🏡 3 Houses In One Compound

📚 The Financial Literacy Library

The best investment you can ever make is in your own financial education. These 5 cornerstone books are what millionaires, financial advisors, and wealth-builders universally recommend for completely rewiring how you think about earning, saving, and investing money.

🧠 The Psychology of Money

Doing well with money isn't necessarily about what you know—it's about how you behave. Morgan Housel masterfully breaks down the emotional and psychological biases that secretly dictate our financial decisions, offering a true paradigm shift in how to view wealth.

🏠 Rich Dad Poor Dad

The #1 personal finance book of all time for a reason. This foundational read shatters the myth that you need to earn a high income to be rich, teaching you the critical difference between working for money and making your money work for you via assets.

📈 Atomic Habits

While not strictly a finance book, building wealth is absolutely dependent on the daily habits you cultivate. James Clear provides the definitive framework for breaking bad spending habits and effortlessly automating the good ones that lead to long-term success.

📊 The Simple Path to Wealth

The ultimate antidote to complex, intimidating financial advice. JL Collins provides an incredibly accessible, low-stress roadmap to financial independence through index fund investing, perfectly explaining why simplicity beats Wall Street complexity every time.

💳 I Will Teach You to Be Rich

A tactical, no-BS, 6-week program that actually works. Ramit Sethi teaches you how to crush debt, automate your savings, and negotiate your salary—all while guilt-free spending on the things you truly love. A must-read for modern money management.

Ever dreamed of a life where financial freedom isn’t just a buzzword, but a tangible reality? Imagine a scenario where your housing costs are dramatically reduced, a supportive community is built right into your daily life, and your property is actively working to build your wealth. This isn’t a pipe dream; it’s the powerful potential of “3 Houses In One Compound.”

In an era of soaring housing prices and a growing desire for community and financial stability, innovative living solutions are becoming more appealing than ever. The concept of having three distinct homes on a single plot of land offers a unique blend of privacy, shared resources, and unparalleled financial advantages. Whether you’re looking to create a multi-generational family hub, generate significant rental income, or co-invest with friends, this approach is a money-smart move that could redefine your financial trajectory and quality of life.

This comprehensive guide will unpack the “3 Houses In One Compound” model, revealing its practical benefits, offering actionable financial strategies, and equipping you with the mindset to turn this vision into a thriving reality. Get ready to explore a path to smart living, savvy saving, and serious wealth building.

What is 3 Houses In One Compound?

At its core, “3 Houses In One Compound” refers to a single piece of property that contains three separate, habitable residential units. While the exact configuration can vary widely based on local zoning laws and personal preferences, the fundamental idea remains the same: three distinct living spaces sharing one underlying land parcel.

Let’s break down what this can look like:

- Main House + Two Accessory Dwelling Units (ADUs): This is a very common setup. You might have a primary residence and then two smaller, independent units built either attached to the main house (like a basement apartment or an above-garage unit) or detached on the same property (like tiny homes, granny flats, or converted garages). Each ADU would typically have its own kitchen, bathroom, and entrance.

- Three Standalone Homes: In some cases, especially on larger plots of land or in areas with specific zoning, you might find three smaller, completely separate houses built on the same lot. Think of it as a mini-cul-de-sac or a small village feel, all within one property boundary.

- Duplex/Triplex + One Detached Unit: Another variation could involve a duplex (two units in one building) plus an additional detached unit, or even a triplex (three units in one building) if local regulations allow. The key is that each unit offers independent living.

The beauty of this model lies in its versatility and the diverse ways people leverage it:

- Multi-Generational Living: Imagine grandparents living in one unit, parents and children in another, and perhaps an adult child or a relative in the third. This fosters a close-knit family environment, provides built-in support for childcare or eldercare, and allows families to pool resources for a higher quality of life. It’s a powerful way to keep family close while maintaining individual privacy.

- Investment Property (House Hacking on Steroids): This is where the money-smart aspect truly shines. You can live in one unit and rent out the other two. The rental income from the two units can significantly offset, or even completely cover, your mortgage payment, property taxes, and insurance. This strategy, often called “house hacking,” allows you to live virtually for free while building substantial equity and passive income.

