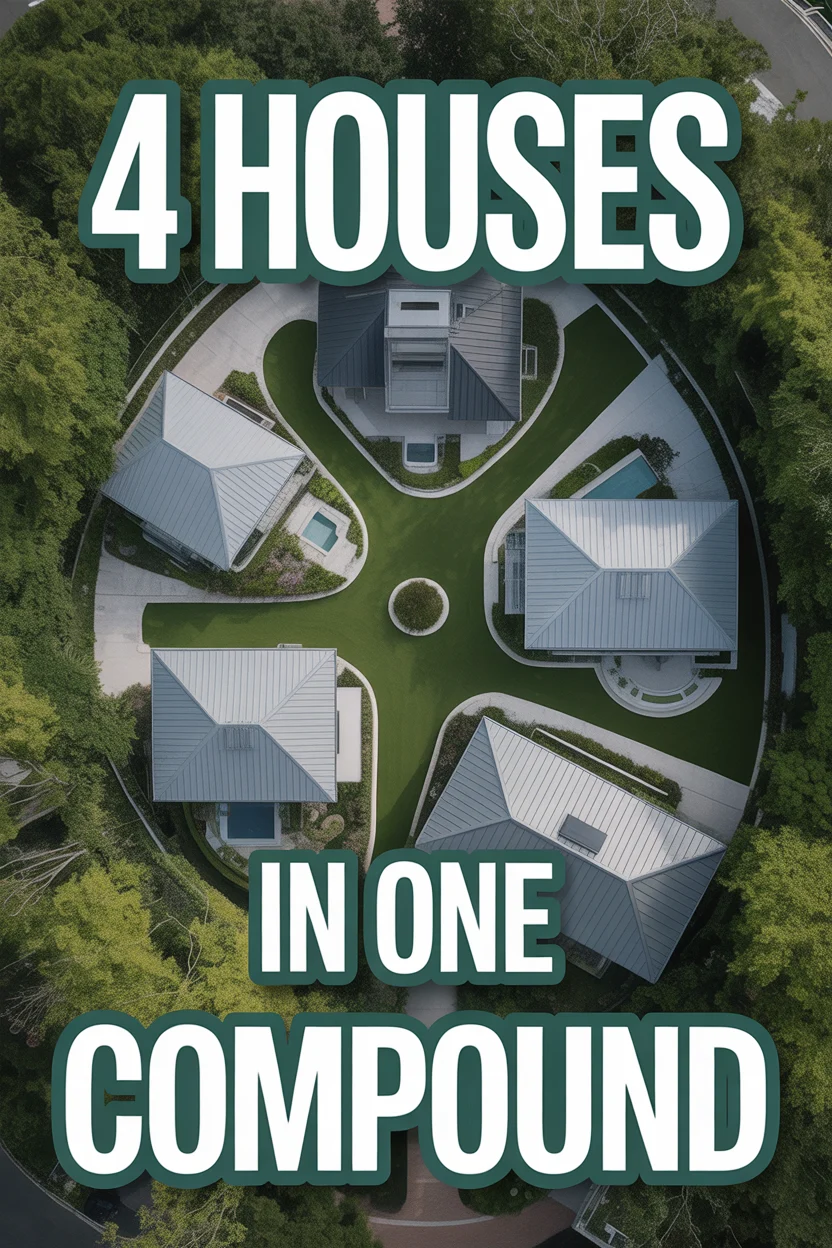

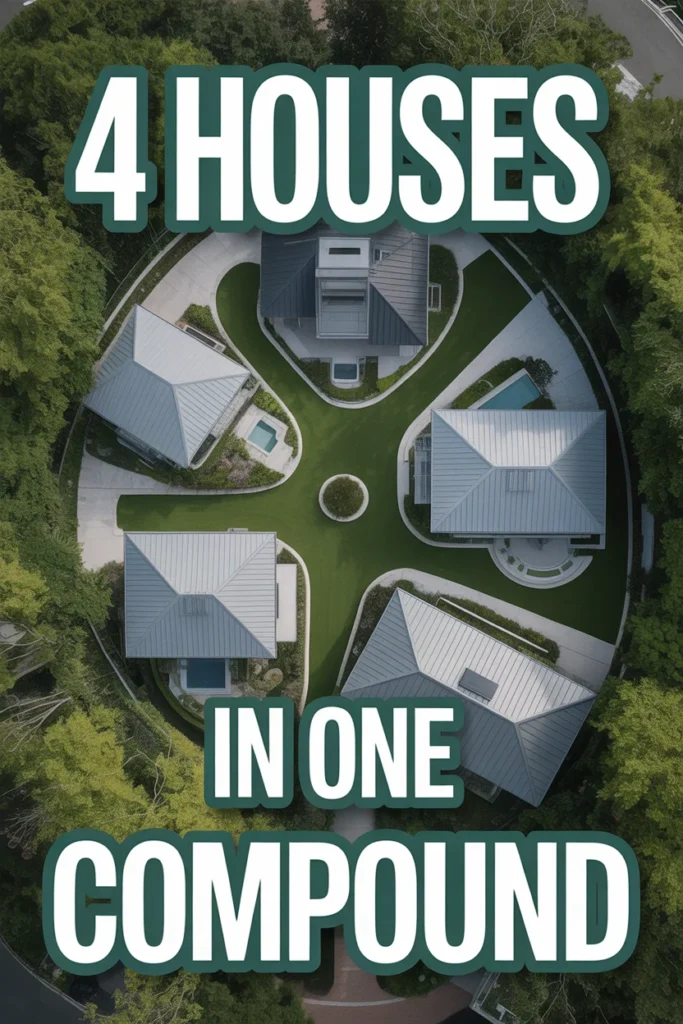

🏡 4 Houses In One Compound

📚 The Financial Literacy Library

The best investment you can ever make is in your own financial education. These 5 cornerstone books are what millionaires, financial advisors, and wealth-builders universally recommend for completely rewiring how you think about earning, saving, and investing money.

🧠 The Psychology of Money

Doing well with money isn't necessarily about what you know—it's about how you behave. Morgan Housel masterfully breaks down the emotional and psychological biases that secretly dictate our financial decisions, offering a true paradigm shift in how to view wealth.

🏠 Rich Dad Poor Dad

The #1 personal finance book of all time for a reason. This foundational read shatters the myth that you need to earn a high income to be rich, teaching you the critical difference between working for money and making your money work for you via assets.

📈 Atomic Habits

While not strictly a finance book, building wealth is absolutely dependent on the daily habits you cultivate. James Clear provides the definitive framework for breaking bad spending habits and effortlessly automating the good ones that lead to long-term success.

📊 The Simple Path to Wealth

The ultimate antidote to complex, intimidating financial advice. JL Collins provides an incredibly accessible, low-stress roadmap to financial independence through index fund investing, perfectly explaining why simplicity beats Wall Street complexity every time.

💳 I Will Teach You to Be Rich

A tactical, no-BS, 6-week program that actually works. Ramit Sethi teaches you how to crush debt, automate your savings, and negotiate your salary—all while guilt-free spending on the things you truly love. A must-read for modern money management.

Imagine a life where your home isn’t just a place to live, but a powerful engine for financial freedom, a hub for family connection, and a cornerstone of your wealth-building journey. This isn’t a far-fetched dream; it’s the tangible reality offered by an increasingly popular and savvy strategy known as “4 Houses In One Compound.” In a world where housing costs continue to climb and the desire for both community and financial independence grows, this innovative approach stands out as a brilliant solution. It’s about maximizing your land, leveraging your assets, and cultivating a lifestyle that supports both your wallet and your well-being.

This comprehensive guide will demystify the concept of 4 Houses In One Compound, breaking down its incredible potential for saving money, generating income, and building lasting wealth. We’ll explore practical tips, smart budgeting hacks, and a wealth-building mindset that will empower you to navigate this exciting path. Whether you’re a multi-generational family seeking closer ties, an investor looking for a high-yield asset, or simply someone yearning for a more financially secure and communal way of living, the 4 Houses In One Compound model offers a blueprint for success. Get ready to unlock the secrets to turning your property into a powerhouse of prosperity and connection.

