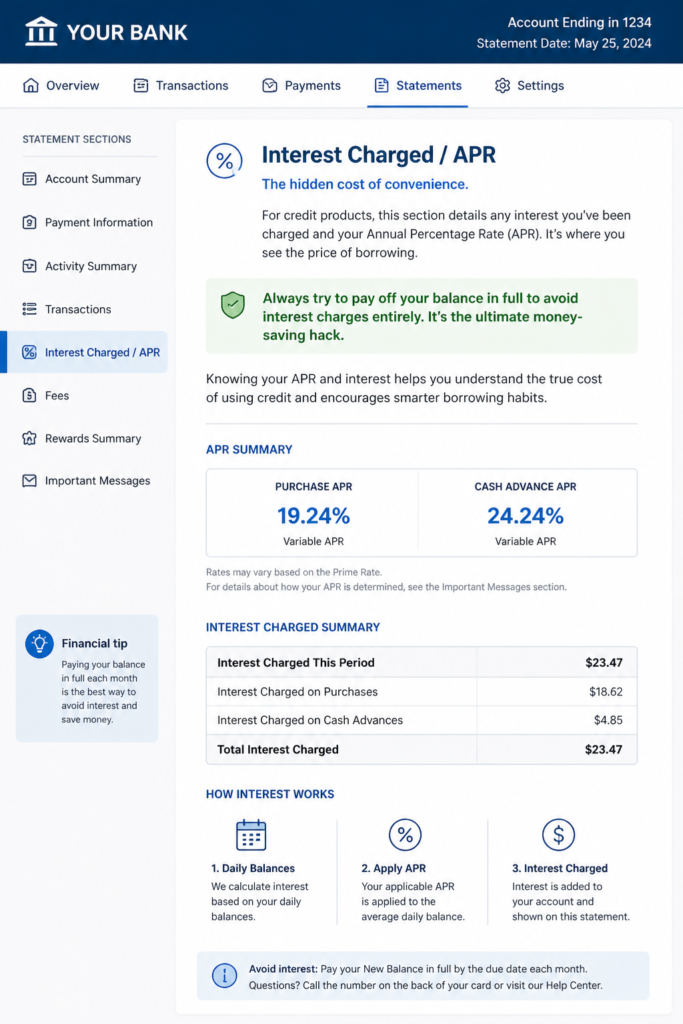

10. Interest Charged/APR

The hidden cost of convenience. For credit products, this section details any interest you’ve been charged and your Annual Percentage Rate (APR). It’s where you see the price of borrowing.

Always try to pay off your balance in full to avoid interest charges entirely. It’s the ultimate money-saving hack.

Knowing your APR and interest helps you understand the true cost of using credit and encourages smarter borrowing habits.

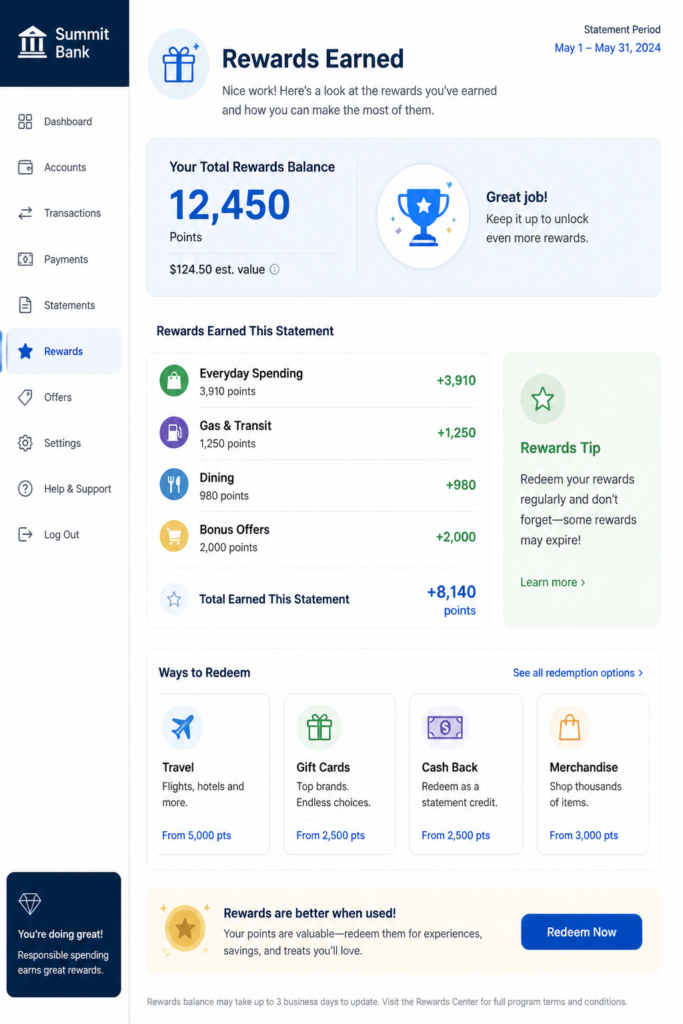

11. Rewards Earned

The good stuff! If your card offers points, cashback, or miles, this section proudly displays your latest haul. It’s like finding money you didn’t know you had.