- Co-Housing or Community Living: A group of friends, like-minded individuals, or even business partners might purchase a property like this together. Each household enjoys its private space while sharing common amenities, responsibilities, and the financial burden of homeownership. This creates a strong support network and a shared vision for living.

- Hybrid Model: Perhaps you live in one unit, rent out a second for income, and use the third as a dedicated home office, a guest house for visiting family, or even a short-term rental for additional income streams during peak seasons. The flexibility is immense.

Regardless of the specific configuration or use case, the underlying financial benefits are compelling. By sharing land costs, potentially sharing utilities, and generating significant rental income, “3 Houses In One Compound” presents a unique opportunity to achieve financial freedom, accelerate wealth building, and live a richer, more connected life.

Key Features

The appeal of “3 Houses In One Compound” isn’t just a trendy idea; it’s rooted in powerful practical and financial advantages. Let’s explore the key features that make this model a smart choice for the money-savvy individual or family.

Financial Leverage & Wealth Acceleration

This is arguably the most compelling feature. Owning three income-generating units on one property provides unparalleled financial leverage:

- Reduced Individual Housing Costs: Instead of one household bearing the full burden of a mortgage, property taxes, and insurance, these costs are effectively spread across three units. For owner-occupiers, rental income from the other two units can drastically reduce or even eliminate your personal housing expenses, freeing up significant cash flow. Imagine what you could do with an extra $1,500, $2,000, or even $3,000+ per month!

- Significant Rental Income Potential: Two additional units mean two streams of rental income. This isn’t just pocket money; it can be substantial passive income that directly contributes to your wealth. This income can be used to pay down the mortgage faster, invest in other assets, or simply boost your monthly savings.

- Shared Property Expenses: Property taxes, homeowner’s insurance, and major maintenance (like roof repairs or driveway paving) are all shared costs. This collective responsibility makes large expenses far more manageable for each individual unit.

- Accelerated Mortgage Payoff: With the extra income from rentals, you have the option to make additional principal payments on your mortgage. This can shave years off your loan term and save you tens of thousands in interest, building equity at an incredible pace.

- Increased Property Value: Multi-unit properties often appreciate faster than single-family homes, especially in high-demand areas. The income-generating potential makes them highly attractive to investors, further boosting their market value.

Community & Support System

Beyond the financial gains, this living arrangement offers invaluable social benefits:

- Built-in Support: Whether it’s help with childcare, eldercare, pet-sitting, or simply borrowing a cup of sugar, a built-in community provides a safety net and convenient support system. This can be especially valuable for young families or aging relatives.

- Enhanced Security: More eyes and ears on the property naturally lead to increased security. There’s always someone around, fostering a sense of safety and peace of mind.

- Shared Resources & Responsibilities: From communal gardens and shared tools to splitting chores like snow removal or yard work, sharing resources reduces individual burden and fosters a sense of collective ownership.

- Stronger Bonds: Living in close proximity, especially with family or close friends, can strengthen relationships and create lasting memories. It’s a return to a more communal, interconnected way of life.