What is 4 Houses In One Compound?

At its core, “4 Houses In One Compound” refers to a property setup where four distinct residential units coexist on a single plot of land or within a contiguous, unified parcel. Think of it not just as a single large home, but as a mini-village designed for efficiency, community, and financial leverage. This concept can manifest in several ways, each with its own advantages:

- Multi-Unit Dwellings: This might be a single building divided into four separate apartments or townhouses, each with its own entrance, kitchen, and living space. While sharing common walls, each unit maintains its independence.

- Main House with Accessory Dwelling Units (ADUs): A common configuration involves a larger primary residence alongside three smaller, detached or attached ADUs (often called granny flats, in-law suites, or backyard cottages). This allows for greater privacy between units while still benefiting from shared land.

- Four Standalone Homes: In some cases, especially on larger plots, the compound could consist of four entirely separate, smaller homes, each with its own footprint but sharing a common driveway, yard, or infrastructure.

The defining characteristic is the “compound” aspect – a shared property boundary that allows for collective management, shared resources, and a sense of community, while each unit functions as an independent home. This arrangement is particularly attractive for several reasons:

- Intergenerational Living: Families can live close to one another, providing mutual support for childcare, elder care, and daily life, all while maintaining individual privacy and autonomy.

- Intentional Communities: Groups of friends or like-minded individuals can pool resources to create a shared living environment that fosters connection and collaboration.

- Investment & Income Generation: For savvy investors, it’s a powerful strategy to maximize rental income from a single property, diversifying risk and potentially generating substantial cash flow.

- Financial Freedom: By offsetting mortgage costs with rental income or shared expenses, residents can significantly reduce their housing burden, accelerating their path to financial independence.

Understanding these variations is key to tailoring the 4 Houses In One Compound model to your specific needs and financial goals. It’s a versatile blueprint for smart living and wealth creation.

Key Features

The appeal of the 4 Houses In One Compound model lies in its multifaceted benefits, touching upon financial leverage, community building, and long-term wealth accumulation. Here are the standout features that make this strategy a game-changer:

- Unparalleled Financial Leverage & Income Generation:

This is where the money-smart aspect truly shines. Instead of one mortgage for one home, you’re leveraging a single property investment to potentially generate income from three additional units. Imagine living in one unit and having the rent from the other three largely or completely cover your mortgage, property taxes, and insurance. This dramatically reduces your personal housing expenses, freeing up significant capital for savings, investments, or debt repayment. For investors, it’s a dream scenario: multiple income streams from one asset, diversifying vacancy risk and often yielding a higher return on investment than a single-family home.

- Significant Cost Savings & Resource Sharing:

Beyond rental income, the compound model offers inherent cost efficiencies. Shared utility connections (water, sewer, electricity, internet) can lead to economies of scale, even if sub-metered. Maintenance costs for common areas like roofs, driveways, and landscaping can be split among residents, drastically reducing individual burdens. Think about bulk purchasing for household necessities, shared tools, or even a communal garden that lowers grocery bills. This collective approach to expenses means more money stays in your pocket.

- Enhanced Intergenerational & Community Living:

For families, this model is a revelation. Grandparents can live independently yet be just steps away from their grandchildren, offering invaluable support for childcare, while adult children can assist with elder care. The compound fosters a built-in support system, enhanced security through mutual oversight, and a vibrant social fabric. It’s the perfect balance of proximity and privacy, allowing family bonds to flourish without the challenges of living under one roof.

- Accelerated Wealth Building & Asset Appreciation:

A property with multiple income-generating units typically commands a higher market value than a comparable single-family home. As real estate appreciates, your compound’s value will grow at an accelerated rate due to its increased income potential. This creates a powerful asset that builds equity faster, acts as an inflation hedge, and provides a significant legacy for future generations. When it comes time to sell, you’re not just selling a home; you’re selling an investment property with established cash flow.