Keep an eye on your rewards balance and redemption options. Don’t let those valuable perks expire or go unused.

This little bonus reminds you that responsible spending can actually have some pretty sweet payoffs.

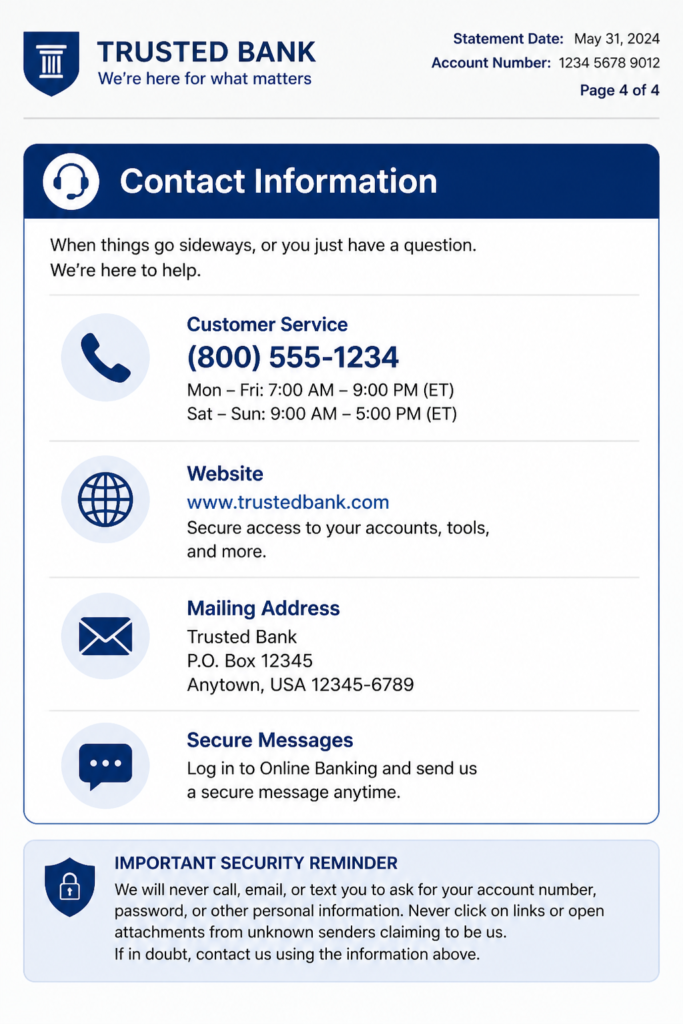

12. Contact Information

When things go sideways, or you just have a question. This section provides the bank’s customer service number, website, and sometimes even a mailing address. It’s your lifeline.

Always save your bank’s contact info somewhere easily accessible, but never trust unsolicited calls or emails claiming to be your bank.

Having this handy ensures you can quickly get help or clarify any statement mysteries without a frantic Google search.

💼 The Money Management Toolkit

Knowledge is power, but proper execution requires the right tools. Getting your financial life organized doesn't have to be overwhelming. These 5 physical management tools are exactly what successful households use to budget, track cash, and secure their most important assets.

📝 Clever Fox Budget Planner & Bill Organizer

The ultimate analog command center for your finances. Sometimes keeping your budget in an app just doesn't stick. Physically writing down your goals, tracking expenses, and planning for debt payoff creates a level of accountability that digital spreadsheets simply can't match.

💵 A6 Leather Cash Stuffing Binder

The viral tool that made the cash-envelope budgeting system popular again. By allocating actual physical cash to designated envelopes (groceries, dining out, fun money), you physically cap your spending, making it virtually impossible to overdraft or overspend.

🔥 Fireproof & Waterproof Document Safe

A critical piece of financial security that many families overlook. Protecting your passports, birth certificates, property deeds, and estate planning documents from disaster is just as important as protecting the money in your bank account.

🏷️ Brother P-Touch Digital Label Maker

The unsung hero of a functional home office. When tax season rolls around or you need to find an important receipt, having perfectly labeled and categorized filing cabinets or accordion folders saves hours of frustrating searches and potential late fees.

🔒 SentrySafe Compact Fireproof Lock Box

For the physical assets that need extra heavy-duty protection—think emergency cash reserves, hard drives with Bitcoin cold wallets, or physical precious metals. This compact, locking safe provides peace of mind that your physical wealth is secure at home.

Conclusion

So there you have it, folks! Demystifying your online banking billing format isn’t just for financial whizzes; it’s for anyone who wants to feel totally in control of their cash. No more squinting at screens or wondering what that obscure code means. You’ve got the lowdown now, ready to tackle your statements like a pro. Go forth and conquer your finances with confidence, knowing exactly where every penny is (or isn’t) going. Your wallet will thank you.