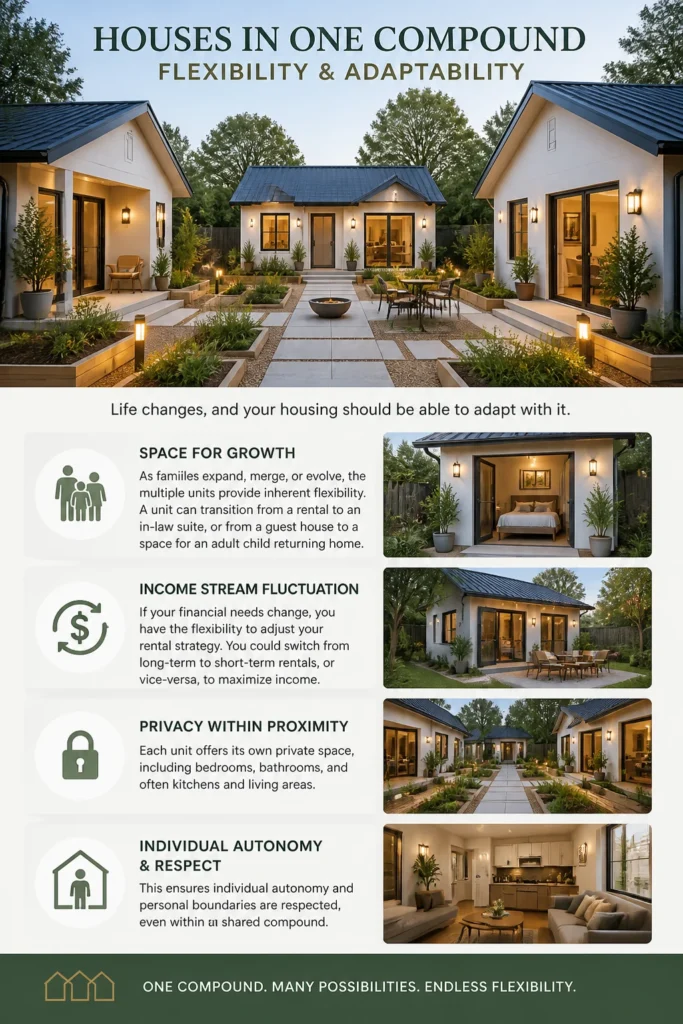

Flexibility & Adaptability

Life changes, and your housing should be able to adapt with it:

- Space for Growth: As families expand, merge, or evolve, the multiple units provide inherent flexibility. A unit can transition from a rental to an in-law suite, or from a guest house to a space for an adult child returning home.

- Income Stream Fluctuation: If your financial needs change, you have the flexibility to adjust your rental strategy. You could switch from long-term to short-term rentals, or vice-versa, to maximize income.

- Privacy Within Proximity: Each unit offers its own private space, including bedrooms, bathrooms, and often kitchens and living areas. This ensures individual autonomy and personal boundaries are respected, even within a shared compound.

Sustainability & Efficiency

- Smaller Environmental Footprint: Sharing land and potentially some utilities can lead to a more efficient use of resources and a reduced overall environmental impact compared to three separate single-family homes on individual lots.

- Potential for Shared Green Initiatives: It’s easier and more cost-effective to implement shared solar panels, rainwater harvesting systems, or communal composting when resources are pooled across units.

These features combine to create a compelling argument for “3 Houses In One Compound” as a savvy financial move and a pathway to a richer, more connected lifestyle.

How to Get Started

Embarking on the “3 Houses In One Compound” journey requires careful planning, open communication, and a strategic financial approach. Here’s a step-by-step guide to help you lay a solid foundation for success.

Step 1: Define Your Vision & Assemble Your Team

Before anything else, get crystal clear on your “why.”

- Clarify Your Purpose: Is this primarily for multi-generational living, a pure investment play, or a co-housing community? Your purpose will dictate many subsequent decisions, from property layout to financial agreements.

- Identify Your Partners: Who will be sharing this journey with you? Family members, trusted friends, or business partners? This is a critical step, as strong relationships built on trust are paramount.

- Establish Communication Guidelines: From day one, commit to open, honest, and regular communication. Discuss expectations, responsibilities, and potential challenges. A shared vision isn’t enough; you need shared values and a commitment to collaboration.

- Consider Legal Agreements: This is non-negotiable. Even with family, a formal co-ownership agreement or partnership agreement is crucial. This document should outline ownership percentages, financial contributions, responsibility for expenses, decision-making processes, dispute resolution mechanisms, and, importantly, exit strategies (what happens if someone wants to sell or move out). Consult with a real estate attorney early on.

