💰 How To Budget For Beginners Biweekly

Feeling like your money disappears faster than a free sample at a grocery store? You’re not alone. Many people feel overwhelmed by their finances, living paycheck to paycheck with little to show for it. But imagine a world where you know exactly where every dollar goes, where saving for your dreams feels achievable, and where financial stress is a distant memory. This guide is your friendly map to that world, specifically tailored for those paid biweekly, transforming confusion into clarity and turning financial anxiety into empowered action.

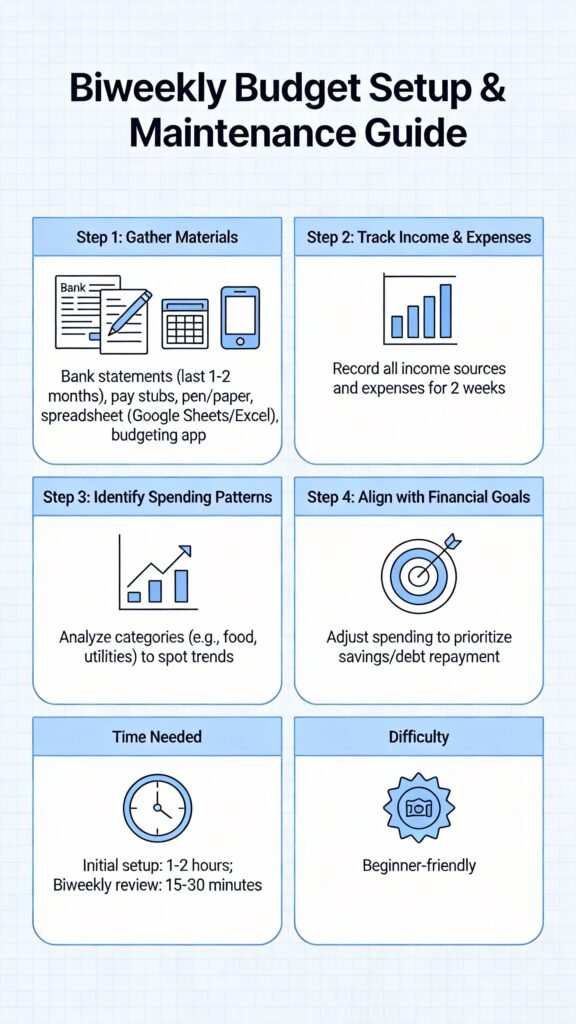

Quick Overview

This guide will walk you through the process of setting up and maintaining a biweekly budget that puts you in control of your money, helps you save, and sets you on the path to financial freedom. You’ll learn how to track income and expenses, identify spending patterns, and make conscious choices that align with your financial goals.

Time needed: Initial setup: 1-2 hours. Biweekly review: 15-30 minutes.

Difficulty: Beginner

What you’ll need: Your bank statements (last 1-2 months), pay stubs, a pen and paper, a spreadsheet (like Google Sheets or Excel), or a budgeting app.

Step-by-Step Instructions

Step 1: Gather Your Financial Data

Before you can budget, you need to know what you’re working with. This means collecting all the relevant numbers related to your money coming in and going out. Think of yourself as a financial detective, gathering clues to solve the mystery of your money.

Start by collecting your bank statements, credit card statements, and pay stubs for the last one to two months. This historical data will give you a realistic picture of your income and spending habits. Don’t worry about judgment; this is purely for information gathering.

Pro tip: If you use online banking, most banks allow you to download statements as PDFs or CSV files, which can make data entry easier later on.

Step 2: Understand Your Biweekly Income

Your income is the foundation of your budget. Since you’re paid biweekly, you’ll typically receive 26 paychecks a year. This means that twice a year, you’ll get a “three-paycheck month,” which can be a fantastic bonus if planned for correctly!

Look at your pay stubs and identify your net income (also known as take-home pay). This is the amount that actually lands in your bank account after taxes, health insurance, and retirement contributions are deducted. For a biweekly budget, you’ll use this net amount for each pay period.

Pro tip: Don’t budget based on your gross income. Always use your net income, as that’s the money you actually have available to spend and save.

Step 3: List Your Fixed Expenses (The Non-Negotiables)

Fixed expenses are those bills that typically stay the same amount each month and are due on a regular schedule. These are your “must-pays” that you can’t easily change in the short term.