- Flexibility & Adaptability for Life Stages:

Life changes, and your housing should be able to adapt. The 4 Houses In One Compound offers incredible flexibility. As children grow up, they might move into one of the smaller units. When they eventually move out, that unit can be rented for additional income. If an elderly parent needs care, they can move into a nearby unit, ensuring comfort and accessibility. This adaptability means your property can evolve with your family’s needs, providing housing solutions for decades.

These features collectively paint a picture of a smart, sustainable, and financially empowering way to live and invest in real estate. It’s about building more than just a home; it’s about building a future.

How to Get Started

Embarking on the journey of creating a 4 Houses In One Compound requires careful planning and strategic execution. Here’s a step-by-step guide to help you get started on this rewarding path:

- Step 1: Define Your Vision & Conduct Thorough Research

Before anything else, clarify your “why.” Are you aiming for financial independence, multi-generational living, or primarily an investment vehicle? Who will be involved – family, friends, or tenants? This vision will guide your decisions. Next, and critically, research local zoning laws and building codes. This is paramount. Look for areas zoned for multi-family dwellings, ADUs, or properties that allow for significant expansion. Many municipalities are easing restrictions on ADUs, but rules vary widely. Consult with local planning departments and experienced real estate agents who understand multi-unit properties in your target area.

- Step 2: Financial Planning & Securing Funding

Create a detailed budget that accounts for property acquisition, design, construction/renovation, permits, and a contingency fund (always allocate 15-20% extra for unexpected costs). Explore various funding options:

- Conventional Multi-Unit Mortgages: Many lenders offer specific products for properties with 2-4 units.

- Construction Loans: If you’re building from scratch or undertaking major renovations.

- FHA Loans: Can be used for multi-unit properties (up to 4 units) if you plan to live in one.

- Private Lenders/Investors: For unique situations or faster funding.

Ensure you understand the debt-to-income ratios and credit score requirements for these types of loans. Get pre-approved to know your borrowing capacity. - Step 3: Location, Property Acquisition & Due Diligence

With your vision and finances in order, begin your property search. Look for land or existing properties that are large enough to accommodate four units (either by building new or converting/expanding). Consider locations with strong rental demand if income is a priority, and good amenities for residents. Once you find a potential property, conduct rigorous due diligence:

- Professional Inspections: Structural, electrical, plumbing, roof, HVAC.

- Appraisal: To ensure the property’s value supports your investment.

- Title Search: To uncover any liens or encumbrances.

- Environmental Reports: Especially for undeveloped land.

A real estate attorney specializing in multi-unit properties can be invaluable during this phase. - Step 4: Design, Permitting & Construction/Renovation

This is where your vision takes physical form. Engage an architect or designer experienced in multi-unit projects. Focus on creating functional, private spaces for each unit while optimizing shared areas. Key design considerations include:

- Separate Entrances: Essential for privacy and rental appeal.

- Soundproofing: To minimize noise transfer between units.

- Energy Efficiency: Investing in insulation, efficient windows, and appliances will save money long-term.

- Accessibility: Consider universal design principles for future flexibility.

The permitting process can be lengthy and complex, so be patient and work closely with your architect and local authorities. Hire reputable contractors with experience in similar projects. - Step 5: Legal & Management Structures

Before occupancy, establish clear legal and financial frameworks:

- Co-Ownership Agreements: If co-owning with family or friends, draft a detailed agreement covering responsibilities, cost-sharing, decision-making, and exit strategies (e.g., if someone wants to sell their share).

- Lease Agreements: For rental units, use legally sound leases that protect both landlord and tenant.

- Utility Management: Decide on separate meters for each unit (ideal) or a clear system for prorating shared utility bills.

- Insurance: Obtain comprehensive landlord insurance in addition to standard property insurance. Consider an umbrella policy for added liability protection.

Consult a legal professional to ensure all agreements are robust and legally binding.

By meticulously following these steps, you lay a solid foundation for a successful and financially rewarding 4 Houses In One Compound.