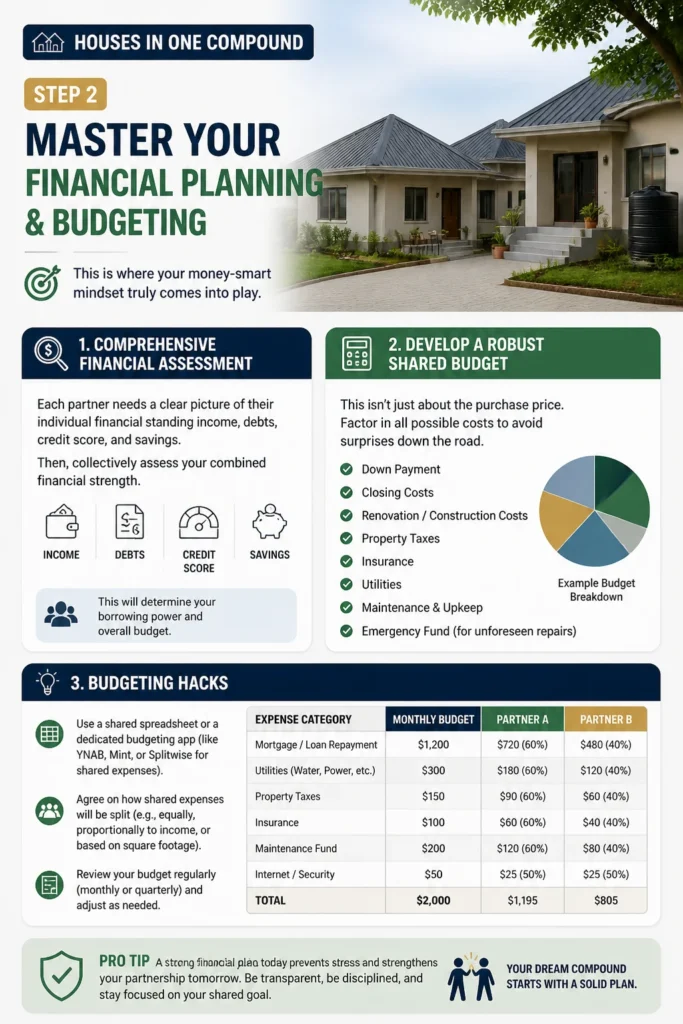

Step 2: Master Your Financial Planning & Budgeting

This is where your money-smart mindset truly comes into play.

- Comprehensive Financial Assessment: Each partner needs a clear picture of their individual financial standing: income, debts, credit score, and savings. Then, collectively assess your combined financial strength. This will determine your borrowing power and overall budget.

- Develop a Robust Shared Budget: This isn’t just about the purchase price. Factor in down payment, closing costs, renovation/construction costs, property taxes, insurance, utilities, and a significant emergency fund for unforeseen repairs.

- Budgeting Hacks: Use a shared spreadsheet or a dedicated budgeting app (like YNAB, Mint, or Splitwise for shared expenses). Agree on how shared expenses will be split (e.g., equally, proportionally to income, or based on square footage occupied).

- “Sinking Funds”: Create dedicated savings accounts (sinking funds) for predictable future expenses like annual property taxes, insurance premiums, and a long-term maintenance fund for big-ticket items (roof, HVAC, exterior paint). Contribute to these monthly.

- Explore Financing Options:

- Joint Mortgage: The most common for family or partners. All parties are typically on the loan.

- Multi-Unit Property Loans: Lenders often view properties with 2-4 units as residential, making them eligible for conventional mortgages. They may even consider potential rental income to help you qualify.

- Construction Loans: If you’re building or undertaking major renovations, you’ll likely need a construction loan, which converts to a permanent mortgage once the project is complete.

- FHA Loans: If you plan to live in one unit, an FHA loan (for 2-4 units) can offer lower down payment options, but there are specific eligibility requirements.

- Build a Strong Emergency Fund: Beyond individual emergency funds, a collective emergency fund for the property itself is vital. Aim for 3-6 months of all shared expenses. This prevents financial stress when unexpected repairs pop up.

Step 3: Location, Location, Location & Property Search

The right property in the right place is paramount.

- Research Zoning Laws: CRITICAL! Before you even fall in love with a property, research local zoning ordinances. Not all areas permit multiple dwelling units on a single lot, or they may have strict regulations regarding ADUs (size, setback, parking, owner-occupancy requirements). Check with your local planning department.

- Consider Amenities & Infrastructure: Look for areas with good schools, proximity to jobs, public transport, parks, and essential services. If you’re planning rentals, these factors greatly influence tenant demand and rental rates.

- Evaluate Land Size & Existing Structures: Do you need to build from scratch, or can you convert existing structures (like a large garage or basement) into ADUs? Is there enough space for privacy between units?

- Work with a Knowledgeable Real Estate Agent: Find an agent experienced in multi-unit properties, ADUs, and investment properties in your target area. They can help navigate zoning and identify suitable properties.