Examples include:

- Rent/Mortgage payment

- Car payment

- Insurance premiums (car, health, renter’s)

- Loan payments (student loans, personal loans)

- Subscription services (Netflix, Spotify, gym membership)

List these out, noting the amount and the due date for each. Since you’re paid biweekly, you’ll need to figure out how to allocate funds from your two paychecks to cover these monthly expenses. For example, if your rent is $1,000 due on the 1st, and you get paid on the 1st and 15th, you might allocate $500 from each paycheck to a separate “rent savings” account or just ensure enough is in your checking account by the due date.

Pro tip: For monthly fixed expenses, divide the total monthly cost by two to see how much you need to set aside from each biweekly paycheck. For example, if your rent is $1,200/month, you need to allocate $600 from each biweekly paycheck towards it.

Step 4: Track Your Variable Expenses (The Flexibles)

Variable expenses are the costs that fluctuate from pay period to pay period or month to month. These are the areas where you have the most control and opportunity to save.

Examples include:

- Groceries

- Dining out/Takeaway

- Utilities (electricity, gas, water – these can vary)

- Transportation (gas, public transit fares)

- Entertainment/Hobbies

- Personal care (haircuts, toiletries)

- Clothing

Review your bank and credit card statements from Step 1 and categorize your spending over the past month or two. This will give you a realistic average of what you’re currently spending in these categories. Don’t judge, just observe.

Pro tip: Be brutally honest with yourself here. It’s easy to underestimate how much you spend on coffee or impulse buys. The more accurate your tracking, the more effective your budget will be.

Step 5: Create Your Biweekly Budget Framework

Now it’s time to put it all together! You’ll create a budget that aligns with your biweekly paychecks.

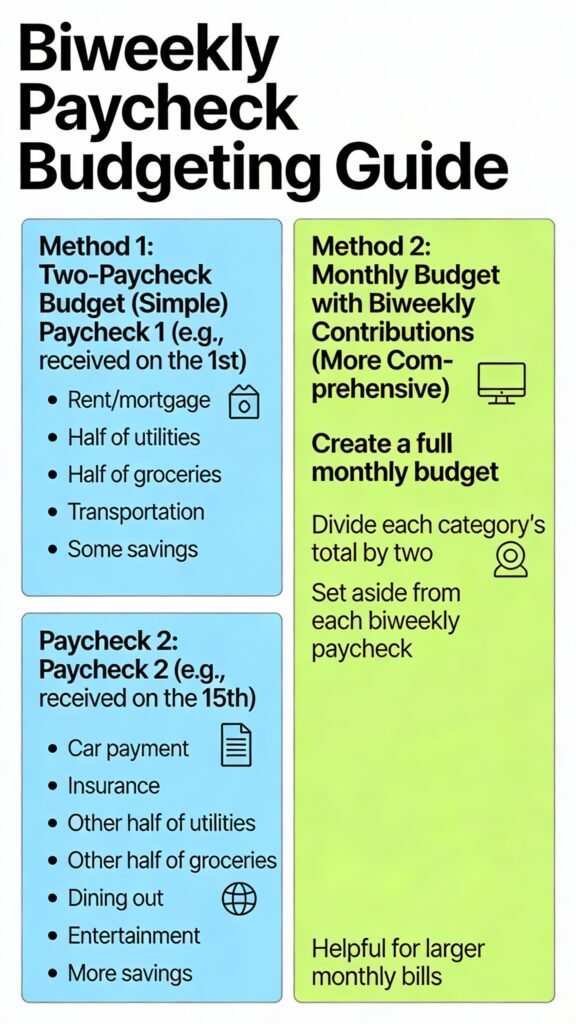

Method 1: Two-Paycheck Budget (Simple)

Allocate specific bills to each of your two paychecks within a month. For example:

- Paycheck 1 (e.g., received on the 1st): Cover rent/mortgage, half of utilities, half of groceries, transportation, and some savings.

- Paycheck 2 (e.g., received on the 15th): Cover car payment, insurance, other half of utilities, other half of groceries, dining out, entertainment, and more savings.

Method 2: Monthly Budget with Biweekly Contributions (More Comprehensive)

Create a full monthly budget, then divide each category’s total by two to determine how much you need to set aside from each biweekly paycheck. This is especially helpful for those larger monthly bills that don’t perfectly align with a biweekly cycle.