Tips for Success

Navigating the journey of 4 Houses In One Compound can be incredibly rewarding, but like any significant undertaking, success hinges on smart strategies and a proactive mindset. Here are 5 pro tips to help you thrive:

- 1. Master Your Budget & Track Everything Meticulously:

This is the bedrock of financial success for your compound. Create a detailed budget that includes all income (rent, shared contributions) and expenses (mortgage, taxes, insurance, utilities, maintenance, vacancy fund). Use budgeting apps (like You Need A Budget, Mint, or even a robust spreadsheet) to track every dollar in and out. Set up separate bank accounts for compound finances to keep personal and property funds distinct. Automate savings and bill payments whenever possible. Regularly review your budget (monthly, quarterly) to identify areas for optimization, adjust for unexpected costs, and ensure you’re on track to meet your financial goals. Knowing your numbers empowers you to make informed decisions and pivot when necessary.

- 2. Communication is Paramount (Especially for Co-Living/Co-Owning):

If you’re sharing the compound with family or friends, clear and consistent communication is the single most important factor for harmony and financial stability. Hold regular “compound meetings” to discuss finances, maintenance, shared responsibilities, and any potential issues. Establish clear expectations from the outset, ideally in a written agreement, covering everything from chore delegation to conflict resolution. Don’t let small annoyances fester; address concerns respectfully and promptly. Proactive communication prevents misunderstandings, builds trust, and ensures everyone is aligned with the compound’s goals.

- 3. Build a Robust Emergency Fund & Diversify Investments:

Real estate, while a powerful wealth builder, can have unexpected costs (major repairs, tenant vacancies). Aim to build an emergency fund specifically for the compound, ideally covering 6-12 months of operating expenses (including mortgage payments if you rely on rental income). This financial cushion prevents stress and protects your investment during lean times. Furthermore, while your compound is a significant asset, don’t put all your eggs in one basket. Diversify your wealth-building efforts by investing in other vehicles like stocks, bonds, mutual funds, or retirement accounts (401k, IRA). A diversified portfolio creates multiple streams of wealth and hedges against market fluctuations.

- 4. Prioritize Proactive Maintenance & Strategic Value Addition:

Neglecting maintenance is a common and costly mistake. Implement a proactive maintenance schedule for all units and common areas (HVAC servicing, roof inspections, landscaping, pest control). Addressing small issues before they become major problems saves significant money in the long run and keeps your tenants happy. Beyond maintenance, look for opportunities for strategic value addition. Energy-efficient upgrades (solar panels, smart thermostats), modernizing kitchens/bathrooms, or enhancing curb appeal can increase rental income, attract higher-quality tenants, and boost the overall property value, accelerating your wealth accumulation.

- 5. Leverage Smart Debt & Understand Its Power:

Not all debt is bad. A mortgage on an income-generating property like your 4 Houses In One Compound is often considered “good debt” because it allows you to acquire an appreciating asset that produces income. Learn about mortgage refinancing options (e.g., cash-out refi for improvements, rate-and-term refi for lower interest rates) to optimize your financial position. Understand how interest rates impact your cash flow and equity. Always aim for a healthy debt-to-income ratio, but don’t shy away from strategically using borrowed capital to grow your real estate portfolio and accelerate your journey to financial independence.

By implementing these tips, you’ll not only create a thriving living environment but also build a resilient and powerful financial engine that supports your long-term wealth goals.

Common Mistakes to Avoid

While the 4 Houses In One Compound strategy offers immense potential, certain pitfalls can derail your progress. Being aware of these common mistakes can help you navigate challenges and ensure a smoother, more profitable journey:

- 1. Ignoring Zoning Laws and Local Regulations:

This is perhaps the biggest and most costly mistake. Assuming you can simply build or convert units without proper permits and adherence to local zoning laws (which dictate property use, density, setbacks, and ADU rules) can lead to fines, forced demolition, legal battles, and significant financial losses. Always start with thorough research of your local municipality’s rules and consult with planning departments and experienced professionals before purchasing or beginning any work.