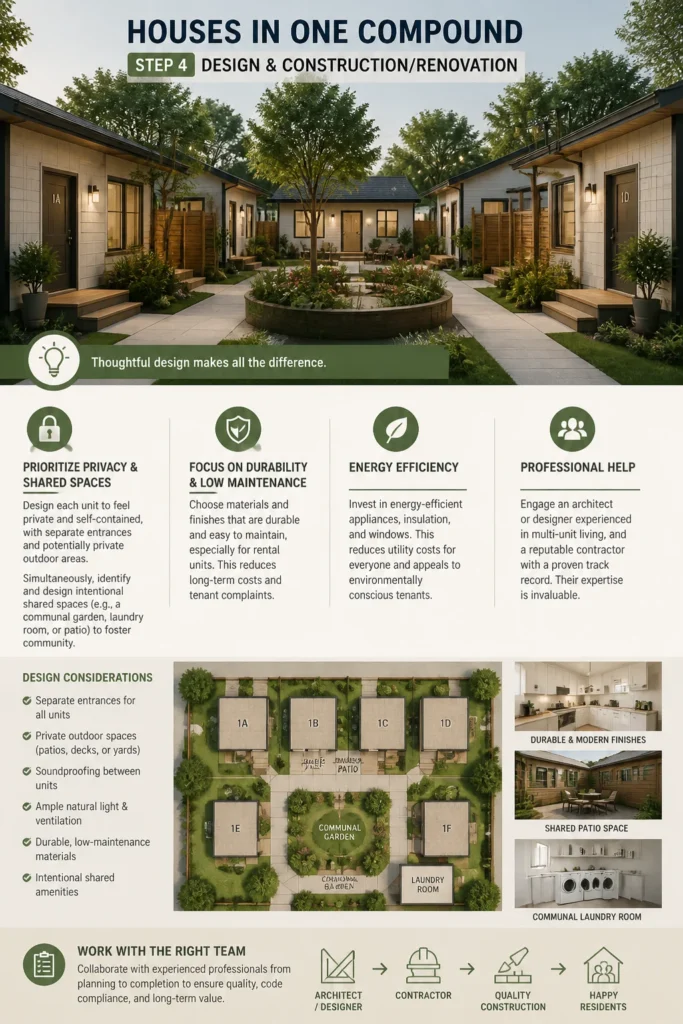

Step 4: Design & Construction/Renovation

Thoughtful design makes all the difference.

- Prioritize Privacy & Shared Spaces: Design each unit to feel private and self-contained, with separate entrances and potentially private outdoor areas. Simultaneously, identify and design intentional shared spaces (e.g., a communal garden, laundry room, or patio) to foster community.

- Focus on Durability & Low Maintenance: Choose materials and finishes that are durable and easy to maintain, especially for rental units. This reduces long-term costs and tenant complaints.

- Energy Efficiency: Invest in energy-efficient appliances, insulation, and windows. This reduces utility costs for everyone and appeals to environmentally conscious tenants.

- Professional Help: Engage an architect or designer experienced in multi-unit living, and a reputable contractor. They can ensure your vision meets local codes and is executed efficiently.

Step 5: Legal & Administrative Setup

- Property Deeds & Co-Ownership: Ensure the property deed accurately reflects the ownership structure (e.g., Tenants in Common, Joint Tenancy). Your attorney will guide you here.

- Utility Setup: Determine if you can (or need to) sub-meter utilities for each unit (electricity, water, gas) or if you’ll split a master bill. Sub-metering is often preferred for fairness, especially with renters.

- Insurance: Obtain appropriate homeowner’s insurance that covers multiple units, potential renters, and liability.

- Rental Agreements (if applicable): If you’re renting units, have robust, legally sound lease agreements in place for each tenant.

By meticulously working through these steps, you’ll be well on your way to creating a successful and financially rewarding “3 Houses In One Compound” living arrangement.

Tips for Success

Building and living in a “3 Houses In One Compound” setup is a journey that thrives on smart strategies and a proactive mindset. Here are 5 pro tips to ensure your venture is not just successful, but truly transformative for your finances and lifestyle.

Tip 1: Master Your Shared Budget & Financial Communication

This is the bedrock of any successful shared living arrangement, especially one with significant financial implications. Just as you budget your personal finances, you need a meticulous budget for the compound.

- Implement Joint Accounts for Shared Expenses: Set up a separate joint bank account specifically for property-related expenses (mortgage, taxes, insurance, shared utilities, maintenance fund). Each party contributes a pre-agreed amount monthly. This simplifies tracking and avoids awkward “who owes what” conversations.