For example, if your monthly grocery budget is $400, you’ll allocate $200 from each biweekly paycheck for groceries. If your rent is $1,200, you’ll allocate $600 from each paycheck.

Choose the method that feels most intuitive for you. The goal is to make sure all your expenses are covered by the time they’re due, with enough left over for savings and discretionary spending.

Pro tip: Use a spreadsheet or a budgeting app (like YNAB, Mint, or EveryDollar) to organize your budget. Spreadsheets offer maximum flexibility, while apps often automate tracking and categorization.

Step 6: Set Your Saving Goals (Make Them SMART)

Budgeting isn’t just about cutting spending; it’s about intentional saving towards your dreams. What are you saving for? An emergency fund? A down payment on a house? A vacation? Retirement?

Make your goals SMART:

- Specific: “Save $5,000 for a down payment.”

- Measurable: “Save $200 per paycheck.”

- Achievable: Is $200 realistic given your income and expenses?

- Relevant: Does this goal align with your broader financial aspirations?

- Time-bound: “By December 31st next year.”

Prioritize an emergency fund first (3-6 months of essential living expenses). Once that’s established, you can focus on other goals.

Pro tip: Treat savings like a non-negotiable fixed expense. Allocate a specific amount to savings from each biweekly paycheck before you even think about discretionary spending. This is often called “paying yourself first.”

Step 7: Allocate Funds & Create Your Budget

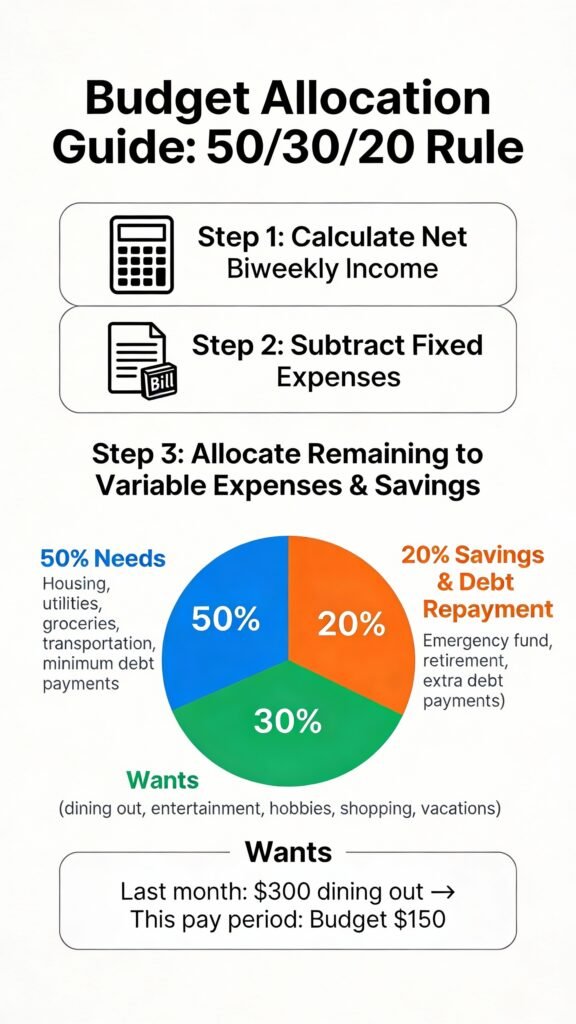

Now, take your net biweekly income and subtract your fixed expenses (allocated biweekly). What’s left is what you have for variable expenses and savings.

Start assigning amounts to your variable expense categories based on your tracking from Step 4 and your saving goals from Step 6. This is where you make conscious choices. If you spent $300 on dining out last month but want to save more, you might budget only $150 for dining out this pay period.

A common budgeting rule is the 50/30/20 rule:

- 50% Needs: Housing, utilities, groceries, transportation, minimum debt payments.

- 30% Wants: Dining out, entertainment, hobbies, shopping, vacations.

- 20% Savings & Debt Repayment: Emergency fund, retirement, extra debt payments.

Adjust these percentages to fit your specific situation and goals. The most important thing is that Income – Expenses – Savings = 0. This is called a zero-based budget, where every dollar has a job.