- 2. Underestimating Costs and Neglecting a Contingency Fund:

The excitement of a new project can sometimes overshadow the practicalities of budgeting. Construction, renovation, and even ongoing maintenance almost always cost more than initially estimated. Failing to account for unexpected expenses (material price increases, unforeseen structural issues, permit delays) can lead to project stalls, increased debt, or even abandonment. Always budget for a contingency fund of at least 15-20% of your total project cost, and remember that ongoing maintenance, vacancy periods, and property taxes are continuous expenses.

- 3. Poor Communication and Unclear Agreements (Especially for Co-Owners):

When multiple parties (family members, friends) are involved in owning or living in the compound, a lack of clear, written agreements can be catastrophic. Ambiguity regarding financial contributions, shared responsibilities, decision-making processes, conflict resolution, and exit strategies can lead to resentment, disputes, and even legal action. Invest time and resources in drafting comprehensive co-ownership agreements with legal counsel that cover every foreseeable scenario.

- 4. Neglecting a Dedicated Emergency Fund for the Property:

Even with careful planning, things go wrong. A sudden major repair (burst pipe, roof damage), an extended tenant vacancy, or an unexpected legal fee can quickly deplete your personal savings if you don’t have a separate fund for the property. Build a dedicated emergency fund specifically for the compound that can cover several months of operating expenses. This acts as a crucial buffer against unforeseen financial shocks.

- 5. Failing to Properly Screen Tenants:

If you plan to rent out units, cutting corners on tenant screening is a recipe for disaster. Bad tenants can cause property damage, neglect rent payments, create disturbances, and lead to costly eviction processes. Implement a rigorous screening process that includes credit checks, background checks, employment verification, and reference checks. Good tenants are worth the effort and contribute significantly to the compound’s financial stability and peace of mind.

- 6. Over-Personalizing Investment Decisions:

While the compound might be your home or a family venture, it’s also a significant financial asset. Making decisions based solely on emotion, rather than sound financial principles, can be detrimental. For example, charging below-market rent to a family member, delaying necessary repairs, or shying away from difficult conversations about money can undermine the compound’s profitability and long-term viability. Treat the compound as a business operation, even if it’s family-centric, and make financially prudent decisions.

By actively avoiding these common pitfalls, you significantly increase your chances of building a successful, sustainable, and wealth-generating 4 Houses In One Compound.

FAQ

Here are some frequently asked questions about the “4 Houses In One Compound” strategy, offering quick, actionable answers to common concerns:

- Q1: Is “4 Houses In One Compound” legal everywhere?

A: No, it is not universally legal. The legality of building or converting a property into four separate units on one compound depends entirely on local zoning laws, building codes, and municipal regulations. Some areas are very restrictive, while others are becoming more open to multi-unit dwellings and Accessory Dwelling Units (ADUs). It is absolutely critical to research your specific city and county ordinances before making any commitments. Start by contacting your local planning department.

- Q2: How do we handle shared expenses fairly among residents?

A: Fairly distributing shared expenses requires a clear, agreed-upon system. Common methods include:

- Proportional by Unit Size: Each unit contributes based on its square footage.

- Proportional by Occupants: Contribution based on the number of people living in each unit.

- Equal Split: All four units contribute an equal share, often for common area maintenance or shared utilities without sub-meters.

- Usage-Based: For utilities like electricity or water, installing sub-meters for each unit is the fairest approach, allowing each household to pay for its exact consumption.

The most important aspect is a written agreement detailing the method, review frequency, and payment schedule, signed by all parties. - Q3: What are the tax implications of owning a 4 Houses In One Compound?

A: The tax implications can be complex and vary based on whether you live in one unit, rent all four, or a combination. Key tax considerations include:

- Property Taxes: Assessed based on the property’s total value, potentially higher for multi-unit properties.

- Rental Income Tax: Any income generated from rented units is taxable. You’ll report this on your income tax return.

- Deductible Expenses: Many property-related expenses (mortgage interest, property taxes, insurance, maintenance, depreciation) can be deducted against rental income, reducing your taxable income.