- Regular Financial Check-ins: Schedule monthly or quarterly meetings with all stakeholders to review the budget, discuss upcoming expenses, and ensure everyone is contributing as agreed. Transparency builds trust.

- “Pay Your Shared Fund First”: Just like you’d “pay yourself first” for personal savings, prioritize contributions to the compound’s joint accounts. This ensures the property’s financial health is robust.

- Automate Everything Possible: Set up automatic transfers for mortgage payments, utility bills, and contributions to the shared expense account. Automation reduces human error and stress.

Tip 2: Prioritize Clear Communication & Establish Boundaries

Living in close proximity, even with separate units, requires excellent interpersonal skills and clearly defined expectations.

- Regular “Compound Meetings”: Beyond financial discussions, hold regular meetings to discuss shared responsibilities, potential issues, and general well-being. This proactive approach prevents small annoyances from escalating.

- Define Personal & Shared Spaces: Clearly delineate what areas are private to each unit and what areas are communal. This includes outdoor spaces, storage, and even laundry facilities. Respect these boundaries rigorously.

- Develop a Conflict Resolution Strategy: It’s not if conflicts will arise, but when. Agree beforehand on a process for resolving disagreements fairly and respectfully. This might involve a neutral third party or a pre-determined decision-making framework.

- Noise & Privacy Expectations: Discuss acceptable noise levels, guest policies, and how much interaction is desired. Some prefer more communal interaction, others value more solitude. Respect individual preferences.

Tip 3: Embrace the “House Hacker” & Investor Mindset

View your property not just as a home, but as a powerful asset that can generate wealth.

- Optimize Rental Income: Continuously research local rental markets to ensure your units are priced competitively. Consider value-added amenities (e.g., updated appliances, smart home features) that justify higher rents.

- Invest in Smart Upgrades: Prioritize renovations that offer a strong return on investment (ROI), such as energy-efficient windows, updated kitchens/bathrooms, or curb appeal improvements. These increase property value and tenant appeal.

- Learn Basic DIY Skills: Being able to handle minor repairs (leaky faucets, drywall patches, basic electrical) yourself can save hundreds or thousands annually. This directly impacts your bottom line.

- Reinvest for Growth: Consider using a portion of your rental income to pay down the mortgage faster, or to save for future property improvements, or even to invest in other wealth-building assets.

Tip 4: Plan for the Long Term & Exit Strategies

Life is unpredictable; your compound plan shouldn’t be.

- Succession Planning: What happens if one owner wants to move, gets married, has children, passes away, or faces financial hardship? Your co-ownership agreement must clearly outline buy-out clauses, rights of first refusal for remaining owners, or procedures for selling the entire property.

- Review & Update Agreements: Life situations change. Periodically review your legal and financial agreements (e.g., every 3-5 years) to ensure they still reflect everyone’s needs and the current market conditions.

- Consider Property Management: If managing two rental units becomes too time-consuming or stressful, factor in the cost of a property manager. While it eats into profits, it can save you time, headaches, and ensure professional tenant relations.

Tip 5: Leverage Technology for Efficiency

Modern tools can significantly streamline the complexities of shared living and property management.

- Shared Calendars & Task Management Apps: Use Google Calendar or Trello to coordinate shared chores, maintenance schedules, and communal events.

- Communication Platforms: A dedicated group chat (e.g., WhatsApp, Signal) for quick updates and non-urgent discussions keeps everyone in the loop.

- Smart Home Technology: Consider smart thermostats for shared areas to optimize energy usage, or smart locks for rental units to simplify tenant turnover.

- Online Rent Collection: Utilize platforms like Zelle, Venmo for shared contributions, or dedicated landlord software (e.g., TurboTenant, Avail) for collecting rent from tenants.

By embedding these tips into your “3 Houses In One Compound” strategy, you’ll not only navigate the complexities with ease but also unlock the full potential of this powerful wealth-building and lifestyle choice.

Common Mistakes to Avoid

While the “3 Houses In One Compound” model offers incredible benefits, certain pitfalls can derail even the most well-intentioned plans. Being aware of these common mistakes can help you steer clear and ensure a smooth, successful journey.