Pro tip: Don’t forget a “Miscellaneous” or “Buffer” category. Life happens, and having a small buffer can prevent you from derailing your budget when unexpected small costs pop up.

Step 8: Implement and Track Your Spending

A budget is just a plan until you put it into action. For the next two weeks (your biweekly pay period), actively track every dollar you spend.

How to track:

- Manually: Keep a small notebook or use a dedicated budgeting app on your phone.

- Digitally: Link your bank accounts to a budgeting app (Mint, YNAB, Personal Capital) that automatically categorizes transactions.

- Cash Envelopes: Withdraw cash for variable categories (groceries, entertainment) and only spend what’s in the envelope. When it’s gone, it’s gone.

The goal is to stay within the limits you set for each category. If you find yourself overspending in one area, look for opportunities to cut back in another or adjust your plan for the next pay period.

Pro tip: Don’t beat yourself up if you overspend in a category. The first few pay periods are about learning and adjusting. The key is to acknowledge it and make a plan to do better next time.

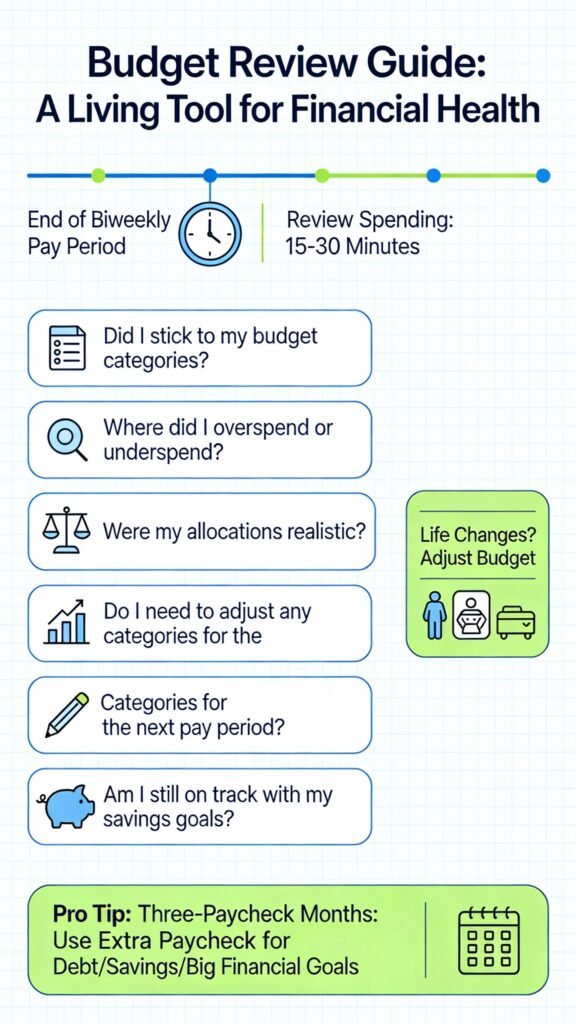

Step 9: Review and Adjust Biweekly

Your budget isn’t a set-it-and-forget-it document; it’s a living tool that needs regular attention. At the end of each biweekly pay period (or before your next paycheck arrives), take 15-30 minutes to review your spending.

Ask yourself:

- Did I stick to my budget categories?

- Where did I overspend or underspend?

- Were my allocations realistic?

- Do I need to adjust any categories for the next pay period?

- Am I still on track with my savings goals?

Life changes, and so should your budget. You might find you consistently spend less on transportation or more on groceries. Adjust your budget to reflect your reality and your evolving goals.

Pro tip: Pay attention to those “three-paycheck months.” When they occur, use that extra paycheck strategically – put it all towards debt, savings, or a big financial goal. Don’t let it just disappear!

Step 10: Automate Your Savings and Bill Payments

This is a game-changer for building wealth and reducing financial stress. Once you have your budget dialed in, automate as much as you can.

- Automate Savings: Set up automatic transfers from your checking account to your savings accounts (emergency fund, down payment fund, investment accounts) on your payday. Even small, consistent amounts add up significantly over time.

- Automate Bills: Set up automatic payments for your fixed expenses (rent, loans, subscriptions) directly from your checking account. Make sure these are timed to go out shortly after your paychecks arrive to avoid overdrafts.