- Capital Gains Tax: When you sell the property, any profit (capital gain) may be subject to tax, though there are exemptions if it was your primary residence.

It is highly recommended to consult with a qualified tax professional who specializes in real estate and rental properties to understand your specific obligations and optimize your tax strategy. - Q4: How do we get a mortgage for this type of property?

A: Mortgages for 4 Houses In One Compound typically fall under multi-unit residential loans. Lenders categorize properties based on the number of units:

- 1-4 Units: These are often considered residential properties, and you may qualify for conventional Fannie Mae or Freddie Mac loans, FHA loans, or VA loans (if eligible), especially if you intend to live in one of the units (owner-occupied).

- 5+ Units: These are generally considered commercial properties and require commercial mortgages, which have different terms, interest rates, and approval processes.

Lenders will assess the property’s income potential (from rental units) in addition to your personal income and creditworthiness. Shop around with multiple lenders and look for those experienced in financing multi-unit properties. Being pre-approved early in the process is crucial.

💼 The Money Management Toolkit

Knowledge is power, but proper execution requires the right tools. Getting your financial life organized doesn't have to be overwhelming. These 5 physical management tools are exactly what successful households use to budget, track cash, and secure their most important assets.

📝 Clever Fox Budget Planner & Bill Organizer

The ultimate analog command center for your finances. Sometimes keeping your budget in an app just doesn't stick. Physically writing down your goals, tracking expenses, and planning for debt payoff creates a level of accountability that digital spreadsheets simply can't match.

💵 A6 Leather Cash Stuffing Binder

The viral tool that made the cash-envelope budgeting system popular again. By allocating actual physical cash to designated envelopes (groceries, dining out, fun money), you physically cap your spending, making it virtually impossible to overdraft or overspend.

🔥 Fireproof & Waterproof Document Safe

A critical piece of financial security that many families overlook. Protecting your passports, birth certificates, property deeds, and estate planning documents from disaster is just as important as protecting the money in your bank account.

🏷️ Brother P-Touch Digital Label Maker

The unsung hero of a functional home office. When tax season rolls around or you need to find an important receipt, having perfectly labeled and categorized filing cabinets or accordion folders saves hours of frustrating searches and potential late fees.

🔒 SentrySafe Compact Fireproof Lock Box

For the physical assets that need extra heavy-duty protection—think emergency cash reserves, hard drives with Bitcoin cold wallets, or physical precious metals. This compact, locking safe provides peace of mind that your physical wealth is secure at home.

Conclusion

The concept of “4 Houses In One Compound” is far more than just a housing arrangement; it’s a strategic blueprint for achieving profound financial freedom, fostering deep community bonds, and building a robust legacy of wealth. In an era where traditional homeownership often feels out of reach or financially burdensome, this innovative model offers a powerful alternative – one that transforms your property into an active asset rather than just a passive expense.

We’ve explored how this approach can unlock unparalleled financial leverage, significantly reduce your living costs through shared resources, and accelerate your journey to financial independence. Beyond the numbers, it provides a unique opportunity for intergenerational living, creating a supportive environment where family can thrive while maintaining individual privacy. It’s a testament to smart land use and a forward-thinking mindset that combines the best of personal space with the benefits of collective living.

However, the path to a successful 4 Houses In One Compound is paved with diligent planning, open communication, and astute financial management. From navigating complex zoning laws and securing the right financing to meticulous budgeting and proactive maintenance, each step requires careful consideration. But as the “Tips for Success” and “Common Mistakes to Avoid” sections highlight, with the right strategies and a commitment to learning, these challenges are entirely surmountable.

If the vision of living a more financially secure, connected, and purpose-driven life resonates with you, then the 4 Houses In One Compound model deserves your serious consideration. It’s a tangible, actionable strategy that empowers you to take control of your housing costs, generate substantial income, and build lasting wealth for yourself and future generations. Don’t just dream of financial freedom; start building it. Begin your research today, connect with professionals, and take the first exciting steps toward transforming your property into a powerhouse of prosperity and community.