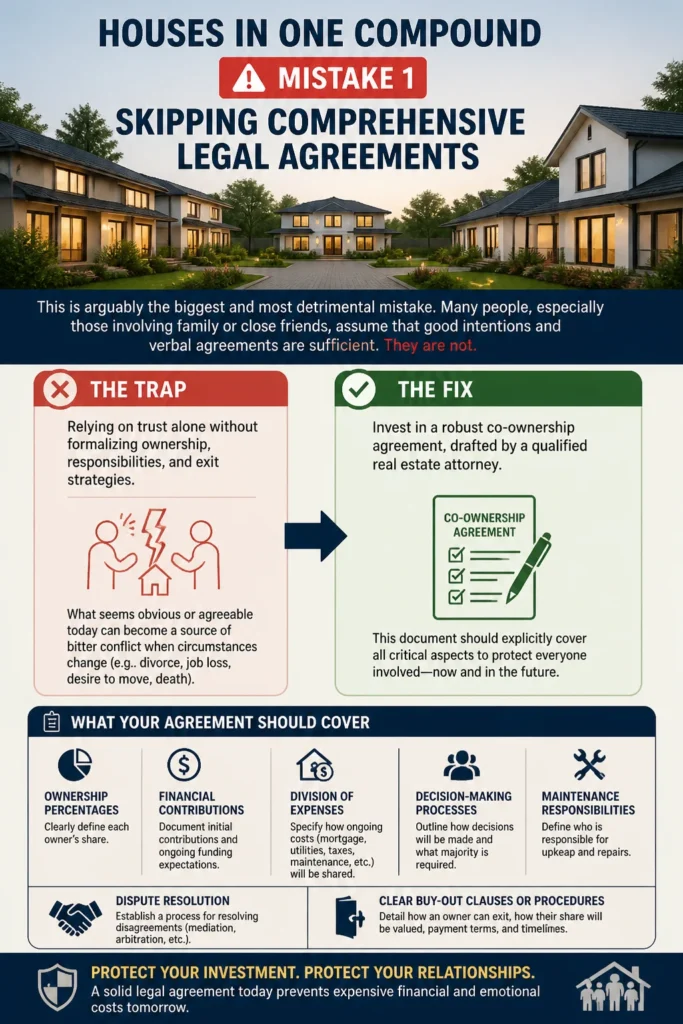

Mistake 1: Skipping Comprehensive Legal Agreements

This is arguably the biggest and most detrimental mistake. Many people, especially those involving family or close friends, assume that good intentions and verbal agreements are sufficient. They are not.

- The Trap: Relying on trust alone without formalizing ownership, responsibilities, and exit strategies. What seems obvious or agreeable today can become a source of bitter conflict when circumstances change (e.g., divorce, job loss, desire to move, death).

- The Fix: Invest in a robust co-ownership agreement, drafted by a qualified real estate attorney. This document should explicitly cover: ownership percentages, financial contributions, division of expenses, decision-making processes, dispute resolution, maintenance responsibilities, and most importantly, clear buy-out clauses or procedures for selling the property if one party wishes to leave. Think of it as pre-nuptial agreement for your property.

Mist2: Inadequate Financial Planning & Underestimating Costs

The excitement of the vision can sometimes overshadow the gritty details of budgeting.

- The Trap: Focusing only on the purchase price and mortgage, neglecting crucial additional costs like closing costs, renovation/construction expenses, property taxes, insurance, ongoing maintenance, and potential vacancies for rental units. Not having a robust emergency fund for the property is another major oversight.

- The Fix: Create a detailed, line-by-line budget that accounts for every conceivable expense, both upfront and ongoing. Get multiple quotes for construction/renovation. Build a significant contingency fund (10-20% of project costs) for unexpected overruns. Establish and consistently contribute to a dedicated emergency fund for the property (e.g., 3-6 months of all shared expenses). Factor in potential rental income fluctuations or vacancies; don’t count on 100% occupancy year-round.

Mistake 3: Neglecting Communication & Boundaries

Even with legal agreements, a lack of ongoing communication can erode relationships and create tension.

- The Trap: Avoiding difficult conversations, letting small annoyances fester, assuming others know what you’re thinking, or failing to set clear personal and shared boundaries. This can lead to resentment, passive aggression, and a breakdown of the living arrangement.