Automation takes the mental effort and willpower out of saving and paying bills, ensuring you consistently make progress towards your financial goals.

Pro tip: Schedule automated transfers to hit your savings accounts the day after your paycheck lands. This way, you “pay yourself first” before you even have a chance to spend the money.

Common Mistakes to Avoid

Making mistakes is part of learning, but being aware of common pitfalls can help you navigate your budgeting journey more smoothly.

-

Being Unrealistic with Categories:

Why it’s problematic: If you budget $50 for groceries when you consistently spend $150, you’re setting yourself up for failure and frustration. An unrealistic budget will be abandoned quickly.

Correct approach: Use your historical spending data (from Step 4) to create realistic initial allocations. As you track, adjust categories to reflect your actual habits and needs, making small, sustainable cuts over time.

-

Neglecting Small, Recurring Expenses:

Why it’s problematic: Those daily coffees, streaming services you barely use, or small impulse buys add up significantly. Ignoring them creates “budget leaks” that can drain your funds without you realizing it.

Correct approach: Track every dollar, no matter how small. Be mindful of subscription creep and review them regularly. Small adjustments in these areas can free up surprising amounts of money.

-

Not Tracking Spending Consistently:

Why it’s problematic: A budget without tracking is just a wish list. If you don’t know where your money is actually going, you can’t make informed decisions or adjustments.

Correct approach: Choose a tracking method (app, spreadsheet, pen and paper) that works for you and commit to using it daily or every few days. Make it a habit until it feels natural.

-

Giving Up After One Slip-Up:

Why it’s problematic: Everyone overspends sometimes. If you treat one mistake as a reason to abandon your entire budget, you lose all the progress you’ve made.

Correct approach: View your budget as a learning tool. Acknowledge the slip-up, understand why it happened, adjust your plan for the next pay period, and get right back on track. Consistency, not perfection, is the goal.

-

Forgetting About Irregular Expenses:

Why it’s problematic: Annual car registration, holiday gifts, doctor’s visits, or home maintenance costs can blow up a budget if not planned for, leading to debt or dipping into savings.

Correct approach: Create a “sinking fund” for these irregular expenses. Estimate their annual cost, divide by 26 (for biweekly), and set aside that amount from each paycheck into a separate savings account. For example, if car registration is $300 annually, set aside ~$11.50 per paycheck.

Troubleshooting

Even with the best planning, you might encounter bumps in the road. Here are some common issues and quick solutions.

-

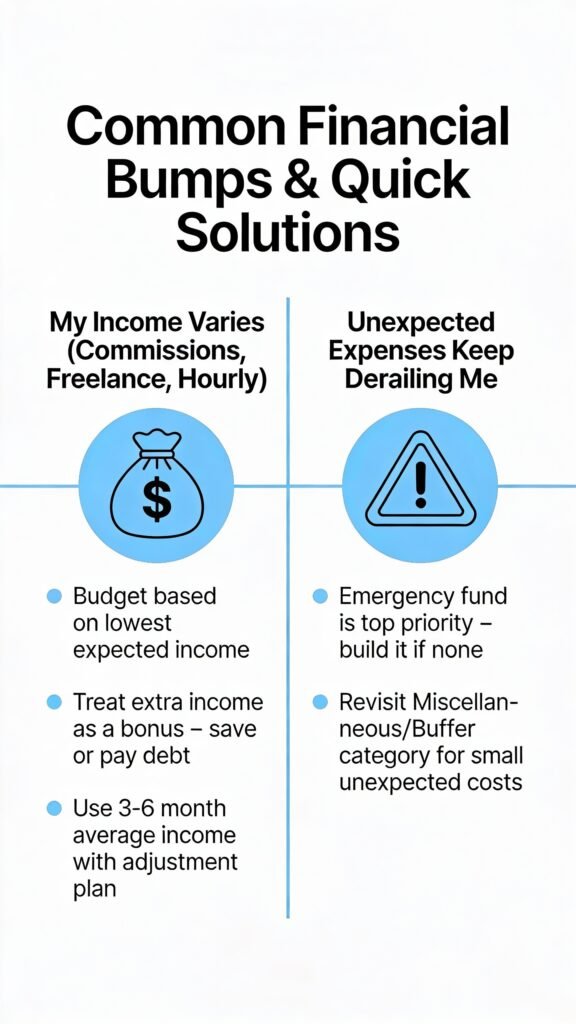

“My Income Varies (Commissions, Freelance, Hourly):”

Solution: Budget based on your lowest expected income. When you have a higher-than-expected paycheck, treat the extra as a bonus – put it directly into savings or use it to pay down debt. Alternatively, you can take your average income over the last 3-6 months and budget based on that, but be prepared to adjust if a low-income period hits.

-

“Unexpected Expenses Keep Derailing Me:”

Solution: This is precisely why an emergency fund is your number one priority. If you don’t have one, focus intensely on building it up. For smaller, less critical unexpected costs, revisit your “Miscellaneous” or “Buffer” category and consider increasing it slightly. If it’s a larger, truly unexpected expense and you don’t have an emergency fund, look for areas in your variable spending where you can temporarily cut back to cover the cost, rather than going into debt.

-

“I Feel Overwhelmed and Deprived:”

Solution: Budgeting shouldn’t feel like a punishment. If you feel deprived, your budget might be too restrictive. Revisit your “Wants” categories. Can you reallocate funds to allow for a small treat or activity that brings you joy? Remember, the goal is balance. Also, focus on your “why” – the saving goals that motivate you. Seeing progress towards a big dream can be incredibly motivating and counteract feelings of deprivation.

Key Takeaways

- Knowledge is Power: Understanding your biweekly income and where every dollar goes is the first step to financial control.

- Pay Yourself First: Prioritize savings by automating transfers to your goals the moment you get paid.

- Be Realistic & Flexible: Create a budget that reflects your actual spending, and be prepared to adjust it regularly as life changes.

- Track Consistently: Monitor your spending to ensure you’re sticking to your plan and to identify areas for improvement.

- Automate for Success: Use automatic transfers for savings and bill payments to reduce friction and increase consistency.

- Progress, Not Perfection: Don’t get discouraged by slip-ups. Learn from them and get back on track.

Frequently Asked Questions

Q: What’s the best budgeting tool for beginners?

A: For absolute beginners, a simple spreadsheet (Google Sheets or Excel) or even pen and paper can be great because they force you to manually input everything, which reinforces awareness. As you get more comfortable, apps like Mint (free, good for tracking), YNAB (You Need A Budget – paid, zero-based philosophy), or EveryDollar (free/paid, zero-based) offer more features and automation.

Q: How often should I check my budget?

A: Ideally, you should quickly check your spending every few days to stay on top of your categories. A more thorough review and adjustment should happen at the end of each biweekly pay period before your next paycheck arrives.

Q: Can I still have fun while on a budget?

A: Absolutely! A good budget isn’t about deprivation; it’s about intentional spending. By planning for your “wants” and allocating funds for entertainment, dining out, or hobbies, you can enjoy these things guilt-free, knowing you’re also on track with your financial goals.

Q: What do I do with the “extra” paycheck in a three-paycheck month?

A: This is a fantastic opportunity! Plan for it well in advance. Use the extra paycheck to turbocharge your financial goals:

- Aggressively pay down high-interest debt.

- Boost your emergency fund.

- Contribute extra to retirement or investment accounts.

- Save for a large, upcoming purchase or a special treat.

The key is to have a plan for it before it even hits your account.

What’s Next?

Congratulations! You’ve taken a massive step towards financial mastery by creating a biweekly budget. But this is just the beginning of your journey to financial freedom.

Once you’re comfortable with your budget, consider exploring these next steps:

- Debt Reduction Strategies: If you have consumer debt (credit cards, personal loans), research methods like the “debt snowball” or “debt avalanche” to pay it off faster.

- Investing for the Future: Learn about different investment vehicles (401k, IRA, Roth IRA, taxable brokerage accounts) and start building long-term wealth.

- Increasing Your Income: Explore ways to boost your earnings, whether through a side hustle, negotiating a raise, or developing new skills.

- Optimizing Your Spending: Continuously look for ways to save money on recurring expenses, like negotiating bills, finding cheaper insurance, or meal prepping.

The most important step is to start today. Don’t wait for the “perfect” time or the “perfect” tool. Grab your statements, open a spreadsheet, and begin building your financial future, one biweekly paycheck at a time. You’ve got this!