- The Fix: Implement regular, structured meetings to discuss property matters, shared responsibilities, and any concerns. Establish clear boundaries for noise, shared spaces, guest policies, and privacy. Practice active listening and empathy. Remember, while you’re sharing a compound, each unit is a separate home, and individual privacy must be respected.

Mistake 4: Ignoring Zoning Laws & Building Regulations

Local laws dictate what you can and cannot build or convert on your property. Ignoring them can lead to costly fines, demolition orders, and legal headaches.

- The Trap: Assuming you can build an ADU or convert a garage without checking local zoning ordinances, setback requirements, parking rules, or obtaining necessary permits. What’s allowed in one town might be strictly prohibited in another.

- The Fix: Before purchasing a property or starting any construction, thoroughly research local zoning laws and building codes. Consult with your local planning department, a real estate attorney, and an architect or contractor familiar with multi-unit properties in your area. Always obtain all necessary permits and ensure all work is inspected and approved. This due diligence can save you immense time and money.

Mistake 5: Overlooking Tenant Management (If Renting)

If your goal is to generate rental income, treating your tenants professionally is crucial for long-term success.

- The Trap: Not properly screening tenants, having vague or incomplete lease agreements, failing to conduct regular maintenance, or being unresponsive to tenant issues. This can lead to high turnover, property damage, legal disputes, and lost income.

- The Fix: Develop a rigorous tenant screening process (credit checks, background checks, reference checks). Use legally sound, comprehensive lease agreements. Be a proactive and professional landlord: conduct regular property inspections, address maintenance requests promptly, and maintain open lines of communication. Consider setting up a separate bank account for rental income and expenses to simplify tax reporting. If the thought of managing tenants feels overwhelming, factor in the cost of a professional property manager from the outset.

By being mindful of these common mistakes and proactively addressing them, you can significantly increase your chances of a rewarding and financially successful “3 Houses In One Compound” experience.

FAQ

Embarking on a “3 Houses In One Compound” venture naturally brings up a lot of questions. Here are some common ones, answered with a money-smart and practical focus.

Q1: Is it hard to get a mortgage for 3 houses in one compound?

A: Not necessarily harder, but it’s different from a single-family home mortgage. Lenders typically classify properties with 2-4 units as “multi-unit residential.” This means you can often qualify for a conventional residential mortgage, rather than a more complex commercial loan (which usually applies to 5+ units). The good news is that lenders will often consider the potential rental income from the other two units when assessing your loan application, which can significantly boost your borrowing power and make qualification easier. However, expect stricter scrutiny on your credit score, debt-to-income ratio, and a larger down payment might be required compared to a 1-unit property (though not always). It’s crucial to work with a mortgage broker or lender experienced in multi-unit property financing.

Q2: How do we handle shared utility bills fairly among three units?

A: Fairness in shared utilities is key to harmony. Here are a few money-smart approaches:

- Sub-Metering: The most equitable solution is to install separate meters for electricity, water, and gas for each unit. This way, each household pays for exactly what they use. While there’s an upfront cost for installation, it eliminates disputes and encourages conservation.

- Fixed Percentage Split: If sub-metering isn’t feasible, you could agree on a fixed percentage split based on unit size, number of occupants, or an agreed-upon estimate of usage. For example, the largest unit pays 40%, the middle 35%, and the smallest 25%. This requires trust and periodic review.

- Usage-Based Estimation: For utilities like internet or trash, you might split equally. For water, if there’s a shared meter, consider a base split plus an additional amount per occupant.

Regardless of the method, ensure it’s clearly outlined in your co-ownership agreement and revisited periodically to ensure it remains fair.

Q3: What if one person wants to move out or sell their share?

A: This is a critical scenario that absolutely must be addressed in your initial co-ownership agreement. Without a clear plan, it can lead to significant financial and relational stress. Common solutions include:

- Buy-Out Clause: The agreement should specify how the remaining owners can buy out the departing owner’s share. This often involves an agreed-upon valuation method (e.g., professional appraisal, agreed formula) and payment terms.

- Right of First Refusal: The departing owner must first offer their share to the remaining owners at a certain price before they can offer it to an external third party.

- Forced Sale Clause: In some agreements, if a buy-out isn’t feasible, the agreement may stipulate that the entire property must be sold, and the proceeds distributed according to ownership shares.